The one sector on the cusp of regulatory transformation

Exploring opportunities arising out of the Electricity Amendment Bill of 2021

Power Industry in India is no stranger to regulations - the industry has battled with regulatory changes since India’s independence in 1947. Most of these changes in recent years, have focused on strengthening the sector and making it more efficient.

Some of these regulations have worked, while others have failed miserably.

The Electricity Amendment Bill of 2021, is different. It focuses on the root causes of the problem and devises solutions accordingly, rather than try fixing them with a Band-Aid (as previous regulations did).

The method opted by the Bill to fix these ailments, is to bring about large changes in the Industry - ranging from privatization of distribution companies to mandatory sourcing of renewable energy.

Whenever there is a regulatory disruption in an establish Industry - the ground is fertile for opportunity. This article is an attempt to identify such emerging opportunities.

Before we proceed, please consider sharing this write up with your friends or on your social media.

My aim, through these write ups, is to reach out to as many people as I can, so that they can make informed financial decisions.

This article is divided into the following parts:

Current Problems with the Energy Sector in India

What does Electricity Amendment Bill 2021 proposes?

Opportunities arising out of Electricity Amendment Bill 2021

Conclusion

1. Current Problems with Energy Sector in India

Within the Indian Energy Sector, the current public electricity distribution companies are a ticking time bomb waiting to explode and impact the financial stability of the entire industry.

Together, all state owned electricity distribution companies (or DISCOMs), owe upwards of INR 75,000cr (~$ 10 Billion) to power generation companies. To complicate matters further, most of these DISCOMs have large debts to various state and national banks.

Financial conditions of these DISCOMs today is so bad that even after subsidies and various monetary schemes by central government (UDAY etc.), they are unable to turn a profit or breakeven.

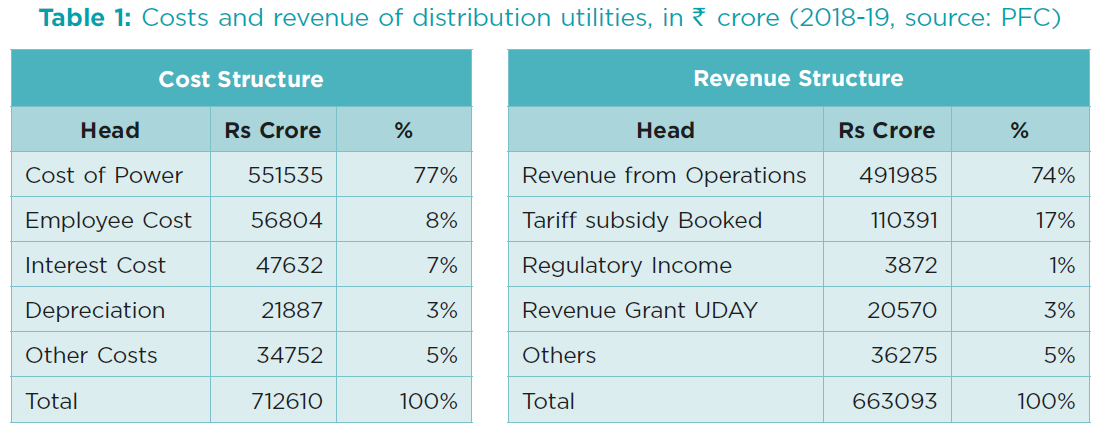

Below table is taken from a report by Power Finance Corporation of India. It shows the difference between cost and revenue structures of distribution utilities. Notice, how in the revenue structure, the total is still ~50,000 cr. short to breakeven. Take away the regulatory grants and subsidies and it gets worse.

These state owned DISCOMs haven’t made enough significant investments in upgrading the transmission and distribution infrastructure. The old infrastructure along with inefficiencies of a government owned utility company and political use of cheap electricity to win votes - has over the years translated towards India becoming the only large economy in the world where AT&C losses are upwards of 22%.

AT&C stands for Aggregate Technical & Commercial Loss, it is the difference in total energy generated by the grid vs total energy commercialized.

AT&C is a measure used to understand how much electricity produced by a country is wasted or lost (via transmission or theft or other inefficiencies)

As you can see from the above Figure, states who have privatized distribution of electricity (eg. Delhi and Maharashtra) report much lower AT&C losses compare to states where distribution of electricity is still under the control of state government (eg. Arunachal Pradesh).

Among the myriad of challenges, include GST and taxation. As electricity comes under State Government, there isn’t a standard nation wide taxation policy. It is left upto State Governments to decide how they want to tax electricity consumption - which in some states is taxed as high as 20%.

To complicate matters further - lots of taxes and duties are levied on coal (responsible for over 50% of electricity generation in the country). Even though coal is under GST regime, electricity consumption is not - which prevents utilities from accessing the input tax credits as per GST policies. It is estimated that just inclusion of electricity under GST will reduce cost of electricity consumption by 17paise per unit across the nation.

Today, the central government has to infuse funds to this sector every year (~90,000cr in 2020 alone) while the collective debt of state owned discoms stand to touch ~6 Lakh cr. This trend is obviously not sustainable and if something isn’t done anytime soon - the entire sector maybe on the verge of collapse.

To prevent this from happening - the parliament is about to pass the Electricity Amendment Bill of 2021 in the upcoming winter session.

Let’s now look at the major parts of this Bill.

2. What does Electricity Amendment Bill 2021 proposes?

Regulatory changes are not new to the power sector in India. Over the previous two decades, multiple regulations have been introduced with the objective to fix specific ailments within the sector.

The last major change was the Electricity Act of 2003, which introduced multi year tariffs and 25 year Power Purchase Agreements along with power trading and open access.

Open Access allows consumers with requirements of more than 1MW to source electricity directly from generators instead of distribution companies

Since 2003, specific regulations have been introduced to either stabilize the financial stress within the sector or to reduce the AT&C losses we discussed earlier.

The Electricity Amendment Bill of 2021 is primarily targeted at

Introducing private distribution companies and allowing end consumers to choose a distribution provider - a private company or a state owned player

Reducing AT&C losses within the system by making it mandatory to install smart meters

Enabling larger consumption of renewable energy by allowing for fixed renewable power purchase obligations

Giving more powers to the regulator to settle disputes and regulate the system by bringing more efficiency and transparency (like RERA did for real estate industry)

Let’s take a closer look at the first three.

Multiple Distribution Companies and Consumer Choice

The Bill recognizes that today distribution companies across the country are monopolies, either government or private. This reduces competition, disincentivizes the distribution company to invest in efficiencies and improving service, and leaves the customers with subpar experience and high electricity rates.

The Government now wants to delicense this entire sector. No longer a distribution company will require a license (which are limited and controlled by the state) to operate. Instead anyone in the country can apply to become a distribution utility.

To operate legally as an electricity distribution company, they have to register themselves with the appropriate commission in the State. As long as these companies meet the eligibility criteria, their applications will be approved within 60 days. Upon approval, a distribution company will remain bound by rules, regulations and oversight of the State Electricity Regulatory Commission (SERC).

What this essentially means is you as a consumer will have choice to either have a Torrent Electricity Meter, Adani Electricity Meter, Tata Electricity Meter or a meter from your local State Government owned distribution company.

The whole process and experience for the consumer will be very similar to how you have a choice today of telecom provider - you can choose between a Jio, Airtel, Vodafone or BSNL.

Just like today a Jio or an Airtel doesn’t have to stand in line and ask for operating license from every State government, similarly tomorrow, a power distribution company will not have to apply for a license in every state.

This operating model is nothing new - its already implemented across most of the developed world. In UK for example, consumers have an option to choose which utility provider they want - this is referred to as retail choice.

To enable this retail choice in India - government will separate the function of content (retail electricity) and carriage (wires). No longer a utility company will be responsible of building and maintaining the transmission infrastructure. This enables specialization and allows a DISCOM to focus on its core objectives - set up connections, provide quality service and collect revenue.

Reducing AT&C losses by making it mandatory to use Smart Meters

As we discussed, earlier in this article, India has one of the highest AT&C losses of any large economy in the world. Billing efficiency in India at a national level stands around ~83%. To counteract the issue of electricity theft and reduce AT&C losses, Govt of India, launched a National Smart Grid Mission, which has met with a lot of success in pilot states of UP, Madhya Pradesh and Manipur.

In Manipur, AT&C losses reduced by ~50% since the government started using prepaid and smart meters.

Smart Meters further help in load management, forecasting and overall more efficient management of the grid. Its no surprise then that Govt of India wants to implement them at a nation wide level now.

Along with smart meters, GOI is also inclined to allow DISCOMs to source power directly from exchanges under a policy called - Market Based Economic Dispatch or MBED.

This combination of cheaper sourcing of power and higher billing efficiency, should help the ailing DISCOMs achieve financial stability.

Larger share and mandatory purchase of renewable power

Renewables already make up of 25% of the national grid capacity. Every State has an obligation to purchase a certain percentage of their electricity requirement from renewable energy producers. However, these renewable purchase obligations are not always enforced. A state discom today chooses to purchase electricity from a state generator even though there maybe cheaper alternatives available in the market.

Further, only top six States in India account for 78% of all the renewable energy (RE) generation. RE rich states like Karnataka, Andhra Pradesh, Rajasthan and Tamil Nadu continue to meet their RPO while other do not.

To plug this gap, the Bill will introduce new provisions related to Renewable Purchase Obligations (RPO) and those who do not meet these new provisions will be subject to harsh penalties.

If you want to learn more about Renewables and New Energy Sector within India, you may opt to watch my in depth five hour long webinar.

Watch the webinar by clicking on the below link ⤵️

3. Opportunities arising out of Electricity Amendment Bill 2021

Whenever there are dramatic changes in an industry structure - either because of regulations or technology - there will always be a set of winners and losers.

Before, I focus on the winners, lets take a look at the characteristics of losers.

A typical loser in this space will be someone who has

High Debt

Current Monopoly Status

Lack of efficient infrastructure or capability to maintain it

Is not investing into customer service and experience

Those listed monopoly distribution utilities are an example of losers esp. if they haven’t kept up with technology, managed the leverage (debt) on their balance sheet and have high inefficiencies when it comes to collections.

The license these companies hold, which continues to prevent their monopoly status, will soon vanish much similar to how a New York Taxi License today is nearly not worth as much as it was before the launch of Uber.

Comment below on who you think meets the above criteria of losers and may get disrupted in coming year.

Let’s now focus on the winners.

Based on the motives of the bill, there are four type of companies that stand to benefit from the upcoming regulatory tailwinds.

Renewable Energy Producers

Power Exchanges

Transmission Infra (Smart Meters, Transmission Companies)

Private Distribution Companies with Strong Balance Sheet

Let’s explore a few available investment opportunities within each of the above category.

Renewable Energy Producers

The obvious beneficiaries are renewable energy producers. The Bill mandates a higher obligation, on all States, to source renewable energy. This will directly benefit the likes of Adani Green and ReNew Power.

Power Exchanges

Second obvious beneficiaries are power exchanges like IEX and PTC. Regulations like MBED, larger advocacy for open access and cross border trading and supply of electricity will function as tailwinds for these companies.

Transmission Infra

The other beneficiaries are companies that are providing the infrastructure required for this transition. Manufacturers of smart meters like Genus Power and those who lay down the transmission lines like Adani Transmission are direct beneficiaries of the new regulation.

Private Distribution Companies

Finally we have private distribution utility companies like Tata Power who are positioned to reap the maximum benefit from the new legislation. Be careful when picking companies within this space - most of them have heavy debt on their balance sheets and as such cannot afford to reap the maximum benefits of forthcoming opportunities.

Length limits of this article prevents me from doing a deep dive into each of the companies mentioned above, but I will leave you with snippets of how some of them are perceiving and preparing for the upcoming opportunity.

Genus Power on Smart Meter Demand

Tata Power on Applying for DISCOM opportunity in multiple cities

Other Private Discoms Ready to Take Over Ailing DISCOMs even before the Bill is Passed

Conclusion

As evidence shows, the Electricity Amendment Bill 2021 represents a historic change in the current structure of the power distribution industry. If implemented correctly, privatization of DISCOMs will have a massive impact on the fortunes of existing private DISCOMs and other incumbents present across the value chain.

As an investor, it is our duty to look at evidence, assign probabilities to outcomes and make decisions based on facts.

My earlier picks in this space have been Tata Power and IEX, and I am currently looking closely at ReNew Power and Genus Power.

I hope this article was helpful in decoding the Electricity Bill and the upcoming opportunities within it. My aim through this write up was to explain the various moving parts of the bill, present an investment thesis via data and then point you towards a direction to research further.

If you would like me to write a deep dive into some of the companies mentioned above, leave a comment.

Thank you for reading, see you in the next one.

Peace,

Tar

Enjoyed reading it. Super informative. Genus looks interesting. Thanks

In depth & also horizontally diverse. What do you think about proxies lime RMC Switchgear? Also how long do you think is the trend? There seems to be some froth here. Stocks like Genus are trading at >150 times.