The Business of Sterling & Wilson Solar ☀️

Turnaround or a Mirage?

Our story begins in 1927, old Bombay, particularly Meadows Street or Angrezi Bazaar.

Shapoorji Pallonji Mistry Sr, the son of Pallonji Mistry and heir to the Shapoorji Pallonji group, was furious. No one in Angrezi Bazaar seemed capable enough to fix his electric iron - an coveted item of luxury in those days.

Just when he was about to give up, he came across Meherwan Daruvala, who ran a small electric shop in Angrezi Bazaar, called Wilson Electric Works. Just like Shapoorji, Meherwan too belonged to the enterprising Parsi community of Bombay. Unlike Shapoorji though, Meherwan came from humble means. While the Mistry’s started their business in 1865 and by 1927 were synonymous with the likes of Tata’s, the Daruvala’s were just getting started.

Impressed by Meherwan’s work and abilities, the two soon struck a friendship. That friendship eventually translated into a business relationship when their sons (Pallonji Mistry and Yazdi Daruvala) formalized the partnership by acquiring 51% stake in Wilson Electric Works. It was then, the name ‘Sterling’, from the Mistry’s family investment firm Sterling Investments, was added as a prefix and so birthed the company - Sterling & Wilson Ltd.

That business relationship has survived almost a century across generations of family members and has led to construction of iconic projects like the Taj Mahal hotel in Mumbai (the electric work was done by Sterling & Wilson, constructed by Shapoorji Group and owned by Tatas), the Sultan Qaboos Palace in Oman, the Reserve Bank of India building and the World Trade Center at Cuffe Parade, Mumbai, among others.

In 2019, Sterling and Wilson, demerged and listed its solar EPC business on the National and Bombay Stock Exchanges.

This, is the business of Sterling and Wilson Renewable Energy.

Part One: Current Business of The Company

Sterling & Wilson Renewable Energy is primarily into the business of setting up large scale renewable energy parks, comprising of mainly solar, wind and battery energy storage systems. The firm, is an engineering, procurement and construction contractor also known as an EPC contractor.

Engineering, Procurement, and Construction (EPC) businesses provides comprehensive turnkey solutions for large-scale projects by combining engineering design, procurement of materials, and construction services under a single contract.

In an EPC business, a company (EPC contractor) is given the responsibility to execute, manage and build a large project. One of the most well known EPC firms in India is Larsen & Tubro, which also happens to be one of the largest EPC companies in the world.

The above graphic highlights various stages of an engineering, procurement & construction (EPC) contract. In some markets, procurement of raw materials function is part of the EPC business and is included in the contract, while in others the client procures and supplies the raw materials.

Another key part of EPC lifecycle is the Operation & Maintenance stage, also known as O&M. Operation & Maintenance is the higher margin, low risk and long sticky revenue business and in most cases is granted to the same company building the project.

The above is a detailed yearly revenue breakup for Sterling and Wilson Renewable Energy from its listing year (2019) to present.

At the heart of it, its a simple business.

You want to build a large solar plant? → We know how to build them → In return for a fee, we will build one for you → and post build, we will even maintain it for you for a yearly fee

But this simple business comes with a myriad of challenges, some of which nearly bankrupted Sterling & Wilson several times.

What are turnarounds?

Before we proceed any further, lets first learn what are turnarounds in investing. To explain turnarounds, here is the legendary Peter Lynch.

As Lynch explains, turnarounds are stocks that went through a tough business phase leading to accumulation of losses, high debt and are most often ignored by the market.

What makes them a turnaround stock, is a trigger - usually an internal change in the way business is performed or a takeover by a new management.

There is a popular market saying, “Turnarounds seldom turn”, which means that most turnarounds fail but when they do succeed they can be humongous wealth generators.

In Indian market there are several recent examples of successful turnaround companies.

Companies like RACL Gear Tech, which was a bankrupt business once, was taken over by a new management, the stock since has returned 20x, or Sangam Renewables which was another failing solar EPC business before being taken over by the giant Waaree - the stock has since returned a massive 175x.

The key questions to ask in turnarounds are:

What is the trigger that leads to change in profitability of the business?

How close or far away is that trigger?

Is the debt on balance sheet manageable?

How much of the debt is due in the short to medium term?

Is there any real evidence in the company’s financials indicating a turnaround?

In the next sections, we will explore the answer to some of these questions.

Part Two: The Past & The Present

Before we begin to understand the triggers for the company, we need to explore what went wrong and the events that led to Sterling & Wilson Renewable Energy to where it is today.

The Global Dominance

When Sterling & Wilson Renewable Energy started its operations in 2011, there was a single mission - to become the largest Solar EPC player in the world.

By 2019, right around the time of IPO, Sterling & Wilson succeeded in achieving this mission - but that success came at a cost.

At the time of IPO, the company had projects across almost every major solar geography - Middle East, Africa, Australia, Americas, South East Asia. If there was a large solar project in any part of the world, the company was there to bid for it.

Sometimes even at unfavorable terms.

The demand for solar projects in India was thin, solar and renewables were yet to take off and across the borders in Middle East - the oil kingdom was doling out orders to construct many Gigawatts worth of solar projects vs few Megawatts in India.

Sterling & Wilson was present to bid for all them, even constructing the largest single site solar project in the world, at the time.

Unlike India, which is a Balance of System (BoS) market - where procurement (primary equipment, i.e. solar modules) is the responsibility of the client instead of EPC company.

The contracts Sterling & Wilson was signing on, included everything.

For a fixed contract price - Sterling & Wilson would do everything from procurement of materials to building the required project in very specific time period. This meant that if there were any cost overruns due to delay in construction or increase in price of raw materials etc., the company had to bear all of them from its own pocket, further putting pressure on the tiny single digit EBITDA margins.

Now to Sterling & Wilson’s credit, finishing projects before the due date was a norm in the company and as far as raw materials were concerned - cost of solar PV modules was falling for more than a decade driven by technology advancements, increased demand and giant capacities in China.

Something must have to really go wrong at multiple fronts for the company to incur losses in these projects. You know, like the world would have to shut down, everything would have to come to a standstill, Chinese govt would have to stop granting subsidies to new solar capacities and solar PV module production in China would have to come to a complete halt for several months at a time.

The possibility of all these events occurring at the same time was so miniscule, the company never thought to protect itself from it.

The probability so tiny, such an event would almost never occur.

Almost.

#AD

If you like this write up, please do consider supporting us by subscribing to our paid weekly market newsletter called #TheWrap🌯.

By subscribing to the TheWrap, not only you get a data portal and highly curated market insights, but you also enable us keeping such deep dives free for everyone else.

Below is a short video that explains #TheWrap🌯 in detail. Hope to see you as one of our subscribers.

#End of AD

2020: The World Locks Down

As the pandemic raged across the world in 2020 and most of 2021, Sterling & Wilson found itself in an increasingly tough spot. Unable to work at most sites due to shortage of workers or lockdowns, combined with increasing prices of solar modules and other necessary equipment, the company was forced to concede and call ‘force majeure’ on most of its contracts.

Force majeure is a legal concept that refers to unforeseeable circumstances or events beyond one's control, such as natural disasters or acts of God, which may exempt parties from fulfilling their contractual obligations.

This cancelling of contracts led to a barrage of lawsuits as clients didn’t want to pay up for unfinished work. To Sterling Wilson’s credit, the circumstances under which these contracts were signed in 2019 or before, were suddenly very different in 2021. To their client’s credit, Sterling Wilson should have protected itself better by foreseeing and demanding specific clauses to be enabled in these contracts.

Every EPC business works on very thin margins and as such opts for short term working capital loans to fund itself. When client’s of Sterling Wilson opted not to pay, it had to default on these loans triggering a downward spiral of its credit ratings, which made future borrowing more expensive.

It also increased legal costs for the firm by many folds, as client sued, creditors sued and Sterling Wilson sued them back.

It was the start of rough times for the company.

Between 2019 and financial year ending 2023, the company’s revenues dropped by 75%, from 8240cr in 2019 to just 2015cr. Further, the company went from positive operating margins of 8% to reporting negative margins for the next 10 quarters.

The pandemic had added Sterling & Wilson to its long list of business fatalities.

Amid rising debt, low funds and increasing litigation, the promoters of the company looked to sell 40% stake to shore up funds and found their white knight in Reliance.

On February 9, 2022 Reliance New Energy, a subsidiary of Reliance Industries purchased a 40% stake in Sterling & Wilson at 375/share for a total of ~737.5cr.

2023: There is Light At The End of The Tunnel

In the week of 17th July 2023, Sterling & Wilson’s posted its Q1FY24 results with first indication of positive gross margins. That week, the stock price went up by ~27% with volumes higher than last 658 days.

The market took it as an early signal that maybe the tough phase for the company was ending. The litigation cases were increasingly coming to their closure with the company winning most of them. Lenders were able to agree on terms to refinance loans at higher rates and the troubled legacy order book of the company was increasingly being replaced with domestic orders.

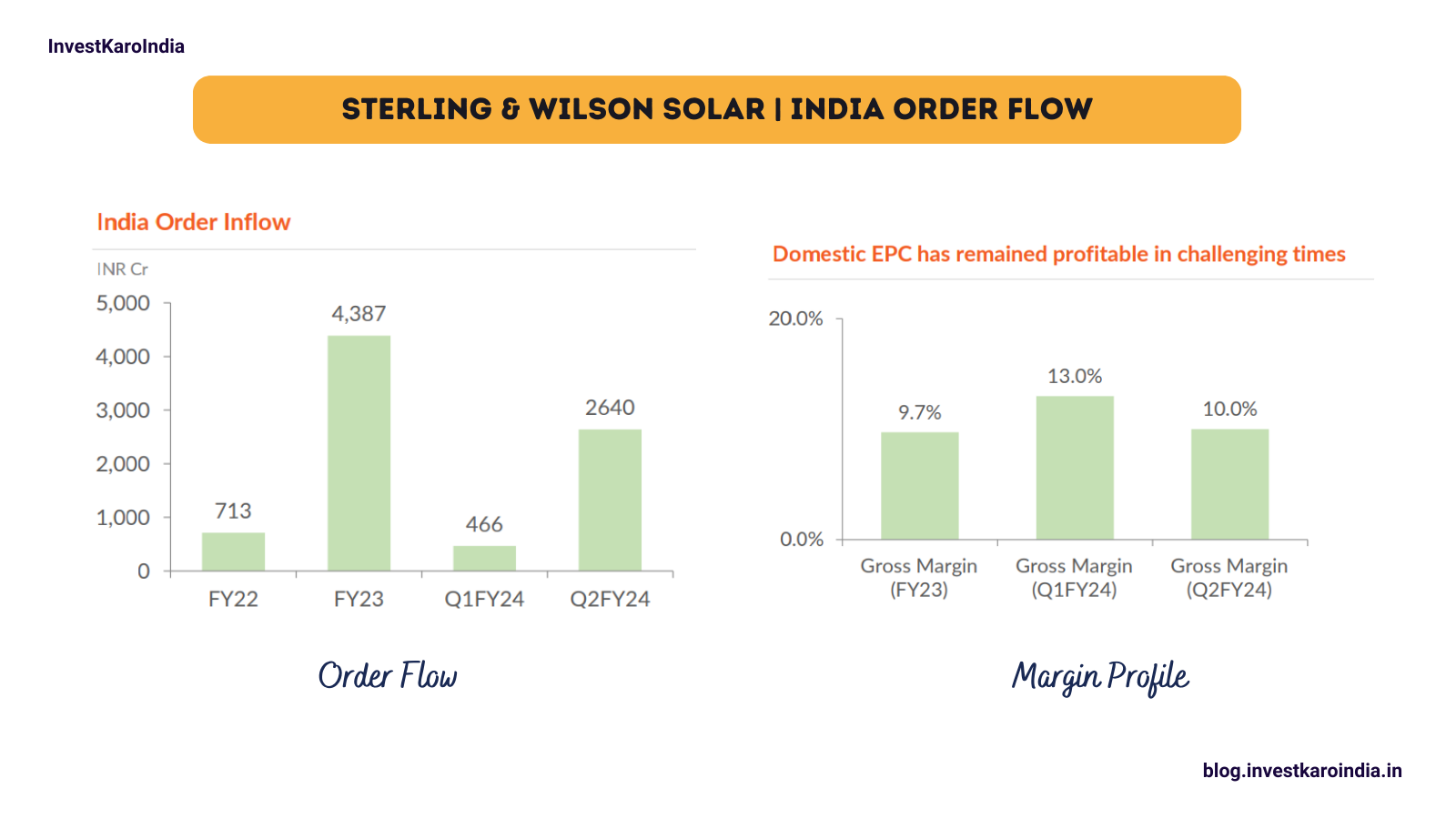

Indian solar market too had drastically changed since 2019. The government’s push for increased solar in total energy output of the country meant that very large orders were now being granted by most public sector undertakings with an overall ambitious goal of reaching 400 GW worth of solar capacity by 2030.

Today *(Oct 2023), the company’s order book comprises of 98% domestic orders - which has always been profitable even during the tough phase from 2019 to 2023.

In its latest quarterly results, the company has achieved profitability on a standalone basis, though remains loss making on a consolidated basis. The losses however have been narrowing.

Most of these losses, stem from the legacy international order book for the company that is still loss making. As the revenue from profitable domestic orders gets increasingly recognized in financial statements, the consolidated financials should also turn profitable.

Even in its international business, the only major new large deal worth over a billion US dollars is for a US govt funded project in Nigeria. It is expected that the deal will be profitable and as such in due course, the international EPC part of the business should also turn profitable on a standalone basis.

With a good understanding of the past and present state, lets now turn our attention towards the current challenges facing the company.

Part Three: Challenges & Triggers

The main challenge (and its a big one) with the company today is that it is short on funds. As of month ending September 2023, the company had only 55cr in its bank account with total debt at 2,123cr.

That’s a lot of debt!

The past three years of troubled phase and losses have led to accumulation of this debt at pretty high interest rates.

The per quarter interest expense has increased nearly 3 times to now at 64cr. Combine that with the lumpy cash flow nature of the EPC business and shortage of funds in bank and you can see why the company defaulted on its short term loan payment in September 2023.

To shore up liquidity the company and turnaround, the company is focusing on below areas.

Fund Raising of 1500cr

The company will raise 1500cr via equity issue in November 2023 in order to strength its balance sheet. Some of these proceeds will be utilized towards short term debt payment while others would be put towards working capital as the company increasingly bids for large upcoming domestic orders.

Now, issuance of equity isn’t that great for minority investors like you and me as it leads to dilution of ownership and more shares in the market but without this fund raise and further capital infusion, I doubt the company will remain viable as a going concern.Collect due indemnity payments from promoters

The promoters of parent company, Sterling & Wilson, owes the company upwards of 400crs which is due in November 2023. The company has asked the promoters to repay earlier so that it can pay back the 135cr amount it defaulted on in Sep 2023.

These dues relate to the indemnity agreements signed between the three promoters (Mistry’s, Daruvala’s and Reliance) of the company.Focus on a Business Turnaround

As the company wins increasingly large orders in domestic market, it is also gaining up on efficiencies. Most of these large projects are centered around key geographies which enables the company to deliver more at lower costs as they are able to utilize equipment and personnel much more effectively.

Further, the company is also focusing on increasing the share of higher margin O&M business by bidding for third party O&M contracts.

Optionalities

Very large orders like those of Nigeria and upcoming ones from promoter Reliance, should bode well for the company in driving revenue, cash flows and ultimately profitability.

Part Four: Risks & Valuation

Risks

There are several risks in the company as of today, some of these are listed below.

Fund Raising: Needless to mention, all future liquidity hopes of Sterling & Wilson Renewable Energy are dependent on the upcoming successful fund raising of 1500cr.

Any hiccups with this would mean short and medium term issues for the company.

Time to Turnaround: As Peter Lynch mentioned in the video earlier, timing with turnaround is of utmost importance. Through the company’s last two quarter’s financial we can devise that margin and profit trajectory are in right direction, the debt alleviation plan remains to be seen.

Various Promoters: The company effectively has three promoter groups, the Shapoorji group, the Daruvala’s and Reliance. While Reliance is the largest shareholder, the board chairman remains Khurshed Daruvala. There are six board seats with Reliance being represented by 3 and remaining 3 distributed between Daruvala’s and Mistry’s. When you have too many cooks at the helm, there is always a chance of things going awry.

Future Funds: Like all turnaround, here too, the future funding of projects and business earnings depend on current business turning profitable. If the company fails to turn profitable in the next four quarters, it may lose out on the lucrative bidding window of several large PSU projects.

Valuation

The company is valued at the bottom of the pile and as if it was going to fail - which isn’t something out of the ordinary for turnarounds. The stock price has remained in a pretty tight range for most of its listing history.

Technically too, the stock is at its major support zone and any fall in prices below 245 should be worrisome.

Conclusion

“Fast cars and turnarounds are not for the faint hearted”

Time will tell whether Sterling & Wilson’s story that started in the alleys of Angrezi Bazaar in Mumbai will come to an end or will the last three year will be but a small hiccup in an otherwise almost a century old story of the company.

Like all turnarounds, you have to be careful and consider every tiny detail as an investor.

In case of Sterling & Wilson Renewable Energy, there is a light at the end of the tunnel. Today, as an investor you do not know, whether that light is a speeding train hurling towards you or an opening to an oasis.

I hope this write up helped you understand the business of Sterling & Wilson Renewable Energy in a holistic manner. If you enjoyed reading this and have any feedback or insights, please share by leaving a comment below 👇

Thank you for reading, see you in the next one.

Peace,

Tar

Great read !!! Thank you so much for the blog

Since this day of writing it's going to be 2x soon. Diligent