The Business of Hero Moto Corp

When Opportunity Hides in Plain Sight

The story of Hero is the story of persistence, collaboration and achieving goals that many would have regarded as impossible.

From its humble roots of selling bicycles in 1956 Ludhiana Punjab, to becoming the world’s largest two wheeler company is an extraordinary feat. Maintaining the momentum, protecting its market share and setting sights towards ‘Future of Mobility’ is something special.

Yet this giant, that sells its products in over 40 countries globally, has manufacturing capacity of over 9 million units annually and churns out a new two wheeler every few seconds from one of its eight production plants spread across India, Bangladesh and Colombia, is valued for about ~1x Sales.

This is my attempt to find out - Why?

Before we proceed, please consider sharing this write up with your friends or on your social media.

My aim, through these write ups, is to reach out to as many people as I can, so that they can make informed financial decisions.

I won’t bore you with the history of Hero, there is more than enough material to read on the internet and if you’re from India, chances are you probably already know about it, as Hero is a household name.

Instead, this write up is focused on the journey of Hero, since the dissolving of its joint venture with Honda, steps taken to rebuild the R&D foundation and what the next decade may look like for the company.

Part One: The Big Set Back

December 2010

Business news headlines around India are reporting Hero Honda’s 33% jump in sales for the month and Hero’s stock is on an upwards trajectory, rewarding its shareholders a ~40% increase in share price that year, out beating the market index by a wide margin.

Yet the atmosphere in the board room, at Hero Honda’s headquarters in New Delhi is not pleasant. What the world doesn’t know yet, is that in less than 15 days, the joint venture between Hero and Honda Motors will dissolve.

Hero’s partnership with Honda was a pivotal moment in its history. The two companies formed a joint venture in 1983 to produce motorcycles for the domestic market. Honda was to supply Hero with R&D while Hero would work on scaling up manufacturing. The arrangement worked well and their partnership, soon catapulted HeroHonda to become the largest two wheeler company in the world by early 1990s.

By 2010, the same partnership was hindering growth for Hero. Honda was never completely forthcoming with the R&D and used it as a leash to control the ambitions of Hero. The initial agreement with Honda, also meant that Hero wasn’t allowed to scale up its export business beyond the boundaries of India and had limited presence in Bangladesh, Nepal and Sri Lanka - tiny markets at the time.

Meanwhile at its home base, in India, competition was brewing from every nook and corner - Bajaj, TVS and Eicher Motors were foraying into premium models and wanted to gain market share from Hero. To add to this competition, user preferences were migrating from motorcycles to automatic scooters, an area dominated by Honda Motors with their Activa offering.

Breaking up with Honda was the logical choice - a tough one but the only way out if Hero wanted to become a global brand.

When two parties agreed to dissolve their partnership, an agreement was formed that Honda would continue to supply R&D and engine designs to Hero till 2014. Honda would later back out of this agreement as Hero forayed into scooters.

The culmination of these events led to the decline of Hero’s market share in the two wheeler space - particularly in the premium category. Hero Honda Karzima used to rule the premium segment of the market, but by mid 2015’s offerings from Bajaj (Pulsar), Eicher (Royal Enfield) and TVS (Apache) took the top spot. Hero instead chose to double down on its entry level offerings, an area its still the leader in today.

Part Two: Hunt for Growth Begins

2016 to 2021

2016 was the year when Hero started to lay the foundation for its future growth. It launched a new R&D center in Jaipur, India followed by another one in Germany.

The same year Hero would invest and become the largest investor in a little known electric vehicle upstart from Bengaluru called Ather Energy.

Over the last five years from 2016 to 2021, Hero has been busy breaking the shackles of its past.

It has forayed into international markets - now supplying its products in over 40 countries globally, eight of which are growing substantially. It has also reworked its mission statement, setting its sights on the ‘Future of Mobility’, not limiting itself to just two wheelers.

Hero’s goal is to produce and sell another 100 million vehicles in the coming decade (Hero has sold 100 million two wheelers since its inception).

Meanwhile back at home in India, headwinds would grow stronger for Hero.

The last five years haven’t been kind to the auto industry - first came demonetization in Nov of 2016, followed by NBFC crisis of 2018, followed by transition to BS-VI transmission norms in 2019 and then finally the pandemic of 2020.

Most of its peers were impacted, but Hero felt the burden more. A major chunk of Hero’s sales comes from entry level motorcycles targeted at the rural segment of India. Hero distributes these motorcycles via 6000 touchpoints spread across the nation. No other auto manufacturer in India has such a wide distribution network.

While most of its peers have reported sales CAGR of anywhere between 4 to 11% for the last 5 years, Hero’s sales have grown at mere 2%. The main reason behind this deviation is the presence of its competitors in the premium segment.

In auto industry, the only way to protect your margins is to have a balance of entry and premium products. Entry level products lets you build scale while premium products help you in pricing power and delivering better margins. Sway too much on either side and you either risk losing your margins or not have enough demand to implement economies of scale in your business. Since Hero product mix sways too much on entry level side, it has scale but not as much pricing power.

Hero is fixing this by offering more premium variations to its existing products.

Splendor Canvas is an example of such an offering. The investment in R&D has also started to yield results - helping Hero launch more premium products with its Xpulse and Xtreme range. Competition remains tough in this category with names like TVS and Bajaj dominating the market share.

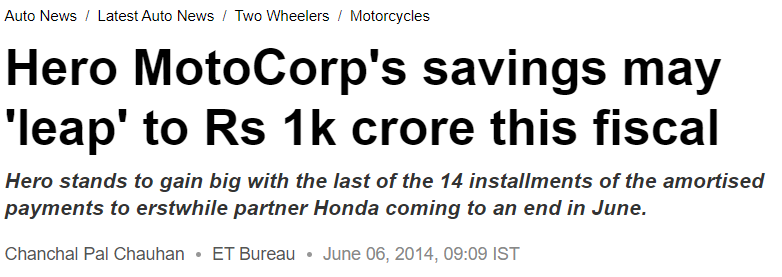

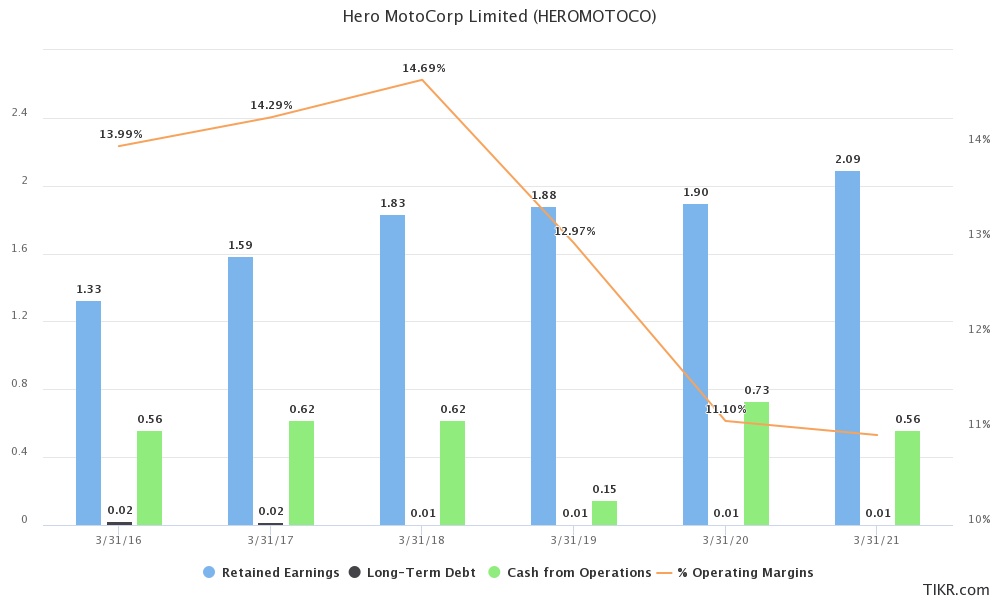

Another step taken by Hero to further alleviate the margin pressure is to implement a company wide cost savings program called - Leap. Leap was implemented in 2014 and has over the years helped Hero cut through the headwinds amid an inflation in commodity prices. Hero today saves enough money today, to delay the price hikes on its products and thus help protect its market share within the entry level segment.

The same Leap program has helped Hero maintain an operating profit margin of above 12%, even in the toughest of years.

You would imagine, five years of headwinds would have depleted the financials of an auto company - but not Hero. Hero Moto Corp financials today are envy of its peers. The balance sheet has negligible debt and cash reserves of over $2 Billion. The main business of Hero still throws up almost half a billion dollars worth of Free Cash Flow every single year, three times more money than Hero plans to spend annually.

The only piece missing in this puzzle is growth. Let’s explore where the growth for Hero will come from.

Part Three: Racing Ahead

Exports

Hero’s strategy with exports is two fold - first it helps the company produce and sell more of what its already good at - entry level motorcycles, and second it helps offset some of the sales erosion that may take place in India on account of transition to electric vehicles.

While a Hero motorcycle can be found in over 40 countries globally, only eight of them account for the lion’s share of the export business. Within these, Bangladesh, Mexico, Colombia and Nigeria are the fastest growing markets. The single thing common between these four - they are all immune to EV adoption, at least in the short term.

Take for example Nigeria, where Hero sells an entry level bike named Hunter. Electrification of a country like Nigeria is far away, motorbikes are still the primary form of transport in the country, referred to as ‘taxis’ by the locals. Hero developed Hunter from the ground up for the Nigerian market. Its designed to carry a heavy load, is durable and beats existing products on mileage - thereby allowing a Nigerian ‘taxi’ driver to earn more.

This is an example on how Hero is catering to a global market by designing and selling products suited for each individual geography.

To grow its exports fast, Hero has borrowed a page out of the playbook of its erstwhile partner - Honda. When Hero enters a new market, it does so in partnership with an established local distributor. This way, Hero doesn’t have to spend a lot of money on building a distribution network in each country and can focus on building products instead. Such a model has worked well for Hero in each of its fastest growing markets - Mexico, Nigeria, Bangladesh and Colombia.

Hero has a target of 15% sales volume from its export business by 2025.

Premiumization

When it comes to selling premium models, there is no brand more iconic than Harley Davidson. Hero has a partnership with Harley to manufacture, market and sell products under the Harley Davidson brand in India. These products will be targeted at the highest end of the market allowing Hero better margins and maybe some room to gain market share in this category.

Today’s Hero’s market share in premium category is at a mere 1.6%.

The company is further beefing up its product portfolio in the 160cc to 200cc category with its XPulse and Xtreme range. It plans to launch one new product in this segment, every year for the next four years.

Making progress is this category is important for Hero - this is the most EV immune part of the two wheeler market and allows Hero to improve its operating margins to above 20%.

Spare Parts

Hero started selling motorcycle components in 2013 under the brand ‘Hero Genuine Parts’. In 2014 this business was making 1800cr in revenue every year, today it makes over 3200cr ever year and is growing at double digits (even during the pandemic).

Hero plans to have 10% of annual revenue from this line of business by 2025.

Spare Parts are a lucrative and very high margin business for any OEM, Hero has further enhanced the margins in this area by backwards integrating into manufacturing these parts on its own. Today over 25% of spare parts are produced in house by Hero, rest outsourced to ancillary companies.

Making over half a billion dollars a year just doing spare parts sales is no easy feat.

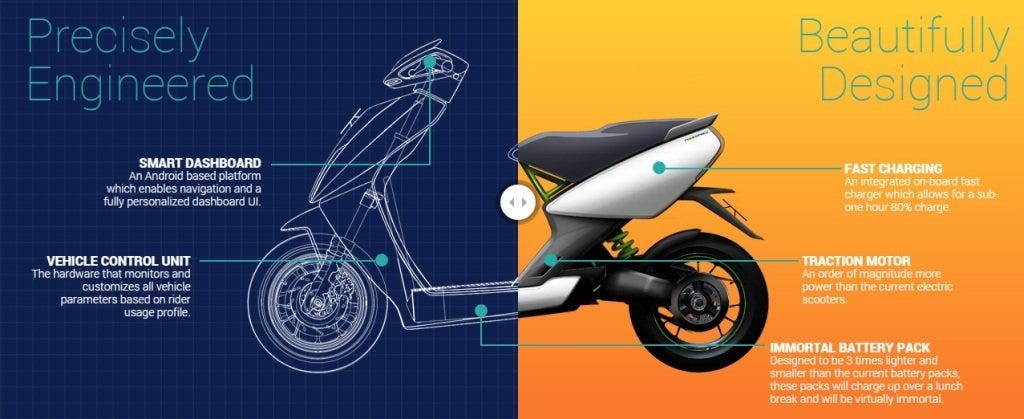

Electric Vehicles

Final part of this growth puzzle is Electric Vehicles. Hero has been ahead of its peers in embracing the transition to EVs. Its first investment in EV space was Ather Energy (~38% stake today). Another big leg up came with the partnership with Gogoro, a Taiwanese based company that has championed battery swap and go technology for two wheelers. Finally, Hero is also developing its own EVs two wheelers in house, with first one to launch in March of 2022.

To an outsider, this approach to electric vehicles may look messy - too many fingers in too many jars type approach, but there is a method to this madness.

Whenever a new technology enters the market, it is imperative to test out multiple approaches in order to assess which technology works for which segment of the population. Just like today, everyone doesn’t buy entry level motorcycles, tomorrow everyone may not choose to buy a standardized electric scooter that tops out at 65km/hr.

Hero’s approach to electric vehicles is to test out what works in the market by making product options available for every segment of the population.

Ather 450X for example is a premium electric vehicle, capable of fast charging and reaching speeds of upto 80km/hr. Gogoro’s SmartScooter can reach upwards of 100km/hr. and is center around battery swap and go technology that mimics the experience of refueling.

While very little is known about Hero’s own electric vehicle scooter, the glimpses provided by Dr. Munjal (CEO of HeroMotoCorp) shows that its capable of fast charging and is designed to keep affordability in mind.

Hero is taking the same approach to electric vehicles as the auto industry has taken to motorbikes in the past. Motorcycles come in three categories - Entry (100-125cc), Deluxe (125-150cc) and finally Premium Segment (150cc and above). Electric Scooters too seem to be transitioning to that segmentation - affordable (Hero’s own EV) , premium (Ather) and swap & go (Gogoro).

Hero plans to launch two electric vehicles in 2022 and thereafter one new electric vehicle every single year till 2030. Out of the total capex of 10,000cr, Hero plans to spend in the coming decade, 50% is reserved for development of EV products.

If you want me to do a deep dive into Gogoro and Electric Scooter space in India, please leave a comment.

Part Four: Feet on Ground, Eyes at Sky

Investment Thesis

In my view, the worst is already baked in to the valuations of Hero today. The headwinds of last five years couple with slow growth has led market to discount what the future and near term holds for Hero Moto Corp.

I foresee a strong case of rerating for Hero in 2022 as the company transitions to launch more electric scooters and build its product catalogue for EVs. Couple that with strong double digit earnings growth driven by exports, rebound in domestic sales and a growing ancillary business - and you have a good investment thesis.

Everything that could go wrong, seems to be already baked into the price, implying a high margin of safety for future revaluation.

Risks

This isn’t to say that there are no risks to the company. There are a growing breed of upstarts in India that are scaling up and launching new electric scooters. Backed by Private Equity giants they have a single mission - to electrify India by 2025. The two major ones to watch out for are Ola Electric and Simple Energy.

There are other ones too but they all lack scale. To succeed in any kind of hardware business, especially in the business of making two wheelers you need scale.

The only two upstarts focusing on implementing scale today are Ola (10 Million annual capacity) and Simple Energy (12.5 Million annual capacity).

The good news is, reaching scale needs time and Hero doesn’t have any shortage of its own funds to deploy in this war for EV market share.

Another major risk, I see in Hero today is cannibalizing its own sales. A EV scooter sold by Hero will be counted as a substitute purchase - an existing customer of Hero who was supposed to buy a bike may now buy a electric scooter from them. So increase in sales of electric vehicles may mean an equivalent decrease in sales of motorcycles for Hero. While for the likes of Ola, a sale is a sale, it is not competing against its own existing products.

A higher than expected slowdown in entry level segment due to this transition to EVs is another major risk for the company as entry level bikes are its bread and butter.

There are a bunch more smaller risks and anti-thesis in the company - I sourced a couple from the community at Twitter - leaving a few of them for you in the segment below.

Risks and Anti Thesis Pointers sourced from Twitter

Thank you to everyone who contributed, sorry I wasn’t able to include them all. If you want to read the entire thread all possible risks within Hero, you may access via below link.

Few good ones, are highlighted below.

Conclusion

The entire investing case in Hero today can be summed up in a single line - can a value bet of today become a growth bet of tomorrow?

Going by their history, the events that led up to valuations of today and incremental earnings triggers of next 5 years - I certainly think so.

Thank you for reading, see you in the next one.

Peace,

Tar

Excellent article .

Intresting read .