In the world of finance, calculating and assessing risk is more important than assessment of returns. If you’re able to accurately determine risk associated with an investment, you can to a large extent accurately determine the returns.

It is for this reason, banks have over the years tried to categorize and formulate risk in the form of credit scores or rudimentary human driven processes and questionaries that can some how help them identify ‘true risk’ associated with grant of a loan.

These primitive methodologies designed in late 1980s are still prevalent around the world and used by major financial institutions to disburse trillions of dollars in loans.

All this in the age where your social media feed is decided by an algorithm.

Why can’t the same technology that drives your social media feed be used to improve the process of determining risk associated with grant of individual loans?

Three folks at Google in 2012 asked the same question and decided to start a company to solve this very problem. Ten years later, their company is valued at over $10 Billion.

This is the story of Upstart.

Before we proceed, please consider sharing this write up with your friends or on your social media.

My aim, through these write ups, is to reach out to as many people as I can, so that they can make informed financial decisions.

Part One: What is Upstart? 🤖

Upstart is an ‘AI’ driven credit lending platform.

If you are a professional data science practitioner like me, you know Artificial Intelligence does not exist. When companies like Upstart advertise themselves as AI driven, what they really mean is that they have several proprietary machine learning algorithms working together to execute a certain task.

In case of Upstart, its the combination of several machine learning models that work together to help identify and define true risk.

True risk in case of lending is identifying the probability of default on a loan.

Therefore, Upstart is a Machine Learning driven platform that helps identify true risk and leverages this proprietary technology to helps banks offer more loans at reduced risk when compared to other traditional models like credit scores.

The Heart of Upstart ❤️

At the heart of Upstart, lives its machine learning driven risk model.

To develop a successful machine learning model, you need three things:

Data Variables: Think of these as your columns in a spreadsheet with each column defining a characteristic of a borrower, i.e. education, income levels, age, number of dependents etc.

In 2014, Upstart started with 32 of these variables, today it has over 1600 and this count is only going to increase from here.

Data Count: The above variables mean nothing if there is no actual data present for them. Think of data count as rows in a spreadsheet. The larger the number of rows, the more data Upstart models can consume and more accurate they can become.

Upstart has over 9 Million+ of these data points and all of these come from the actual real world data Upstart gathers from the loans that originate from its platform.

Learning Algorithms: The final piece of our puzzle is a learning algorithm. A learning algorithm is bunch of coded instructions that over time modifies itself to learn from the data supplied to it and gets better at the task required from it.

In Upstart’s case, the main job of a learning algorithm is to predict the probability of default for a loan.

In 2014 Upstart started with two basic learning algorithms. Today it has over 16 different models that feed into each other trying to predict everything from probability of prepayment, default, income fraud, identity fraud and interest rate optimization.

This is where things get exciting.

This part of the article is very important to understand the competitive advantages of Upstart later, so please bear with me if it gets too technical.

In the domain of machine learning, there are two main types of learning concepts - supervised learning and unsupervised learning.

Think of supervised learning as a teacher teaching you in a class. You’re given very specific instructions to follow and your job is to follow them as accurately as you can.

Unsupervised learning is when that teacher doesn’t give you any instructions whatsoever but instead tells you what the answer should be. Your job is to figure out the instructions required to arrive at the answer accurately.

The way unsupervised learning works is the algorithm learns from previous ‘experiences’ and gets better at the job required from it automatically.

I will let the below video help you understand how unsupervised learning works in real life. In the video there are two unsupervised learning algorithms competing against each other in the game of hide and seek.

Both algorithms job is simple, one has to get better at hiding and other at seeking. Watch till the end to understand how dramatically these algorithms can improve themselves without any additional input.

The learning algorithms and data Upstart collects from its platform are its biggest competitive advantages. Over the years, Upstart has been busy trying to remove all human elements from these learning algorithms while making sure they stay true to their purpose - to identify true risk.

“We are in the process of removing all human based involvement in decision making. There is still a lot of work to be done and until 2016 we were just building the foundations of our model. We are trying to automate every corner of our codebase that isn’t machine driven today and we are confident that over time we will be able to achieve that.” - Paul Gu, Co-founder and SVP, Upstart

What started as a simple binary classification model is now a combination of several automated learning algorithms that feed off from the real world credit data and make each other better.

Over time the improvement in the output of these algorithms at Upstart will be more dramatic than any financial analyst at Wall Street can predict today.

This inbuilt competitive advantage is also evident in Upstart’s business flywheel shown below.

More Data → More Sophisticated Models → Higher Approvals of Loans

The Problem to Solve 🧮

Upstart’s mission is to ‘enable effortless credit based on true risk’.

Four in five Americans have never defaulted on a loan yet almost 50% of them have credit scores that wouldn’t qualify them for a low interest rate loan. This gap in lending is the problem Upstart is trying to solve.

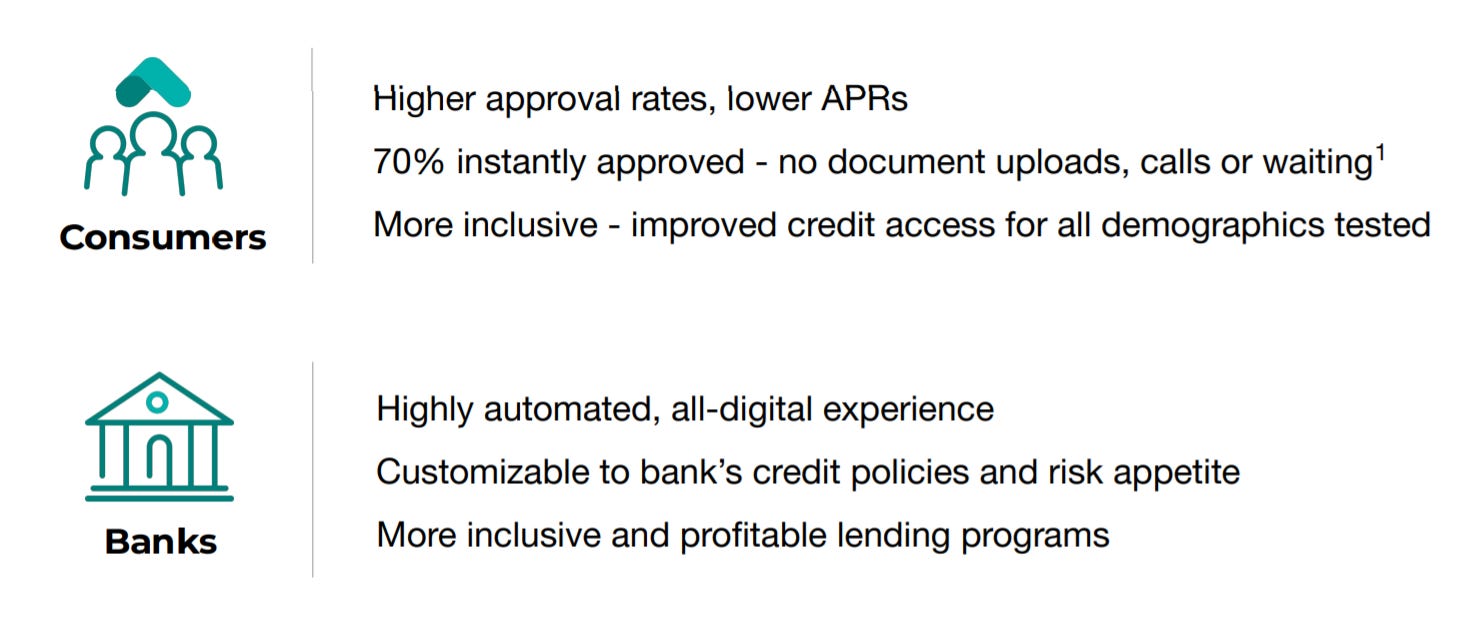

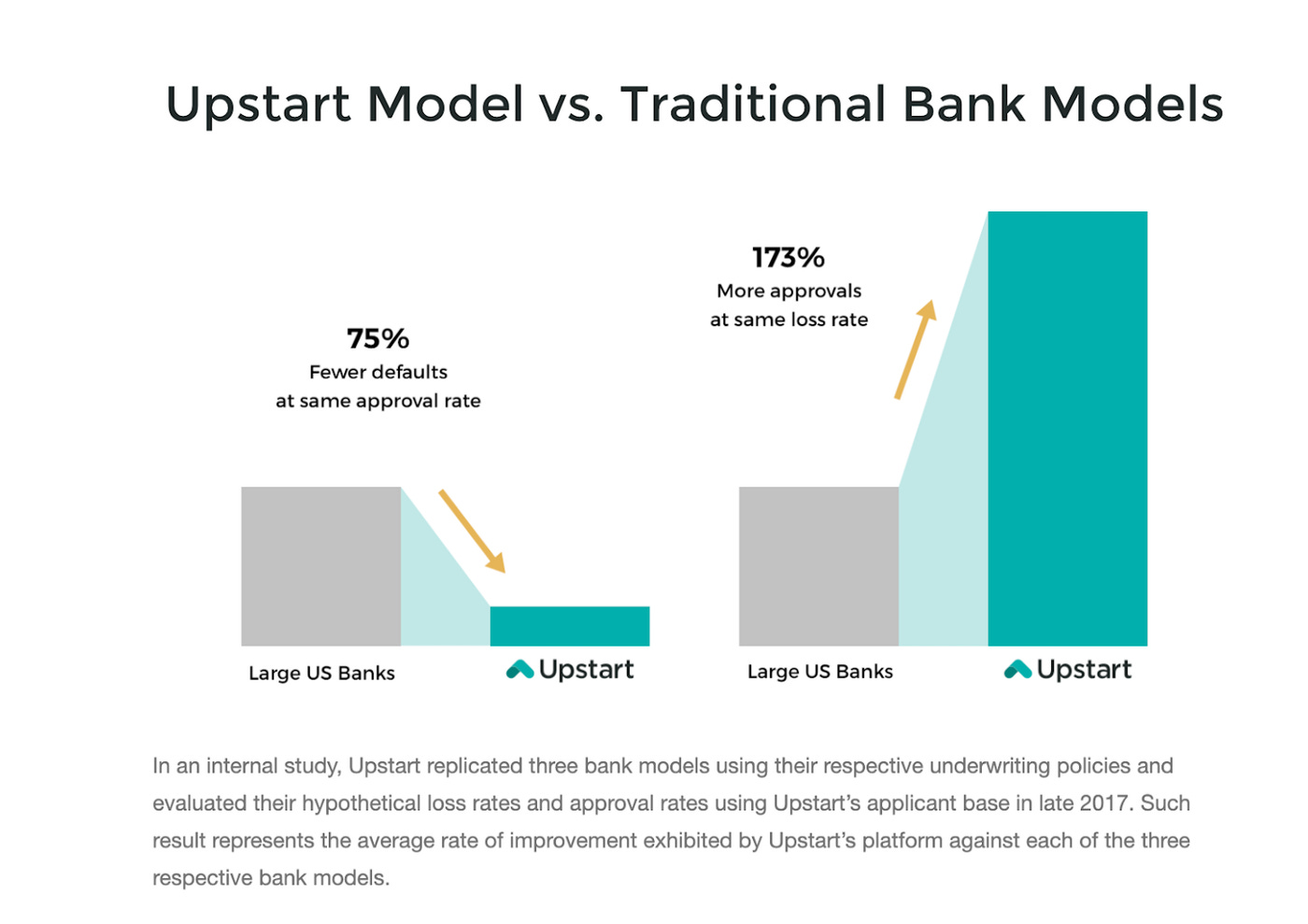

By leveraging data and machine learning techniques Upstart can more efficiently estimate ‘true risk’ than traditional models ever can. Upstart’s model lead to a 75% reduction in loss rates for banks while increasing the conversion rates by 10x.

By estimating risk better, Upstart’s bank partners can disburse more loans at much lower risk profiles, while consumers can avail these loans at cheaper interest rates.

A win-win scenario for everyone.

Upstart, in essence, has built a better mouse trap - one which banks can use to approve more loans while controlling their risk and driving default rates lower.

How Upstart makes Money? 🪙

Upstart is a two sided platform - on one side they market and create a funnel of prospective loan seekers via their website Upstart.com and on the other hand they have 40+ bank partners that can either choose to underwrite these loans directly from the Upstart’s website or opt in to create a white label solution of Upstart’s platform for their own customers.

Upstart makes money primarily three ways.

Referral Fee: This is usually 3 to 4% of the loan value charged to banks whenever a successful loan transaction is made via Upstart’s platform.

This segment makes up for majority of Upstart’s revenue, representing over 94% of Q4 FY21’s revenue.

Platform Fee: This is a fixed dollar fee per loan charged to banks for the privilege of using Upstart’s platform

Servicing Fee: This represents a fee collected from banks or institutional partners to service the loan i.e. collections, reporting etc. This usually represents 0.5% to 1% of loan value.

Upstart does not charge any fees to consumers. This revenue model works well as bank partners only pay to Upstart if they are using the platform while consumers do not pay anything.

A logical question to ask here now would be as to who is underwriting these loans?

The answer is - its a mixed equation.

When Upstart enters into a product category they usually underwrite a small percentage of loans (2%) to get the ball rolling. Majority of loans are underwritten by its 40+ bank partners which have the privilege to later sell these loans to Upstart’s 100+ institutional investors like Goldman Sachs, JP Morgan and Morgan Stanley.

Upstart doesn’t want to take any credit risk on its balance sheet and doesn’t want to compete with banks either. It’s goal is to help banks adopt technology and seek Upstart as their primary lending technology partner.

Part Two: Financials, Risks and Valuations 📈

Financials 🏦

Upstart’s revenues have grow at a blistering pace since its public listing. Revenue each quarter has increased in triple digit percentage when compared to previous year.

Q4 of 2020 for example, Upstart did around $87 Million in topline. The same quarter in 2021, topline was $305 Million representing a 252% year over year increase.

The primary driver behind this revenue growth is the increase in the loan transaction volume on Upstart’s platform. Transaction volumes in Q4’21 were up by ~230% when compared to Q4’20.

As Upstart gains more recognition and becomes a brand, these transaction volumes should increase further.

While the topline is increasing, bottom line too is showing signs of improvement. Upstart’s contribution margin has been increasing from mid 30’s to now 52 percentage points for the latest quarter.

Contribution margin represents how much money Upstart makes from the transaction volume on its platform.

Risks 🚩

Lending is a Cyclical Industry

The biggest risk to Upstart’s revenue projections is that it works in a cyclical industry that is bound to follow the ebbs and flows of the larger economic outlook.

When economy is thriving, credit and lending demand is sky high and banks feel comfortable in underwriting a larger portion of loans. When economy is in a recession, credit demand is at its lows and banks tend to be more risk averse.

Since, Upstart’s revenues are directly linked to loan transaction volume on its platform, its revenue will take a hit whenever the state of the economy turns. With inflation running sky high in US and Federal Bank increasing interest rates, it is possible that US economic growth slows down to an extent in the near term.

Concentration of Loan Book

While Upstart has 40+ banking partners on its network, a majority of loans originating from Upstart are underwritten by a single bank, Cross River Bank. While the dependency on Cross River Bank has reduced over the years from 83% of all loans underwritten in 2017 to 60% of all loans underwritten in 2020, it still represents a large chuck on their loan underwriting volume. If Cross River Bank were to pull back tomorrow, it would represent a sudden liquidity crunch on Upstart’s platform.

Upstart has been onboarding other small and medium sized banks (their target area) to improve liquidity and reduce dependency on any single banking partner. A typical bank partner onboarding process for Upstart takes anywhere between six to fifteen months, so going from 40 to a 100 banking partners will take some time.

Concentration on Customer Acquisition Funnel

While Upstart has been trying to market itself and establish a standalone brand name, a major chunk of its customer funnel comes from a single source - Credit Karma, a loan aggregator website.

The concerning part is that even though Upstart has increased its marketing budget by several times in the last three years, the percentage of customers acquired via Credit Karma and dependency on it has increased from 28% in 2017 to almost 60% in 2020.

While this is not of immediate concern, if Credit Karma were to shut down tomorrow, Upstart would lose a part of its major customer acquisition funnel. This dependency highlights the importance for Upstart to build and control its own customer funnel and establish itself as a brand.

Valuation and Earnings Triggers 💰

Earnings Triggers 📊

Until recently Upstart was a single product company and was present only in the market of personal loans.

They are now slowly expanding into other lending verticals namely - Auto Lending, Small and Medium Scale Business Lending and Mortgage Lending.

Each vertical has a larger market than personal loan business. To me, Upstart’s foray into personal loans was just a proving ground and having built a successful business there, they can blitzscale the learnings from personal loan business and apply to scale up auto, business lending and mortgage businesses.

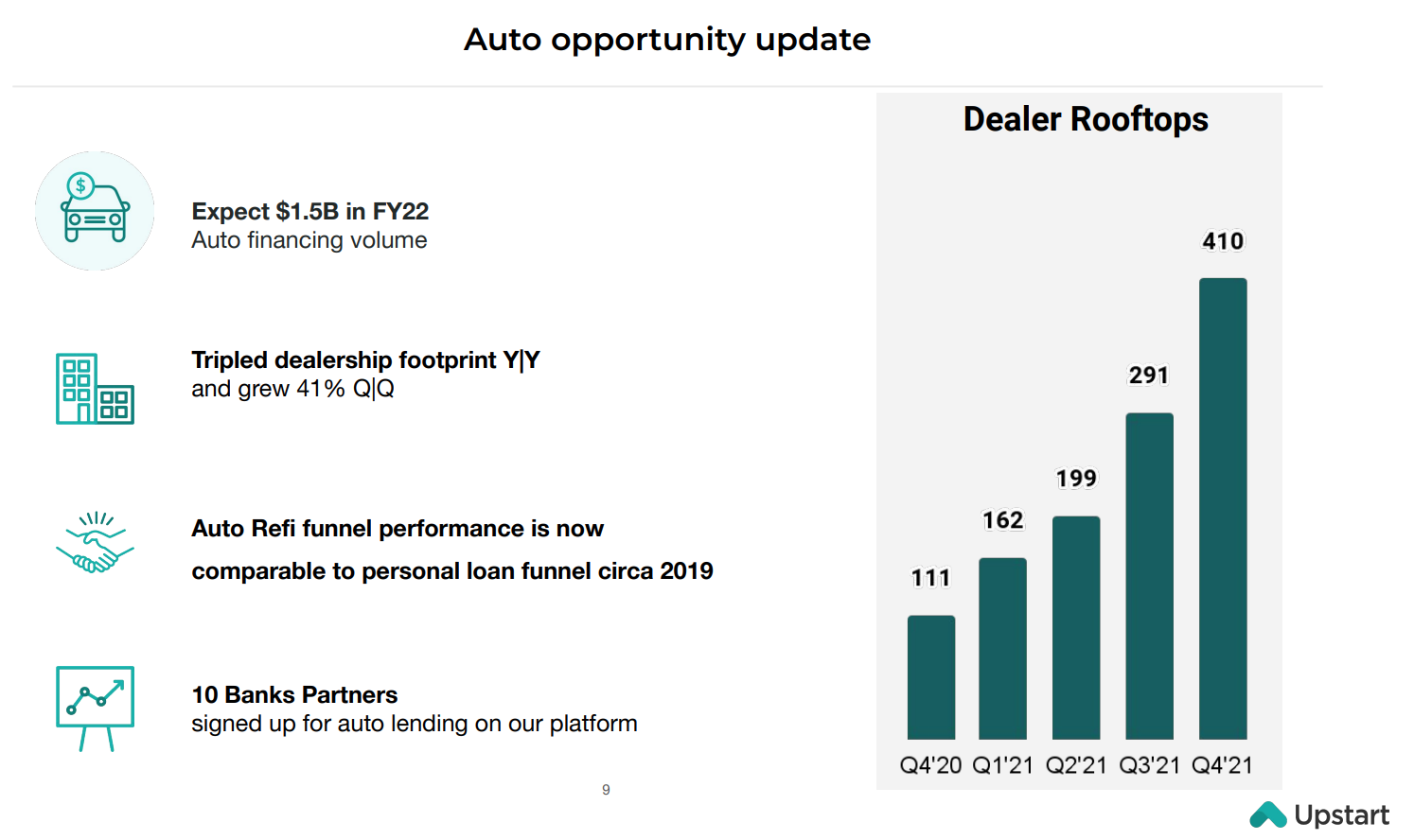

Auto Lending is the first market they are targeting for 2022 and this is our first major earnings trigger.

From the capital they raised from IPO, Upstart acquired Prodigy Software, a provider of cloud based automotive retail software to auto dealerships. Upstart later rebranded Prodigy Software to Upstart Auto.

“While Amazon and Shopify have modernized the online shopping experience, the auto industry has been left behind. Upstart is on a path to reduce the cost of auto financing, and we can accelerate this opportunity with a modern multi-channel purchase experience.” - Dave Girouard, CEO, Upstart

Leveraging Upstart Auto, Upstart wants to help dealers in US manage and sell cars while also providing auto financing options through the Upstart platform. Their target for 2022 is $1.5 Billion in transaction volume from Upstart Auto.

Upstart Auto has already started showing signs of taking off. Earlier this month, in March 2022, world’s largest car manufacturer Volkswagen, announced its partnership with Upstart to modernized its dealerships by leveraging the Upstart Auto Retail platform.

“When we started working with Upstart Auto Retail, they were an up-and-coming startup in the digital retail space. We chose them because other platforms simply did not meet our needs. Having worked with them now for so long, it has been nothing but a success story,” stated Josh Lever of Platinum Volkswagen.

“They worked with me at the dealer level and took our dealership’s needs into consideration. I cannot thank the team enough for developing such a robust product around what dealers need today.”

The Mortgage and Small and Medium Business Lending are much bigger markets than Auto, Upstart has a target of 2023 to launch viable products for the same.

Valuations 💸

Upstart’s market cap has been no stranger to volatility. Having IPO at $20 a share in December 2020 at a $2 Billion valuation, Upstart saw its share price climb to $400 at its peak valuing it at $33 Billion.

Valuations have since cooled off and entered a realm of reality. Upstart today, as of writing this article is valued at ~$10 Billion which is a 7x NTM Price to Sales multiple.

In my view this valuation is much more reasonable but doesn’t represent a bargain with a margin of safety.

In the spirit of full disclosure, I do have a position in the company at $78 per share and I will look to slowly increase my position as and when the share price presents a reasonable value.

Part Three: Conclusion 🏁

I believe Upstart to be one of the true FinTech companies of our generation. The leadership team is strong, mission motivated and they have clearly build a product that helps all the users on its platform.

The opportunity and market size is large enough for Upstart to become a $100 Billion player and still not represent a large percentage of the market. Their technology is hard to replace with high barriers to entry and applications around the world.

Being a professional data science practitioner who loves finance, its exciting for me to see a company leveraging and applying the great parts of machine learning and cutting edge developments in this field to the world of finance.

What do you think about Upstart? Let me know in the comments below.

Thank you for reading, see you in the next one.

Peace,

Tar

Insightful. Thanks Tariq for the great work.

Awesome read only heard about upstart now having read this seems like a great fintech