The Business of Sigachi Industries ⚗️

A fast growing company with a lot of red flags!

Microcrystalline Cellulose or MCC, belongs to the category of ‘highly consumed invisible substances’. These substances are an integral part of a modern consumers life yet they tend to stay under the radar, ‘invisible’ and out of consumer’s knowledge.

You probably consumed MCC today, in the form of medicine, food or even cosmetics. Microcrystalline Cellulose, which in its raw form looks like a white powder, is derived from wood pulp and serve as a excipient in medicines, binding agent in food and stabilizer in cosmetics.

Think of it as a naturally occurring packaging material that is non harmful to humans.

So why is an investment newsletter talking about some weird powdery packaging material? Well, that’s to do with the business we will be exploring today.

Sigachi Industries is a 33 year old family run business that is one of the leading global suppliers of Microcrystalline Cellulose. The business publicly listed itself among much fanfare in Nov 2021 with listing day gains of over ~250%.

The stock price has since corrected by over ~50% and now hovers at ~INR 315/share, as of this writing.

Like most families, this business too is complicated with a lot of pros and cons. It is also undergoing a significant transformation of itself, something it has exceled at in the recent past, just before its public listing.

Through this write up, we will explore the global microcrystalline cellulose industry, get introduced to the various players operating in the local as well as the global market, explore the current financial and growth triggers of Sigachi and also look at several red flags of the company.

By the end of this article, you should be well versed with the business, that is, Sigachi Industries.

Before we proceed, please consider sharing this write up with your friends or on your social media.

My aim, through these write ups, is to reach out to as many people as I can, so that they can make informed financial decisions.

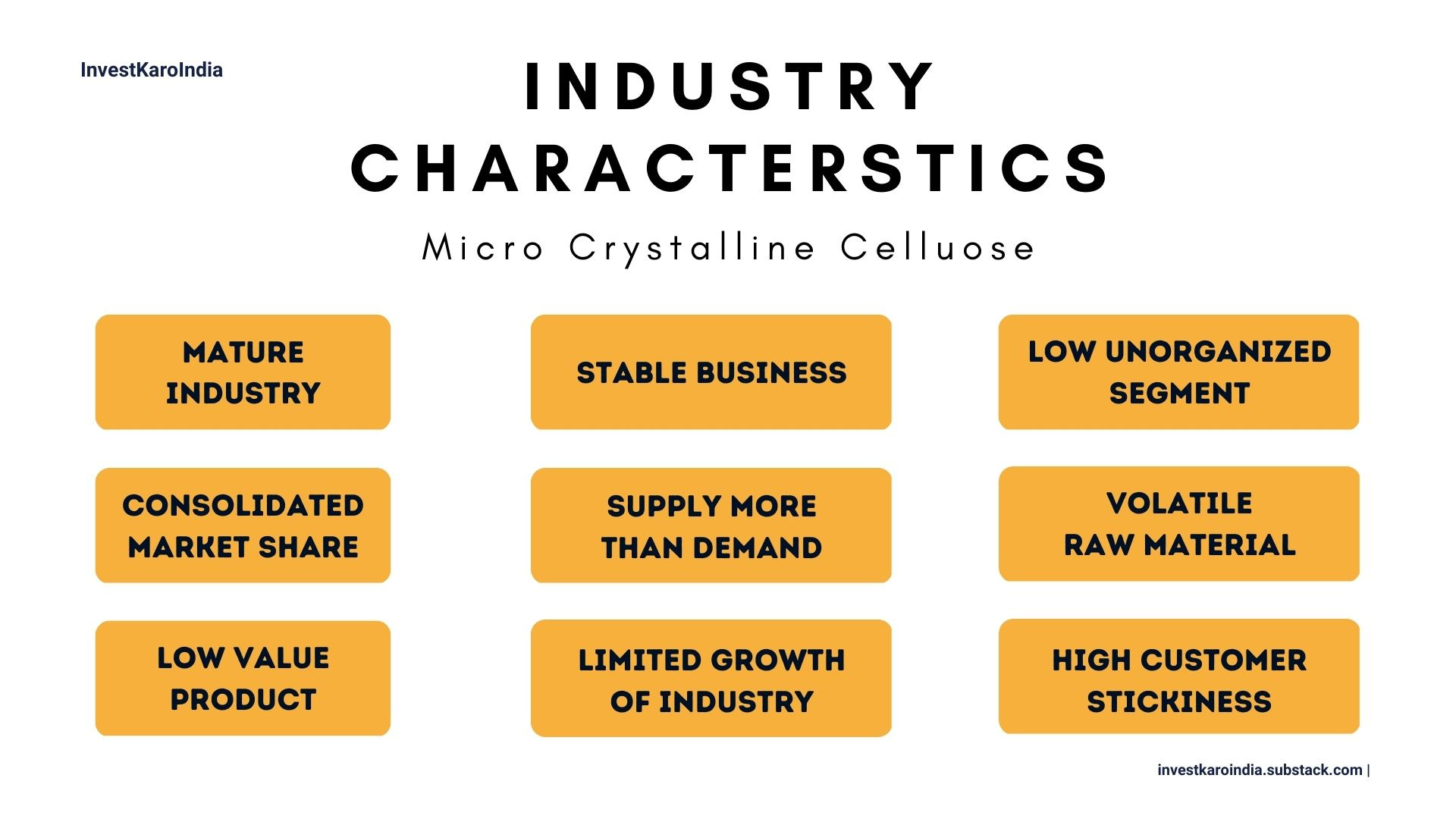

Global Micro Crystalline Industry

The global micro crystalline industry can be segregated into two major type of players - giant established corporations and everyone else. MCC as a product finds its primary application in pharmaceutical industry, which accounts for a lion’s share of the demand - currently around ~70%.

The finished product is also low value, commoditized, as such the pharma giants and other large corporations tend to stick to a single supplier of the product to ensure quality control.

Since the product is low value in nature, the producers of MCC find it relatively easier to pass on any price hikes and raw material related inflationary costs pressures. As such the margins tend to remain stable for everyone involved in the entire value chain.

The supply of MCC product always outpaces the demand due to its commoditized nature and a simple manufacturing process.

Further, regional players have a consolidated market share for their respective geographies. For example, DuPont is the primary supplier to majority of innovator pharma companies in North America and Sigachi being an outside company limits itself to generic pharma companies.

Finally, there are two major changes ongoing in the industry.

First is the shift of manufacturing from high cost locations to low cost locations like Thailand. Being a low value and thin margin product, it has become increasingly challenging for suppliers to keep manufacturing MCC in high cost geographies like US and EU.

This is evident by two facts

Sigachi and every other MCC manufacturer in the world, sources its raw materials from a high cost geography, refines and manufactures MCC in a low cost country and then sells its back to a high cost geography

Companies like DuPont (the worlds largest supplier of high grade MCC) setting up manufacturing facilities across Thailand

Second major change in the industry is the onset of ‘value added’ MCC products. The manufacturers have started producing various purity grades and types of MCC depending on the end customer usage, in order to differentiate themselves.

A value added product also helps the producer make higher margins and garner a larger wallet share from the customer.

Now that we have understood the industry Sigachi operates in, lets explore the company in detail.

Current Revenue Profile of Sigachi Industries

Sigachi has been growing its revenues at an approx. CAGR of ~20% for the last six years. The company used to do ~100cr of sales in 2018 and should be able to close this year will net sales of more than ~300cr.

Further the company’s operating margin profile has increased from ~12% to now stable at ~20% per year.

The main boost in margins have come from the R&D push by the company. It has over the years refined its manufacturing process and has been able to produce more with less raw materials, thereby saving costs and increasing margins.

Topline growth is aided by the company really sweating its assets. Sigachi has an asset turnover of ~1.2x, which is really healthy for an asset heavy manufacturing company.

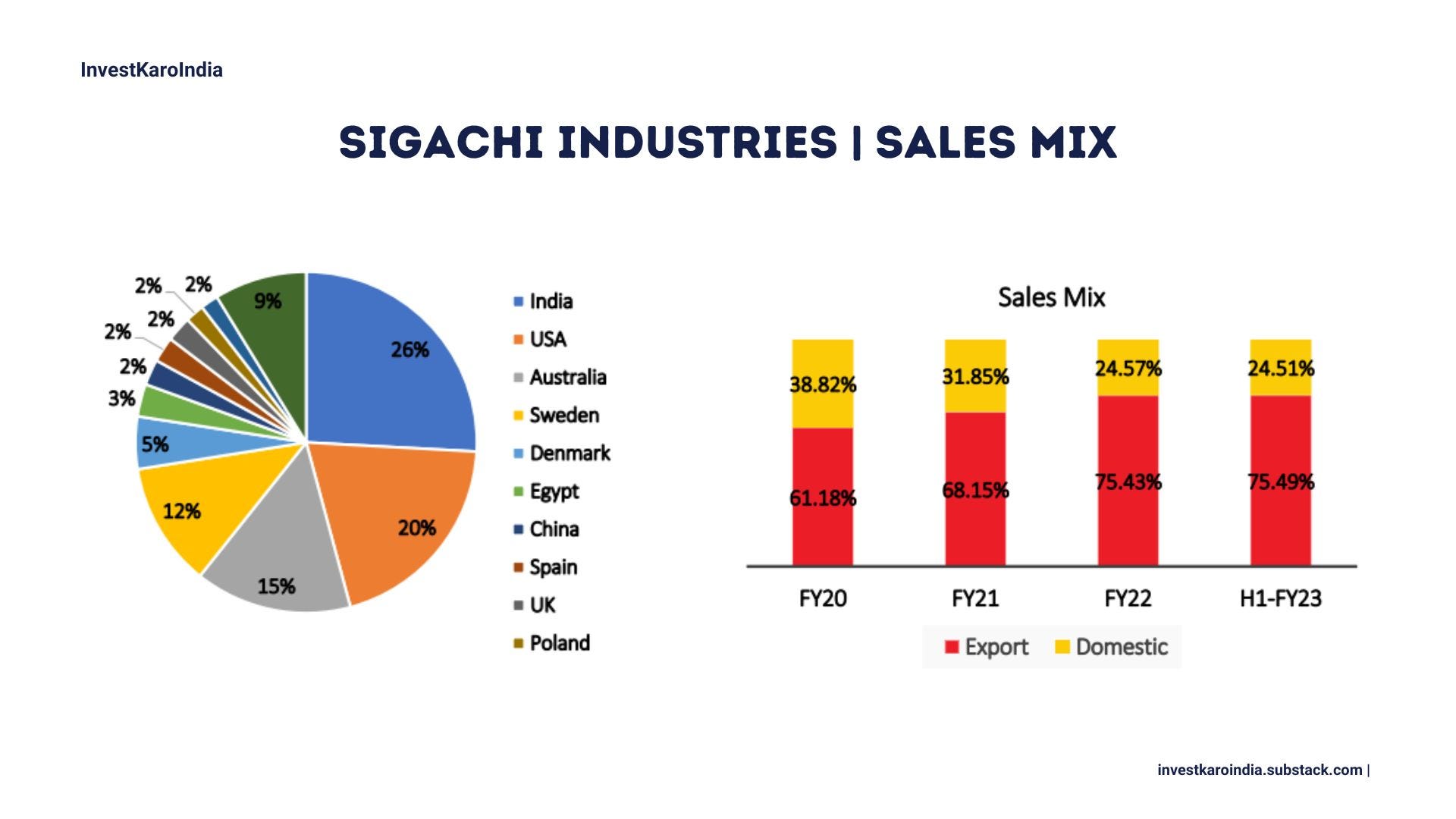

The company is primarily an export oriented firm, with exports representing ~75% of its topline and rest accounting for domestic sales. Primary customers of the company are large distributors of MCC and other pharma and food ingredients.

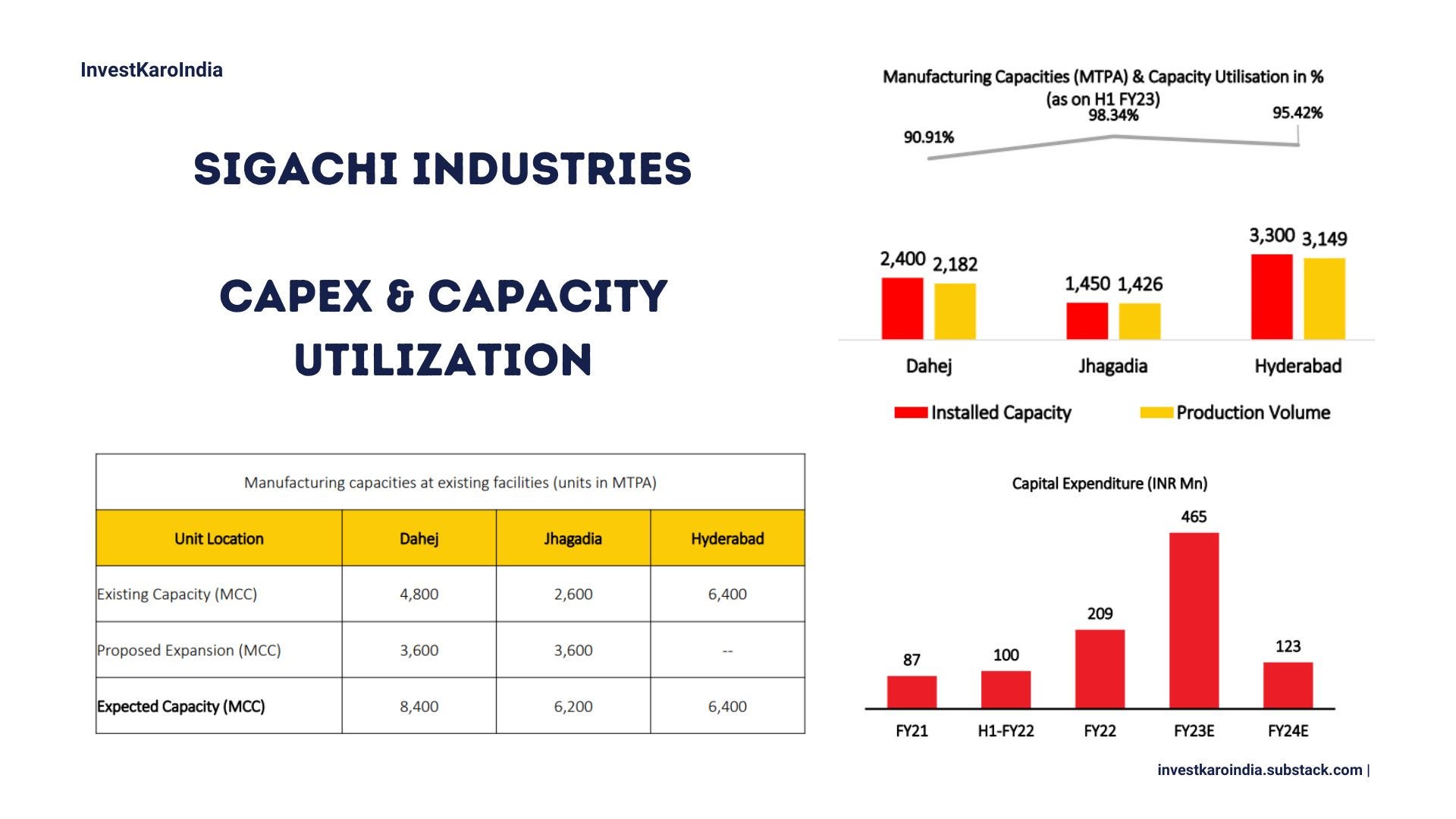

The company has three manufacturing plants spread across Gujarat and Hyderabad, with all three of them are running at above 95% capacity.

Owing to high capacity utilization, the company is expanding its manufacturing capacity by over ~50%. New capacities will come online mid 2023 and early 2024.

The company boasts healthy return ratios, with both return on equity and capital employed exceeding ~25%.

So on paper, Sigachi looks like a great company. It has a large export oriented customer base, new capacities coming online, high demand for its product, great margin profile and a fast growing topline.

But when we look a little bit deeper, several red flags start to emerge. Lets explore them in detail.

Financial Shenanigans

Red Flag #1 🚩

The Company doesn’t own its own IP

Just before Sigachi was about to IPO, the company sold all of its trademarks, brand names and even the name ‘Sigachi’ to its owners, for a measly sum of Rs 2.4 lakhs.

In return, for the privilege of using the name Sigachi along with other trademarks and brand names, the company is set to pay 1% of sales as royalty to the promoters starting 2025.

Further, this royalty agreement is only valid till 2035, post which if the promoters choose, they can reset the agreement or even bar the company from using the trademarks and any other intellectual property again.

Below is the excerpt from their IPO document that calls out this clause in detail.

Red Flag #2 🚩

The Incentive for the Promoters reside in the topline growth and not the bottom line

As a minority shareholder, your incentive to invest in the company for the long haul is a essentially a bet that the company will grow its bottom line, i.e., profit after tax. As a company makes larger profits, these profits eventually should make way to your bank account in the form of dividends.

Companies do well over time when both promoters and minority shareholders’ incentives are in sync. This is not the case with Sigachi.

Since the promoters incentive are clearly at the topline growth (owing to the 1% royalty agreement we spoke about earlier), the company has been ‘diworsifying’ into various ancillary businesses.

So far in its limited history of being a public listed company, Sigachi has

Hired consultants and then cancelled plans to open an ethanol factory

Launched a nutritional premix product range via taking a lease on a premix manufacturing plant

In process of launching a OTC healthcare segment and investing to build a domestic distribution network in India

All of the above are not related to its core business, i.e. making cellulose based excipient products.

Meanwhile, the debtor days for the company have increased from 77 days to now 88 days with receivables (credit sales) accounting for over ~25% of the overall sales.

Clearly the promoter incentives are to maximize topline in order to maximize the royalty rather than maximizing profit.

Red Flag #3 🚩

A whole lot of related party transactions

Apart from the upcoming royalty payments to the promoters, the company has been leasing properties from its owners.

Below are the few excerpts from the IPO Document.

Below are some of the properties controlled by the promoter and used by the company on a rental basis.

The company’s corporate office, manufacturing plant, guest houses all are owned by the promoters and the rent on these seem abnormally high.

Further, the company’s rental expense has increased by ~25% just in last year!

The are more red flags like abnormally high promoter remuneration, non-independence of audit committee, but I sense that you get the gist!

Lets now explore some of the growth triggers and current valuations of the company.

Growth Triggers

Sigachi has two main growth triggers ahead

A 50% increase in capacity that should disproportionately aid in topline growth

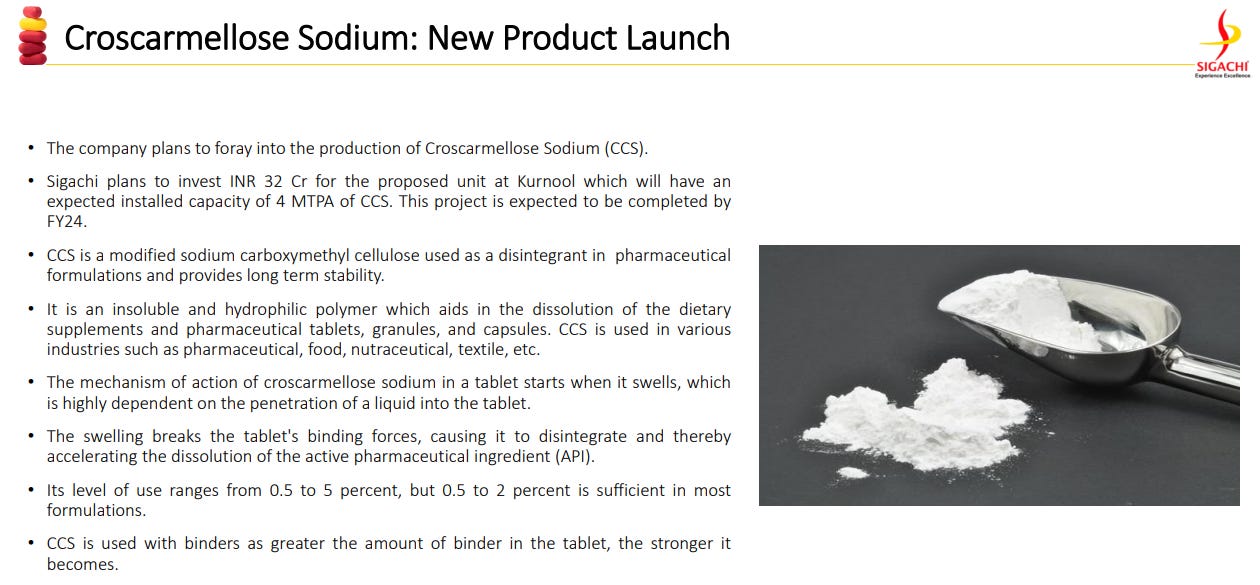

Launch of Croscarmellose Sodium or CCS as a new product

We spoke about the capex growth trigger earlier in this write up, lets explore a bit about croscarmellose sodium or CCS.

CCS is a high value, high margin product that is also in high demand by the pharma industry. It is used as a disintegrant in medicines to ensure the API in the medicine gets digested at the right time when its in the body.

This would be a new product for Sigachi and it aims to leverage its existing customer relationships to sell this higher margin product in addition to MCC.

In my view this product can easily help Sigachi maintain or even extend its margins from ~20% to ~25% range in the short term.

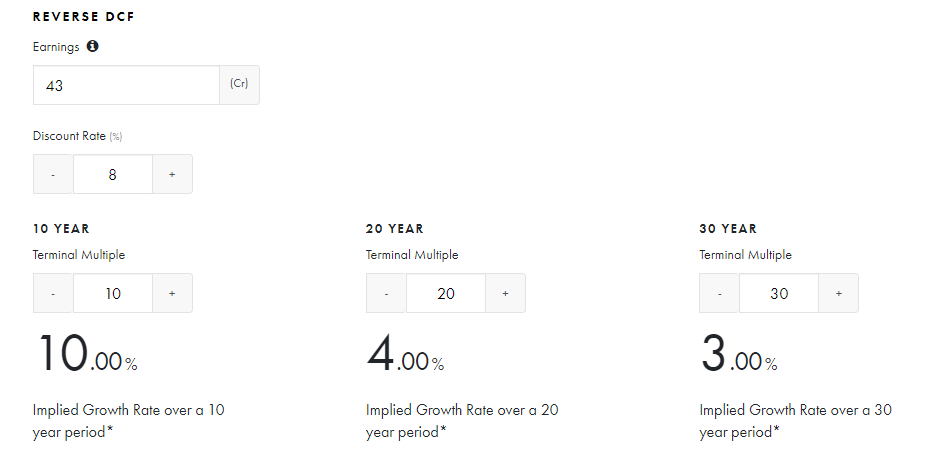

Valuations

At the current stock price of Rs ~315 per share, the market is assigning a 10% earnings growth to Sigachi.

This seems low for a company that will expand its manufacturing capacity in near term and introduce a higher margin product. The company is also able to easily pass on higher raw material and related costs to end customer, there by giving us confidence that a ~20% operating margin profile will stay.

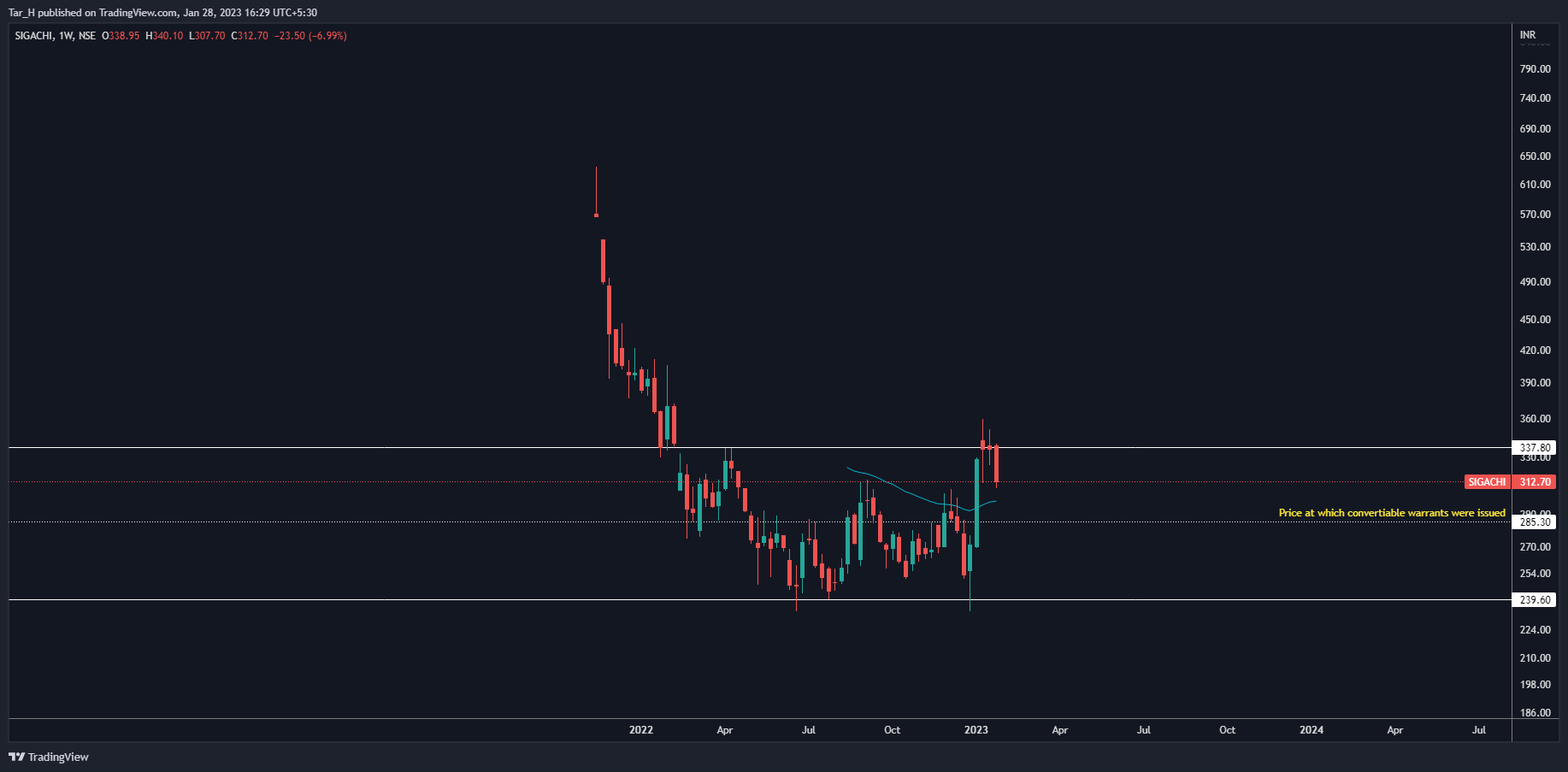

Technically the stock looks strong and has so far managed to stay well above its immediate support of Rs ~240 per share.

Maybe the market doesn’t like the long laundry list of related party transactions and royalty agreements along with the ‘diworsification’ into unrelated segments.

Conclusion

Sigachi Industries, as per me, is a typical case of a good business run by a greedy promoter. The company is minority shareholder un-friendly but at the same time has lot of earnings trigger.

Given the misplaced promoter incentives, its anybody’s guess whether the topline growth will ever translate into bottom line for the company.

I will be a trader of the stock and not an investor.

I hope this write up helped you understand the business of Sigachi Industries in a holistic manner. If you enjoyed reading this and have any feedback or insights, please share by leaving a comment below 👇

Thank you for reading, see you in the next one.

Peace,

Tar

A good detailed write up on the company

There’s a company by the name of Pracheen Chemicals based out of Gujarat who make the same products as Sigachi, namely MCC and CCS and nearly 70-75% of their revenue comes from Sigachi

So the question is raised here is does Sigachi actually make MCC at their Gujarat plants??

Because they always refuse for plant visits whenever requested

Also if you see their cash conversion is very poor, hardly any of the EBITDA is converted to OCF

Nice explanation sir.