January 20, 2020 was the date when first case of Covid-19 was found in United States. Within months Covid spread around the world and rampaged every nation. It was (and still is today) the fastest spreading disease in human history.

Why am I telling you something that you already know?

Cause, to understand the events of today, we have to understand the financial events that took place at the start of the Covid-19 pandemic.

Nations around the world weren’t prepared for an event like the Covid pandemic, and who can blame them. The last known pandemic (Spanish Flu) happened more than a 100 years ago in 1918, much before globalization and commercial air travel was a thing.

Before Covid, pandemic preparedness in the modern world was meant for medical text books. Not a single financial book ever talked about economic implications of a pandemic, much less prescribe the playbook of necessary steps required to steer the economy through one.

So when the pandemic hit in Jan 2020, Reserve Banks around the world were entering uncharted territory. By March of 2020, when the entire world shut down and everything came to a standstill, the US Federal Reserve along with US Congress took a few bold steps and announced unprecedented liquidity measures to support their economy.

Anyone who wanted to borrow money, could at dirt cheap rates.

Free stimulus money of upto USD 1200 was sent directly to every US citizen, small businesses were allowed to borrow money at extremely favorable rates, unemployed citizens were granted additional USD 600 per week in payments (~31,000 USD per year) and US Fed cut its interest rates as close to zero as possible.

The Fed had one goal at the time - to prevent US economy from a depression onset by the severe and unrecoverable destruction in demand.

By providing ease of money in an otherwise troubled economy, the Fed orchestrated the greatest financial maneuver in the history of economics. It was able to ensure the demand stays intact even though almost every major part of the economy was shut.

These moves of US Fed were replicated by major central and reserve banks across much of the western nations.

What these central banks failed to judge accurately is when to stop the pandemic era stimulus measures - and it is at this point of failure our story begins.

Before we proceed, please consider sharing this write up with your friends or on your social media.

My aim, through these write ups, is to reach out to as many people as I can, so that they can make informed financial decisions.

Part One: Too Much Demand, Too Little Supply 🏷️

Economics and finance are usually termed as social sciences. They do not have any rigid rules of hard sciences like E = MC^2 in physics or the covalent bonds from chemistry.

Most of the rules in economics are malleable and depend on the context of the situation, except one.

If demand rises faster than supply, prices rise.

If supply rises faster than demand, prices fall.

This demand and supply rule of economics, is maybe as close to a scientific rule as we would ever discover.

When demand increases much faster than supply, prices rise sharply.

This sharp increase in prices is what is termed as inflation.

The pandemic era stimulus measures helped keep the demand intact around the world but supply side of the equation deteriorated. Lockdowns across majority of the world ensured that factories weren’t running at their maximum capacity and cargo shipping lines, which carry nine out of every ten products globally, came to a standstill.

When the world slowly returned to normal, restoring these supply chains took time. The previous two decades of globalization also meant that more products move from eastern part of the world (Asia) to western part of the world (EU and North America).

These skewed trade routes led to problems like ports getting clogged, long shipment wait times and not enough labour, which contributed to the initial inflationary pressures within the global economy. These initial pressures were felt by businesses and we witnessed profit margins for majority of companies reducing by mid 2021.

Employment levels in US were still rising all through this period and as such US Fed maintained that inflation is transitory. To their credit, inflation wouldn’t have been such an issue, had it not been for two simultaneous events that twisted the global supply chain further in 2022 - the Russian War and the Chinese lockdowns.

Part Two: Grains, Fuel and Everything Else 🌾

8.5% of the global wheat supply

70% of global neon gas supply

40% of global krypton supply

46% of global sunflower oil supply

Before February 24th 2022, these stats about Ukraine weren’t common knowledge.

That changed with Russia’s invasion; overnight Ukraine took centerstage. Apart from sending supply shock to global food, semiconductor and edible oil markets, the war also destabilized the oil and natural gas markets of the world.

Russia accounts for 10% of global oil production and 8% of global natural gas production. To make matters worse, major economies in European Union, like Germany, rely a large part on Russia for their energy requirements.

Just within days after Russian invasion, global oil prices rallied 40% to hit an all time high of $138 per barrel.

Prices of oil, wheat and edible oil impact everyone in the world.

When oil prices rise, everything gets expensive.

Russia’s invasion of Ukraine was an unseen shock - even though Russia was building a military presence on Ukrainian borders for months - few expected Russia to launch a full scale invasion of another sovereign nation in Europe.

The global energy market was suddenly caught off guard.

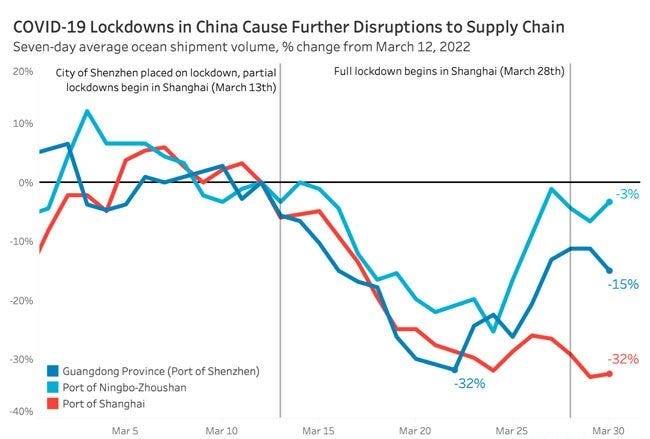

At any other time, this invasion would have been the top news across the world, but not this time. The war had barely begun, when four days later on 28th February 2022, a large scale outbreak of Covid-19 (omicron variant) emerged in the largest city of China - Shanghai.

China managed to relatively escape the wrath of Covid for majority of the last two years. As soon as pandemic emerged, the Chinese government shut down borders and isolated any cases it could find. While this helped keeping the fatality count low, it also lead to another healthcare issue.

The Chinese population at large hasn’t developed a natural immunity against Covid like the rest of the world has. So when omicron emerged, its impact was minor for majority of countries but deadly for China.

Within days of first omicron case, thousands of cases started to emerge in Shanghai followed by Beijing - two of China’s largest cities. China’s Zero Covid Policy also meant that they had no option but to lockdown these cities and along with it - two of the most important cogs in the global supply chain.

Together Beijing and Shanghai account for a large share of global supply. The port of Shanghai is in fact the busiest port of the world for almost a decade now.

With both these cities under lockdown, the already stressed supply chain of the world, squeezed even further.

These two unrelated and isolated events (Russian War and Chinese Lockdowns) contributed to the acceleration in otherwise already steady growth of inflation around the world - which brings us to where we are today.

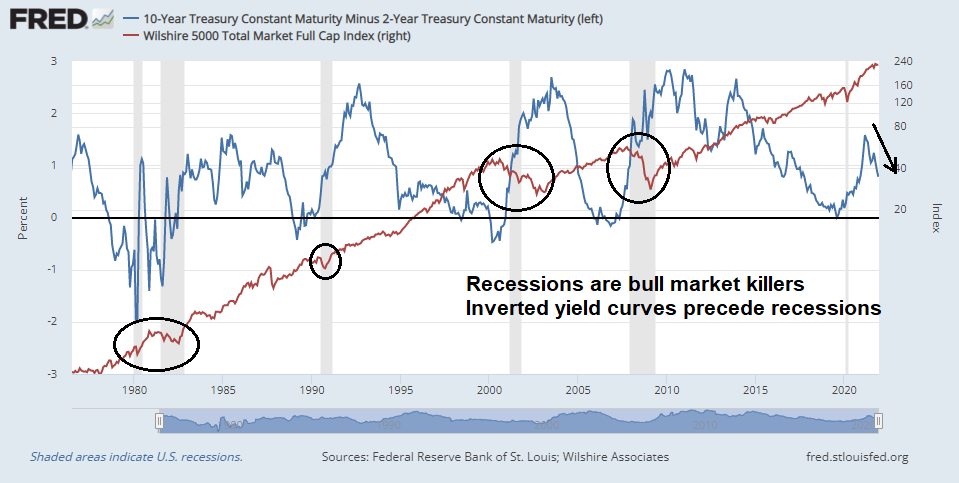

Part Three: Will there be a Recession? 📉

As I write this post, on a Wednesday night (15th June 2022), in the background US Fed is announcing the highest increase in Fed Funds Rate since 1994.

I wont get into the details of how Fed Rates impact an economy and stock market. If you want a primer on that, you can go through the below Twitter thread.

The inflation is US is at a 40 year high of 8.6 per cent against the Fed’s target of 2 per cent.

Developed economies like US do not normally have inflation 4 times their target.

The last time inflation was running rampant in US was during the early 90s and Fed then didn’t have to combat a broken supply chain along with a pandemic recovery!

Inflation isn’t just high in the US, its impacting a majority of countries around the world - a direct effect of the broken supply chains.

So when supply chain keeps getting stressed and demand is overheating in an economy, we either have to fix and increase the supply or reduce the demand for us to able to control price rise - and its effect - inflation.

Since Fed cannot really control the supply side and new production capacities along with production bottlenecks in real world take time to resolve, the only option we have at the moment is to reduce demand.

A faster than expected reduction in demand will eventually lead to a recession - a degrowth in corporate earnings along with income and spending levels of individuals.

As an investor, the correct question to ask ourselves today - isn’t whether there will be a recession or not - it is what will be the severity of such a recession and how long will it last?

While the consensus states that their will be a recession, the jury is still out on the severity and duration of such a recession.

Part Four: Impact on India

So there will be a recession in US, EU, UK and much of the western world, but what does that mean for India?

During the pandemic when majority of western world was busy distributing cash to its citizens, Indian Reserve Bank treaded lightly. The RBI was accommodative to the extent necessary and our Government made policies that were targeted at specific sections of the society rather than a blanket one size fits all approach.

That conservative approach of RBI is helping us tame inflation today. While the inflation in India is high as well, it is no where near the 4x of upward target of 6%.

To put this in context, current inflation rate in US is well above 8% (4x of Fed’s long term target of 2%). Had RBI been as aggressive as US Fed during the pandemic, inflation in India today might have been as high as 24%.

Add to this, our banking system along with the government are flushed with cash and possess strong financials.

So while there maybe a slowdown in overall economic growth rates of India due to a recession in western world, the extent of such a slowdown will be limited.

This trend also shows itself in the broader stock market indices. Over the last six months, Indian stock market have been more resilient compared to their peers in Europe and America.

This resilience comes against the backdrop of the highest FII outflows from India in more than a decade.

So why are FIIs selling if India is doing so great?

A simple logical explanation is because India has done so great. When you look across the emerging market options available to institutional investors globally, there are pretty much only four major markets to invest in - China, Taiwan, South Korea and India.

Traditionally China has taken the lions share of emerging market allocation, followed by South Korea, Taiwan and then India. No institutional investor allocating to emerging markets looks at India in isolation, its always a comparison vs other countries.

When money moves out of emerging markets its moves out across all countries as a risk off approach. Because India has relatively performed stronger than other markets, more money moves out of India as that’s where institutional investors have profits to take off the table from.

My Investment Strategy

So all of the above ultimately brings me to my investment strategy for next two years.

Here are some of the assumptions I am working with.

There will be a recession in EU, UK and US

Severity of the recession will be mild in US

Extent of such a recessions will last upto 18 months (start to mid 2024)

India’s economic growth will slow down but still remain above 6%

India will still remain the fastest growing economy in the world

Stock markets will gyrate between volatile to sideways until 2024

Intense bull market run will not start again until after the elections of 2024

Valuations will cool off to the lowest or mid quartile range from current highest quartile range

Recent speculative SPAC listing in US will continue to get butchered and may prove to be a good hunting ground for high risk high return investments

FIIs will return to India late 2023 with a higher allocation that they have made ever in the past

I will put a caveat here that these are just my assumptions and not necessarily what will happen. I have made the above assumptions based on the factors described throughout this article and in my view the above have a decent probability of playing out.

Based on the above assumptions, below is my simple investment plan.

Continue to be very stock specific and extend the timeline of building full position from weeks to quarters

Allocate to index where a large correction has already occurred and underlying fundamentals of index constituents remain robust - Nasdaq 100 and Bank Nifty for example

Build and continue to hold at least a 15 to 20% cash position until end of 2023

Sell positions where inflationary headwinds are eroding fundamentals and earnings

So as you can see, from supply chain issues, inflation, Russian War and Chinese lockdowns there are little fires everywhere across the world 🔥

Whether these little fires turn into a full fledge blaze is dependent on

How fast supply chains get fixed

How central banks and governments around the world act through the upcoming recession

Do you have an investment plan? What assumptions described above do you not agree with? Let me know in the comments 👇

Thank you for reading, see you in the next one.

Peace,

Tar

Hats off Tariq. Please write more or start Youtube channel like Ishmohit to explain topic like stock selection, selling method, allocation method and what not. Hope to hear more from you in future. Thank you. If possible please make your conversation with Ishmohit public regarding quarterly results and other. Thank you once again to clear all doubts.

Excellent write up! Sensible approach to "how to invest from now on"!