How to Invest in International Equities?

A guide to invest in International Markets from India

Disclaimer: No part of this article is investment advice, please consult a financial advisor before investing.

Over the last decade, International markets have outperformed the returns over domestic ones.

Nasdaq100 (US Tech Index) has increased 1200% since its last bottom in March of 2009. Other US indices like S&P 500 and Dow Jones Industrial Average (DIJA) have yielded similar returns to their investors. In other parts of the world, like China this growth is even higher.

We live in a globalized world, consume global products and services and yet continue to only invest in domestic stocks. If you fall under this category, you're not alone. Majority of investors worldwide exhibit this behavior known as home country bias.

Home Country Bias is a behavioral finance phenomenon which states that investors have a tendency to favour companies from their own country over those from other regions even though by investing globally they may reduce the risk in their overall portfolios.

As the awareness about global brands and services increase, investors are rapidly overcoming this bias and gaining exposure to international equities. In India too you can witness this growth with the emergence of mutual funds that have exposure to international markets and various startups launching new products to invest in global equities directly.

This article will help you understand everything you need to know before investing internationally - the charges, taxes, legality and the various options of platforms available to you.

Is it Legal?

The most frequent question I get asked over at Twitter about investing internationally - is it legal?

So let me answer that first - yes, its legal.

Reserve Bank of India (RBI) allows every Indian citizen to remit upto USD 250,000 internationally every year. What that means is that every year you can invest or transfer upto ~Rs 1.8 crore (1 USD = 75 INR) anywhere in the world from India.

You can use this money to buy a house in United States or you can transfer this amount to a US based broker to invest in stocks or you can just spend all of it on a trip to Disneyland - its your choice. The limit is USD 250,000 per year in either case.

This policy of RBI is called Liberalized Remittance Scheme or LRS. There are a bunch more associated regulations with this scheme, you can read all about them here.

What are the options available to invest?

With that out of the way, lets look at the options available for an Indian individual to invest internationally.

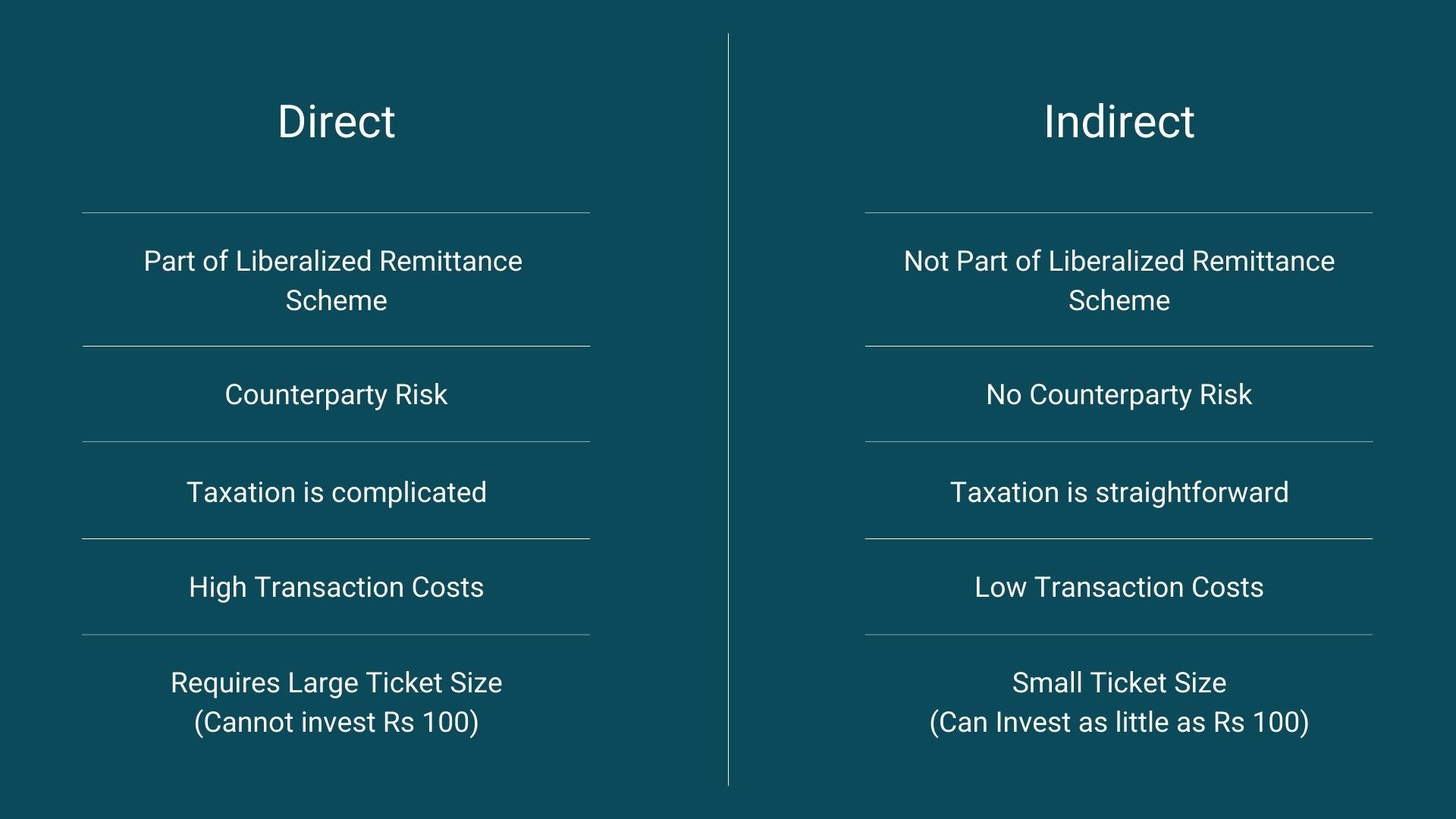

There are two ways you can get exposure to international equities - Direct and Indirect.

Direct is by investing directly into single stocks similar to how you will buy a stock of a domestically listed company from your Indian brokerage account. We will discuss the details of this later in this article.

Indirect is by investing via mutual funds that allow you to invest either in an international index like S&P 500 or Nasdaq 100 or have a portfolio that holds international stocks.

An example of the latter is Parag Parikh Flexi Cap Fund - that has exposure to international stocks like Facebook and Google in its portfolio.

Benefits of Indirect vs Direct

There are several benefits of indirectly investing in international stocks vs direct investing. Indirect investing is hassle free, straightforward and ancillary costs to invest are much less compared to direct investing.

Though you can invest as low as USD 100, the costs associated with direct investing don't make sense for a small portfolio. While most brokerages and platforms do not charge you a lot for each transaction, the costs to transfer funds and withdraw are really high. Due to this, it only makes sense to invest directly, if you have a sufficiently large portfolio and each investment is greater than at least Rs 1 Lakh in value.

I have laid out these charges and ancillary costs for each platform further in this article.

With that, lets first discuss the various Indirect options (mutual funds, index funds) available to invest today.

There are three types of Mutual Funds that let you gain exposure to international markets:

International Index Funds

Feeder Funds

Domestic Mutual Funds with exposure to International Stocks

International Index Funds

These are funds that invest into an ETF that tracks international indices like Nasdaq 100, S&P 500 or HangSeng (Chinese Index). An advantage of these funds is that you can invest via SIP with amounts as small as Rs 100. The entire process is similar to investing in a domestic mutual fund with expense ratios on these funds being quite reasonable. This route of investing is the most affordable and convenient way to add international exposure to your portfolio.

E.g. Motilal Oswal Nasdaq 100 Fund of Fund

Feeder Funds

These are mutual funds that have a partnership with a larger international fund. These domestic mutual funds serve as feeder funds to the larger parent fund. Their purpose is to collect capital from domestic investors via lumpsum or SIP routes and send that capital to the parent fund to invest and manage along with the larger fund. The expense ratios on these funds are slightly higher than international index funds and its important to investigate and understand the holdings of the parent fund before investing in these feeder funds.

E.g. Edelweiss Greater China Equity Off shore Fund

Taxation on both International Index Funds and Feeder Funds are as below:

Short Term (Less than 36 Months): Gains taxed as per your Income Tax slab

Long Term (More than 36 Months): 20% tax on gains with Indexation Benefits

Domestic Mutual Funds with Exposure to International Stocks

Some domestic mutual funds do invest into select international stocks as part of their investment portfolios. These are again a very good way to gain international exposure. Some of these mutual funds have outperformed the broader index and have consistently ranked among top performers over a 5 year and 3 year period.

E.g. Parag Parikh Flexi Cap Fund

Taxation on these funds is more straightforward and in line with other domestic mutual funds.

Short Term (less than 12 months): Gains taxed at 15%

Long Term (more than 12 months): Gain taxed at 10% on returns over Rs 1 Lakh

How to invest directly?

There are several ways to invest directly, each with it own set of complications and benefits. Each of these options have associated charges with them - withdrawal fee, deposit fee and transaction fee being the most important ones.

Let's explore each of these options and associated fees in detail.

Traditional Brokers (HDFC, Axis Bank, ICICI, Kotak)

Traditional Brokers, like HDFC, Axis, ICICI and Kotak Securities have tied up with various investing platforms to bring international investing to their clients.

Each traditional broker has a partnership with a different platform and as such have very different structure of fees and charges.

ICICI Direct Global (partnership with Interactive Brokers)

ICICI Direct has a partnership with a US based brokerage firm called Interactive Brokers.

A major advantage of ICICI Direct is that you can invest in pretty much all major markets around the world including but not limited to, United Kingdom, United States, Germany, Japan, Singapore and Hong Kong.

The fees and charges for each of these markets is different and can be accessed here.

Another major advantage of ICICI Direct is that your deposit and withdrawal process is relatively easy if you have an ICICI Bank account.

If you're someone who has a large portfolio (>1cr) and wants to invest into direct stocks globally in all major markets than this is the best option available for you.

HDFC Securities (partnership with Stockal)

Just like ICICI Direct, HDFC Securities has partnered with another platform called Stockal.

Unlike ICICI Direct, HDFC and Stockal's platform only lets you invest into US listed equities. The process to deposit and withdraw is seamless and online if you have a HDFC bank account and there are no minimum deposit or account opening charges.

Below are the charges for HDFC + Stockal's offering.

Axis Bank (partnership with Vested)

Like its peers, Axis Bank too has partnered with a platform called Vested to bring its customers the option to invest in US listed equities. Like HDFC's offering, Axis's offering too lets you invest in US stocks only.

Here are the charges for Axis + Vested's offering.

I personally, am not a fan of Vested's offering since they charge for Account Opening, have significantly less number of stocks available and have higher withdrawal fees compared to their peers.

One area where Axis + Vested wins over its peers (ICICI, HDFC) is the 0% brokerage on any transactions.

If you're someone who has a small ticket size and will not withdraw often then you may consider this option.

Kotak Securities (in partnership with Interactive Brokers)

Like ICICI, Kotak too has partnered with Interactive Brokers to allow its clients to invest globally.

The key difference between ICICI's offering and Kotak's offering is:

Unlike ICICI, Kotak only allows to invest in US listed equities. You cannot invest in other markets like UK, Singapore, Germany, Hong Kong and Japan.

Kotak's base plan is cheaper than ICICI's on a per trade basis. While ICICI charges you USD 2.75 per trade on its base plan, Kotak only charges you USD 1.99 per trade on the base plan.

If you wish to have exposure to only US stocks and have a significant corpus to invest then this maybe the right option for you.

Standalone Offerings

If you do not wish to open an account with these banks then you can directly open an account with any of the service provides these banks have partnered with. The charges in this case may differ and you may be charged an account opening fee along with other host of fees.

Links to these platforms are mentioned below.

New Age Broking Platforms

Other than the above options, you may open an account with a new age broking platforms like Groww and IND Money.

Both these platforms are mobile first - they have made significant investments into UX/UI and their app design, investing and account opening experience is as easy as downloading their app.

Both these platforms do not charge any fee - no account opening fee, no withdrawal fee, no transaction fee. Your bank will however charge you a deposit fee to remit money internationally to the US based brokers these apps have partnered with. These remittance charges vary based on your bank and are fixed irrespective if you transfer USD 100 or USD 100,000.

I personally use Groww and it has so far served me well. I like the UX/UI and the entire process to remit, place orders and monitor positions is easy and user friendly. The offering for Groww is currently limited by invitation only - you can use this link to secure your invite and receive Rs 100 as a reward to open your account.

Taxation for Direct US Investments

Finally, lets understand the taxation aspects if you wish to directly invest into US equities.

Broadly, there are two types of taxation

Taxes on Investment Gains

Any gains on your investment will be taxed in India and will not be withheld in United States. The amount of taxes you pay, depends on the length of your investment.

Short Term (less than 24 months): Taxed according to your income tax slab rate Long Term (more than 24 months): Taxed at 20% with indexation benefits

Taxes on Dividends

Any dividends received by you on your investments will be directly taxed in the United States at a flat rate of 25%. United States and India have a Double Taxation Avoidance Agreement, under which you can avail this tax paid as Foreign Tax Credit and can use it to offset any income tax payable in India.

Risks and Recommendations

Risks

If you choose to invest directly into US equities you should be aware of the major risk, i.e., these investments are not held under your name by the US Broker but under the brokers name.

Unlike in India, where stocks are held under individual's name by the Depository Participant, in the US, stocks are held under the broker’s name by the Depository. The broker in turn maintains a record for each individual and this information is not privy to the depositories.

So in the unlikely scenario, the broker goes bust, you are likely to lose your investment above USD 500,000. This USD 500,000 limit is the federal insurance limit under which all registered brokers in the United States are covered. You may read all about it here.

So if you have investments of more than USD 500,000 you may want to consider this risk before investing.

Recommendation

Here are my recommendations for different types of investors.

ICICI Direct Global - For a serious investor with large corpus who wants to invest in global markets not limited to just United States

Kotak Securities - For an investor with large corpus who wants to gain direct equity exposure to US stocks only

Groww - For the new age investor who wants to invest small amounts and gain small exposure to US Stocks

Index Funds and Mutual Funds - This route of indirect investing, is suitable for 99% of investors who do not want the hassle of added taxation, or want to pay additional fees

I personally use a mix of Mutual Funds, Index Funds and some single stock names via the Groww platform to gain exposure to Chinese and US markets.

In today's world, portfolios need to have global exposure to participate in the growing international markets. As discussed in this article, there are many options available to invest and choose from - ranging from low cost index funds to sophisticated platforms that let you invest in multiple markets. I hope this cleared any doubts related to investing internationally from India.

Until next time.

Peace,

Tar

Very informative

Hi Tar,

I am bit confused on how indexation works on LTCG tax for international mutual funds. Could you please explain or guide to a good resource?

Also, the article is very helpful. Thanks.