The Business of PolicyBazaar

A Deep Dive into the past, present and future of India's first InsureTech Unicorn

Disclaimer: No part of this article is investment advice, please consult a financial advisor before investing

Mr. Yashish Dahiya is an impatient man. In one of the interviews with The Ken, he narrated a story of how while in college he used to run home to Noida every Friday and back to college on a Monday morning (both 30kms in one direction) as he found public buses too slow for his liking.

Mr. Dahiya, is also persistent and doesn't give up easy - he is one of the few people in the world who has completed the grueling Ironman triathlon - an intense race that consists of swimming, bicycle ride and a marathon all raced in that order - widely considered one of the most difficult one-day sporting events in the world.

It’s these qualities of impatience, persistence and continuously improving oneself that can be found in the business of PolicyBazaar or PBFinTech, the name of the parent company applying for IPO.

Like most successful start ups - Facebook, Google, Amazon, Apple - PolicyBazaar has a history of reinventing itself and going through several evolutions to get to where it is today.

In this deep dive, I will take you through the journey of PolicyBazaar. We will explore its beginnings, understand some of the failed projects and hurdles it faced along the way, how does it fit into the insurance industry in present day and try to chart a map of the many possible paths it may take in future.

The Beginnings

PolicyBazaar started in June 2008 as an insurance aggregator.

That's a fancy word for stating that it had a website which looked like a form, where a prospective customer could key in their details. These details would then be sent to a call center run by PolicyBazaar, where an employee would call back the prospective customer, understand their requirements and pass on the lead to an insurance company. This insurance company would then try to sell an insurance policy to the customer and if the sale was made, PolicyBazaar would get commission for generating a lead.

This is how their website looked like on July 6th 2008.

As you can observe it was a barebones operation and a very simple solution to an otherwise complicated and an unsolved problem that the insurance industry was facing - the problem of quality data.

Insurance runs on data

As the quality and granularity of data increases, Insurance companies can assess risk behind an insurance policy better and offer that policy at more subsidized rates. PolicyBazaar was created to solve this problem of data - the call center employees at PolicyBazaar were tasked with capturing higher quality and more granular data of customers than a commission based insurance agent would do. As the customers of PolicyBazaar grew, so did this data and with that the importance of PolicyBazaar in the insurance ecosystem.

The most valuable asset today of PolicyBazaar isn't its website, the office buildings it leases, the trademarks or its partnerships with the various insurance companies - it is this data that PolicyBazaar has captured over the years since its inception.

This data helps the company work with its insurance partners and create policies that are suited for a specific need and segment of customers. It is also this quality of data that enables it to pass on discounts from insurance companies in the form of lower premiums to its customers.

In the business of Insurance - data and the quality of data is everything. By solving the problem of generating and storing quality data - PolicyBazaar solved many problems with one platform.

In its DRHP, PolicyBazaar, like every other platform company today, is quick to mention this flywheel - the infinite loop of solving problems both on consumer and insurer side - all via data. It is this flywheel and first mover advantage, that enabled PolicyBazaar to capture 90% market share of the digital insurance segment in India.

Better data leads to lower claims which leads to insurance provider providing same policy at lower rates to PolicyBazaar's customer. Lower policy rates attracts more customers to the platform which leads to further aggregation of data and so on and so forth.

Its a forever loop that runs on data.

The stuff FinTech Dreams are made of

A lot has changed since 2008 when PolicyBazaar was first founded, it has launched new products, transformed itself from a simple insurance price comparison website to a web aggregator of insurance policies, forayed into credit and loans business via PaisaBazaar, started and shut operations for a health insurance aggregator (DocPrime) to now (in June 2021) securing an insurance broking license for itself from IRDAI (Insurance Regulatory and Development Authority of India) which allows it to sell life and general insurance polices offline in addition to the online business.

PolicyBazaar doesn’t carry any credit risk on its books nor does it underwrite any insurance on its own. It acts as a broker between customers and other insurance providers, helping its customers with a variety of insurance related services.

Below is a brief history of PolicyBazaar as a company presented in the form of a timeline.

PolicyBazaar's ambitions from here are growing.

The firm is raising more capital through its IPO than it has raised in all of the previous funding rounds from a dozen private investors put together.

The total IPO size is around ~ $810 Million which is a combination of fresh issue and offer for sale from existing investors. Of this total ~ $810 Million, around $500 Million is fresh issue. To put this in context, the start up has raised about $716 Million since its inception in 2008, it has only used about $50 Million of that money.

The company still has about ~$250 Million of cash on its books.

This existing cash combined with the fresh issue for $500 Million from IPO and some debt will give the company roughly about ~$1 Billion of capital, to deploy in new areas of growth.

PolicyBazaar's DRHP lays out this growth plan in exquisite detail.

Broadly the growth plans can be clubbed into five board categories.

Build an Offline Presence

Go after Small and Medium Scale Enterprises and Build Corporate Clientele

Build new offerings including a health tech platform

Pursue International Expansion

Venture into neo-lending via PaisaBazaar

Lets explore them in detail.

Building an Offline Presence and Onboarding Corporate Clients

The bulk of capital raised via IPO will be utilized by PolicyBazaar to build an offline presence. This is a strategic and important move on part of the company. Even today, India's insurance industry is only 10% Digital and 90% Offline. PolicyBazaar already has 90% market share of the digital segment.

To grow further it needs to capture the offline segment otherwise the company risks becoming a large fish in a very small pond.

The company aims to set up 200 physical retail outlets across the country in all city tiers by end of Fiscal 2024. Today, it has less than 15 physical stores. So in the next 3 years, PolicyBazaar is looking to grow its physical stores by almost 14 times to arrive at a total of 215.

These stores will provide service to end customers in local languages and develop a network of sales staff that can sell insurance policies to end customers, help them process claims and provide support whenever required.

In a sense PolicyBazaar is moving away from its digital roots to become an omni channel insurance and credit platform.

This move helps PolicyBazaar increase its customer base and start catering to small and medium scale companies as well as to other corporates. In the corporate and business segment, average premium value per policy is higher, there by allowing PolicyBazaar to capture a larger pie of the overall business. Having secured an insurance broker license, it can now also foray into providing group health insurance for these corporate customers - a market valued at Rs 25,000 crore per year.

An example of corporate insurance is Acko providing Health and Accident Care coverage to delivery partners of Zomato. PolicyBazaar can follow the same model and provide insurance coverage to delivery partners of Swiggy, Delhivery, Dunzo etc.

Having disrupted the online segment, the company is preparing to disrupt the offline segment.

This growth won't be easy though. There are dozens of new age startups along with traditional players already in this segment and each has their own war chest prepared to go after this market.

Of all the new age competitors in this space, the moves of Digit, Paytm and Acko are the ones PolicyBazaar will be watching out for.

New Offerings - A Health Tech Insurance Platform

As mentioned earlier, corporate health insurance is an yearly 25,000 crore market which remains largely run by traditional insurance providers. PolicyBazaar new broking license allows it to go after this segment and most likely we will hear about an acquisition announcement maybe just a few months after listing of the company.

The company's DRHP points to this specific acquisition target in detail.

This segment of market will be a significant addition to its customer base and should serve the second lever for growth along with the increasing offline presence. India's Plum Insurance is the neo age start up in this space and if I have to speculate - this can be PolicyBazaar's target mentioned in its DRHP.

It will be interesting to see if PolicyBazaar is able to scale up this segment of business successfully after the acquisition. It tried to venture into this space with an earlier venture called DocPrime - which was eventually shut and sold off as it was burning more cash than it was generating.

Pursue International Expansion

Growth area number three for PolicyBazaar is expanding its services internationally. The company currently has a small presence in Dubai and UAE. Part of proceeds from IPO will be used to scale up its business in Middle East along with foraying into South East Asia.

South East Asia is a very competitive market though with Chinese companies like ZhongAn and PingAn already having tie ups with existing local players.

The intent to go after this market shows the seriousness and development curve of PolicyBazaar. Its no longer is an Indian insurance start up - it wants to become a global FinTech giant and is taking its first steps to move in that direction.

PaisaBazaar - Neo Lending

PaisaBazaar accounts for about ~30% of revenue pie for PolicyBazaar. Its the platform developed to help customers avail loans. If you have ever applied for a loan in India you know how cumbersome the entire process is - endless trails of documents and constant back and forth dilutes the entire experience.

PaisaBazaar was launched to change that. Just like with its PolicyBazaar platform, the company has leveraged data to build this platform too. Customers usually come to PaisaBazaar to avail the free credit report and in process provide valuable data to the company for free. The company then uses this data to target customers for various offers in segments like - credit cards, personal loans, home loans, business loans and micro loans.

For a home loan for example, the company provides document pick up service and one representative for the customer to talk and work with during the entire loan application process.

Small steps like these, to improve the overall customer experience helps PolicyBazaar retain a customer to cross sell products later.

Using data, PaisaBazaar was able to come with with innovative products like credit card backed by Fixed Deposit and a Step Up Credit Card - for users with no previous credit history. All of these innovations are possible only via the use of data which lets PolicyBazaar understand which set of customers posses more risk compared to others.

PaisaBazaar now wants to use this data to repeat its success of credit card with loans. There is a large segment on Indian population that doesn't have access to credit because they are underbanked. PaisaBazaar wants to change that and help meet unfulfilled credit needs of customers across geographies and income levels.

Industry Trends - Bite Sized and Niche Insurance

Insurance industry around the world is moving away from traditional insurance policies towards a new concept of Bite Sized Insurance. These are small ticket insurance policies that cover very specific risks. For example, ZhongAn - the Chinese Insurance giant derives a bulk of its revenue by offering ecommerce shipment insurance to its customers.

Under the policy, if for whatsoever reason the customer receives a broken or incorrect ecommerce shipment, they are protected for the value of the product and get a full refund from the insurance company. The company today has 400 Million customers and has sold over 10 Billion policies.

Another segment that is on the rise is niche insurance, for example, pet insurance policies.

These are policies that aren't provided by traditional insurance companies and are only possible via the data collected by Insurance Tech companies.

I expect PolicyBazaar to eventually foray into these segments as well, mostly cause its competitors already have. Ola for example provides ride insurance policy in collaboration with Acko. Toffee Insurance, provides cycle theft insurance and fitness insurance policies. Digit too has come out with home content insurance, targeted at people who are living on rent and want to protect their belonging but not the structure of the house.

Insurance Industry in India

Penetration of insurance in India is abysmally low.

Only about 28% of Indian Adults are covered under life insurance as opposed to 92% of the population in US. Even in Health Insurance, only 34% of Indians are covered as opposed to 100% of population in France.

Property insurance is non existent - when was the last time you heard someone taking a home insurance policy along with their house purchase?

The only two segments of insurance that seem to be doing well are - crop (27%) and motor insurance (81%) - both mandated by government regulation.

As of FY20, India's insurance industry was worth $102 Billion (measured in Total Premium) and this expected to grow to $520 Billion by FY30. This represents an overall industry growth rate of 17.8% per year.

Within this, Life Insurance is growing at a faster rate (18.8% CAGR) compared to Health Insurance (15.3% CAGR) and General Insurance (13.5% CAGR).

There is a lot of scope and opportunity for all players to grow in the industry as insurance remains highly underpenetrated throughout the country.

Risks to PolicyBazaar

The grass in PolicyBazaar's garden is not all green. There are lot of risks associated with the company as well. The biggest of them is its insurance partners leaving the platform.

Today, PolicyBazaar has 51 insurance partners that it works with and the company doesn't have any exclusive or binding contracts with these partners. At any point in time, these partners may choose to leave the platform and chart their own route.

This recently happened with HDFC Ergo and LIC pulling its products from the platform. Limited players in India have license to conduct insurance business in India - if PolicyBazaar loses a major chunk of the big ones - it will lose its ability to deliver products to its customers.

The contribution of revenues from four largest partners was 30.82%, 35.11% and 32.81% for 2019, 2020 and 2021 respectively.

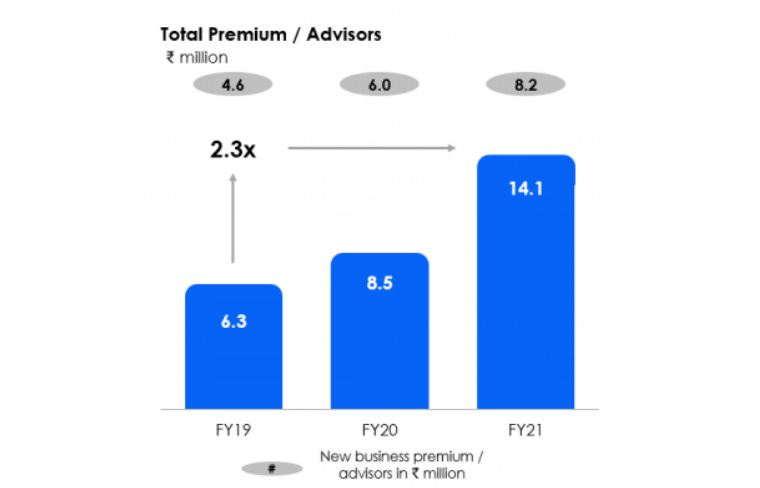

The company however has so far helped its existing partners increase the total premium transacted on its platform at a CAGR of 42% in last three years. With foray into offline segment, this growth rate should inch higher for the next three years.

Another area of risk for the business is the excessive financial regulation. IRDAI is a very strict regulator and any mishap by the company in this segment can attract large fines from the regulator. Cyber crime is also a bigger headache for the company as it has sensitive financial and insurance related data of its customers.

Being a financial business, it is closely linked with growth in the economy. Any events that hamper this growth will adversely effect the business too.

Covid and the RBI Moratorium, for example, reduced PaisaBazaar's revenues drastically in Fiscal 2021 as lending partners weren't able to issue new loans at the same rate as before.

Closing Notes

Based on the history of PolicyBazaar, previous growth rates and where the entire insurance industry is heading, I am quite confident that this business will continue to grow and march forward. Their foray into international geographies along with offline segment marks the beginning of a major milestone for the company.

What PolicyBazaar has achieved since its inception is maybe just a fraction of what it aims to and could achieve in future.

Just like its founder, Mr. Yashish Dahiya, this business is impatient, persistent and bent on continuously reinventing itself to grow further.

Sources

PolicyBazaar DRHP

Insurance Tech Report by Boston Consulting Group

My Notes

See you in the next one.

Tar

Quite an overview Tar

Post the pandemic, India is going through a watershed moment for health insurance. Companies like Pazcare & Healthysure (https://www.healthysure.in) are doing wonders in the space of group health and players like Turtlemint and Renewbuy are differentiating against policybazaar with an alternative agent led model.

Great Article Tar. Beautifully explained the market, new entrants & the risk.

There’s a great influx of new tech startups in insurance and specifically in the health insurance space in India, primarily influenced by the pandemic impact, and partly by the government policies. More companies like LoopHealth & Onsurity are offering similar group health plans like that of Plum. Companies like even & Bright Plan (https://www.brightplan.in) are offering health plans for individuals in this space.