Corporate India's Q3FY23 can be summed up in a single phrase - "Mixed Results, Slowing Growth." The latest quarterly earnings report suggests that inflationary pressures, rising interest rates, and global recession concerns are beginning to take effect.

India's consumption-driven growth, which helped it buck the global trend in 2022 following the post-pandemic reopening, appears to have stalled. Out of the approximately 4,253 listed companies, only about 42% reported growth in both topline (sales) and bottom line (operating profit) compared to the previous quarter in Q3FY22.

To gain a better understanding of Corporate India's Q3FY23, we will be analyzing four key metrics across industries - trailing twelve months (TTM) vs. previous year (PY) sales growth, TTM vs. PY operating profit growth, current quarter (CQ) vs. previous quarter (PQ) operating profit growth, and CQ vs. PQ sales growth.

In an effort to provide a more accurate picture of results, companies with a market capitalization below 100 crore have been excluded from the analysis. This is because such firms tend to have an outsized impact on overall results of an industry and can distort the true state of affairs.

Before we proceed, please consider sharing this write up with your friends or on your social media.

My aim, through these write ups, is to reach out to as many people as I can, so that they can make informed financial decisions.

The Backdrop

To provide you with an accurate understanding of the results, it is important to first contextualize the current global economic environment. Here's a brief summary.

Interest rates around the world are on an upward trajectory, driven by central banks mission to control inflation. High interest rates tend to have a cooling effect on an economy in two ways - first, it incentivizes people to save rather than spend and secondly, it sucks the excess ‘liquidity’ out of the system as it becomes expensive to borrow.

A combination of the above two is supposed to reduce demand and there by help tackle the inflation problem. Reducing demand (i.e. consumption) has a direct impact on earnings growth of companies.

Furthermore, rising interest rates can also impact companies that rely heavily on borrowing to finance their operations. As borrowing becomes more expensive, these companies may face higher interest costs, which could further eat into their profits.

The US Federal Reserve, which is widely considered the most important central bank in the world, has raised interest rates from their historic low of 0.05% in March 2020 to 4.57%, representing the fastest increase on record. It is expected that the Fed will continue to raise rates throughout this year, potentially reaching a range of 5.5% to 6%.

But what does this mean for you, and particularly for corporate earnings?

In the short term, consumers are being encouraged to save rather than spend, as they are offered higher returns on bank deposits. At the same time, borrowing money has become more expensive, as higher interest rates translate to higher EMI payments.

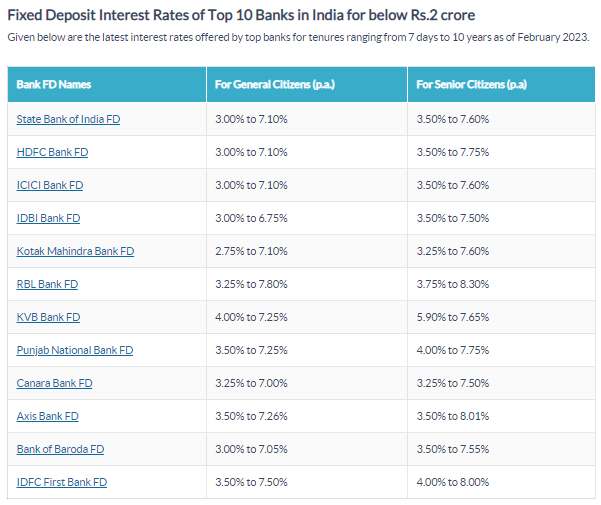

Below are the interest rates for traditional fixed deposits at some of the major Indian banks. Banks are willing to provide as high as 8.3% today for you to deposit your money with them. So if you were, for example, thinking of buying a second car for Rs 10 Lakh, you are being disincentivized to the tune of Rs 83,000 as the opportunity cost.

Similarly, yield on risk free assets like 6 month US Treasury Bill is now higher than the earnings yield of S&P500. So for a low risk dividend seeking investor, it now makes more sense to buy a 6 month US Treasury Bill than invest their money in S&P500 index.

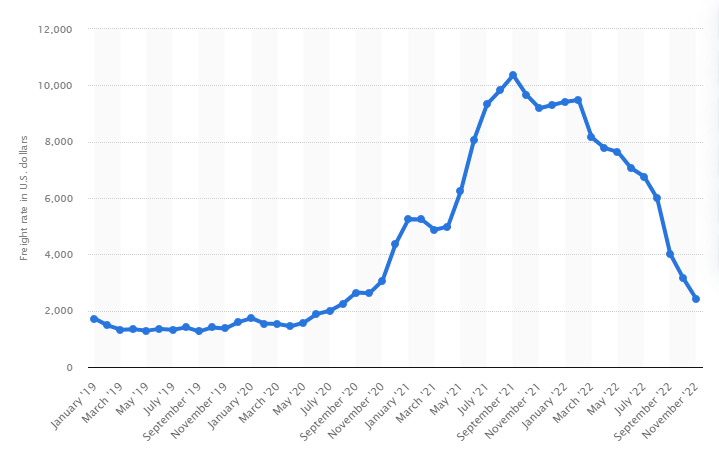

However, it's not all doom and gloom. There is some positive news for the global economy, as two of the most significant costs - oil (energy) and shipping (transport) - have decreased significantly in the past 12 months. This should help corporates offset some of the pressure from higher interest costs.

Now that we have established the global economic backdrop, let's shift our focus to analyzing the earnings of each industry within India's corporate sector.

Across Sectors Sales and Earnings Growth

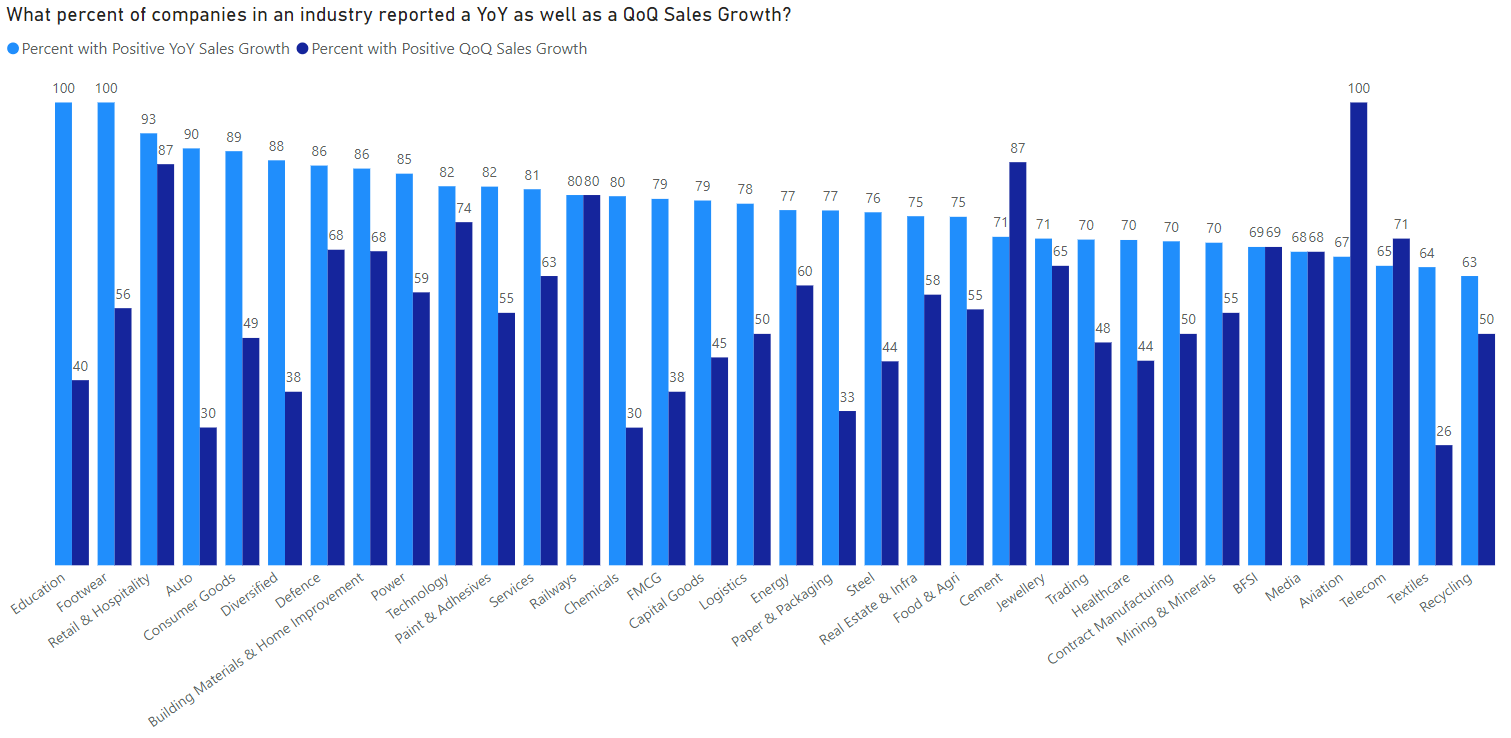

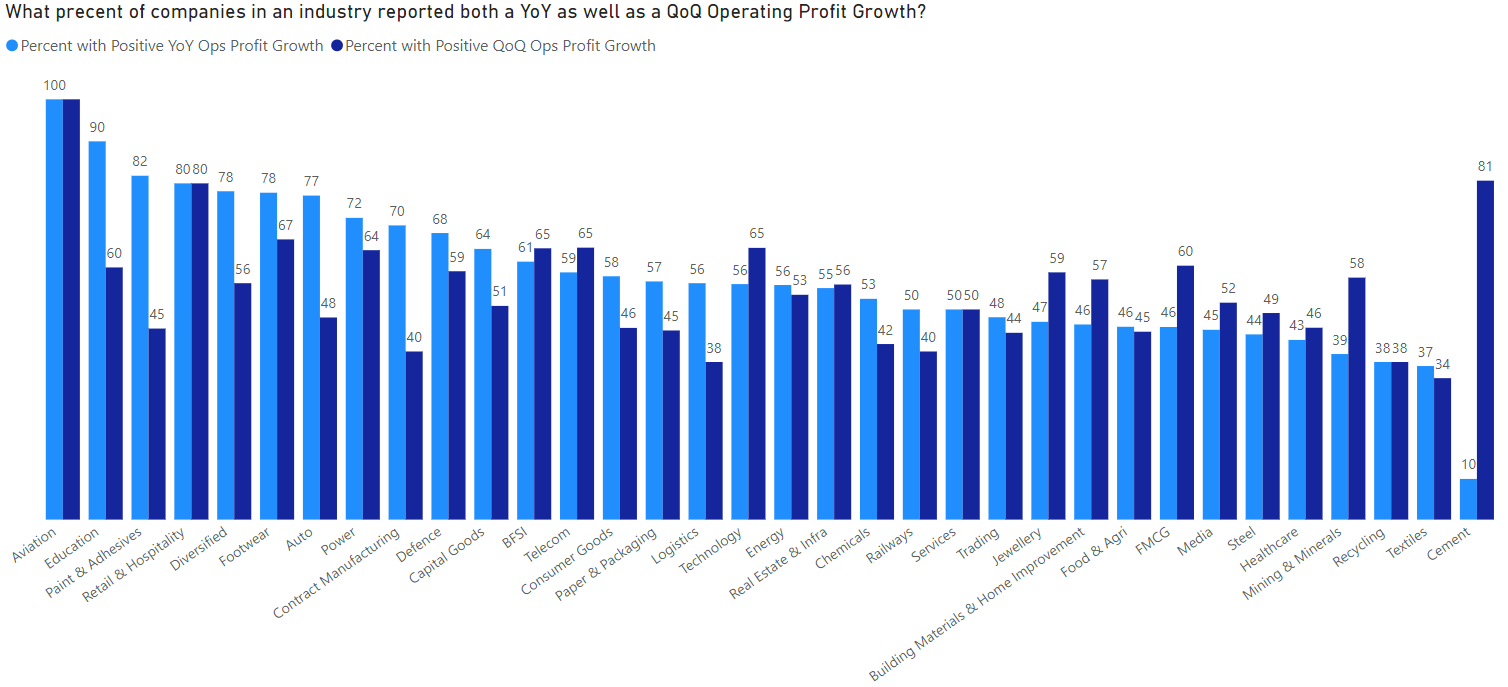

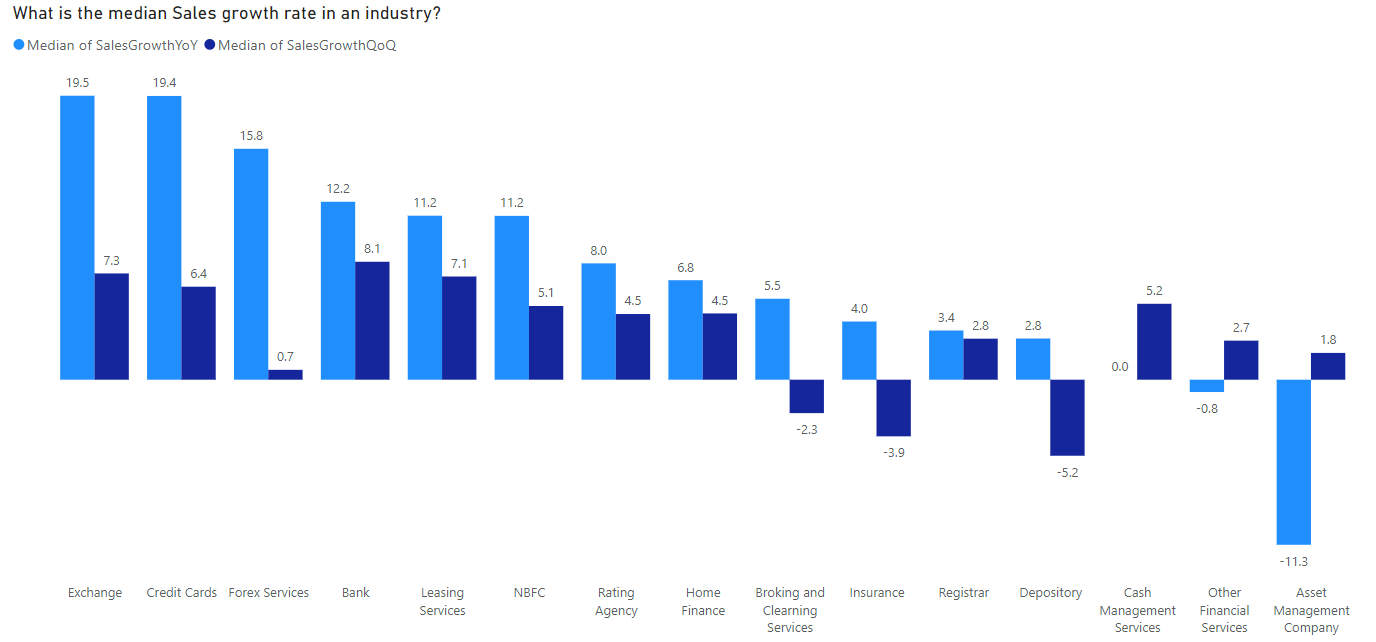

After excluding companies with a market capitalization below 100 crore, the remaining data indicates that around 77% of companies reported sales growth compared to the previous year. However, only around 51% of companies reported sales growth compared to the previous quarter.

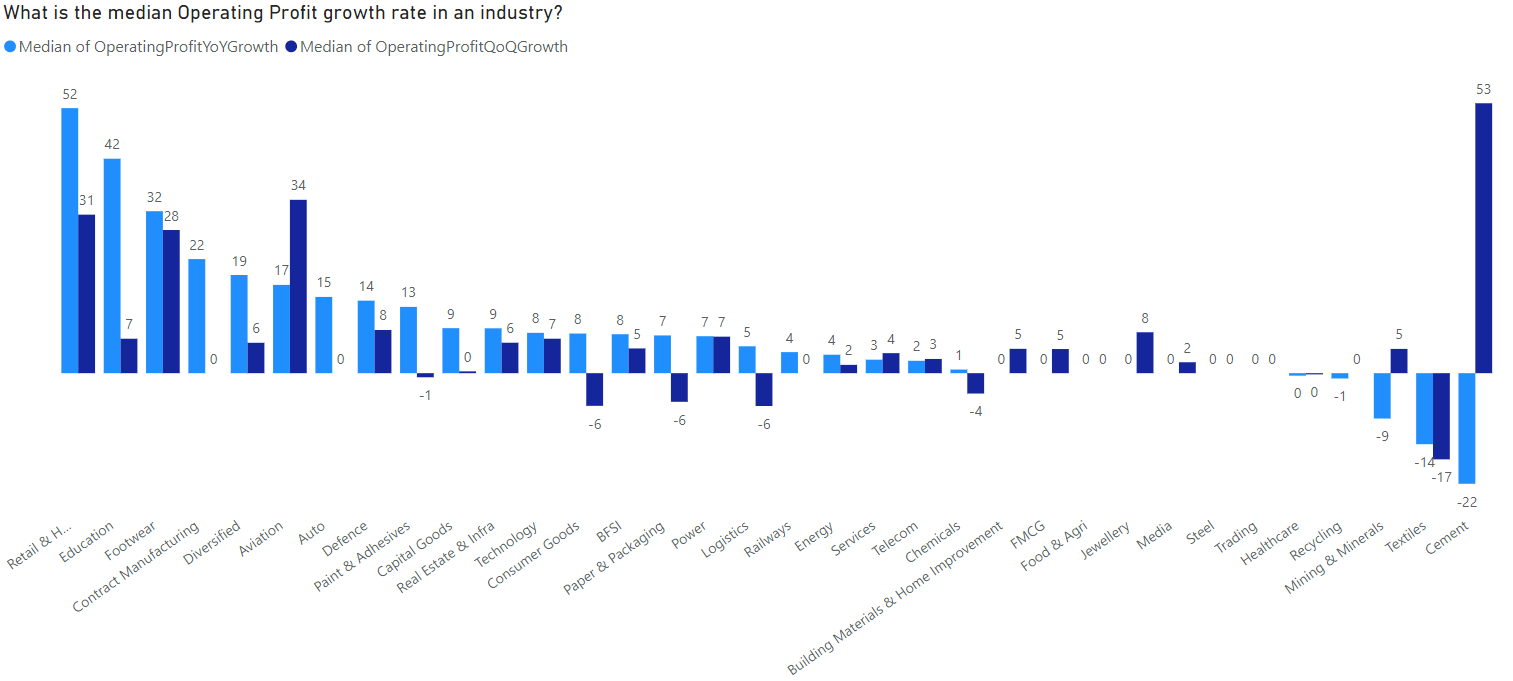

In terms of earnings, approximately 56% of companies reported earnings growth compared to the previous year, while around 53% reported earnings growth compared to the previous quarter.

The data clearly indicates a slowdown in topline, though corporate India is able to withstand margin pressure to some extent.

Upon examining individual industries, it is clear that the slowdown is most pronounced in sectors that deal directly with consumers. Industries such as footwear, consumer goods, automobiles, and FMCG have all reported a slower pace of topline growth.

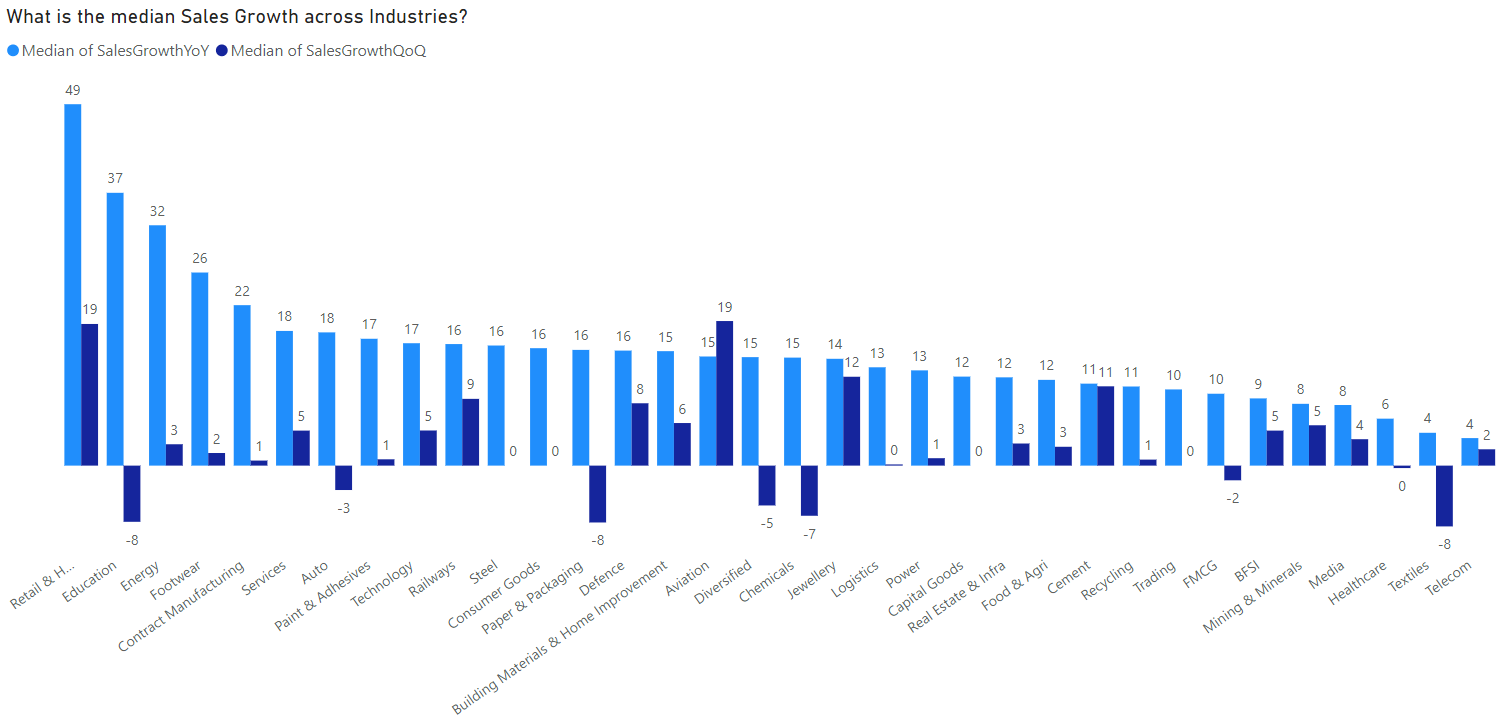

For example, only 56% of listed companies in Footwear industry reported a quarterly sales growth. Similarly in FMCG, only 38% companies reported a quarterly sales growth. Further, on a consolidated basis, median quarterly sales growth across FMCG companies stands at a negative two (-2%) percent.

The only sectors that reported both, a strong quarterly as well as yearly sales growth are - Aviation, Jewellery and Cement.

The worst impacted sectors are chemicals, textiles, paper & packaging and education - all of them reporting a negative median quarterly sales growth.

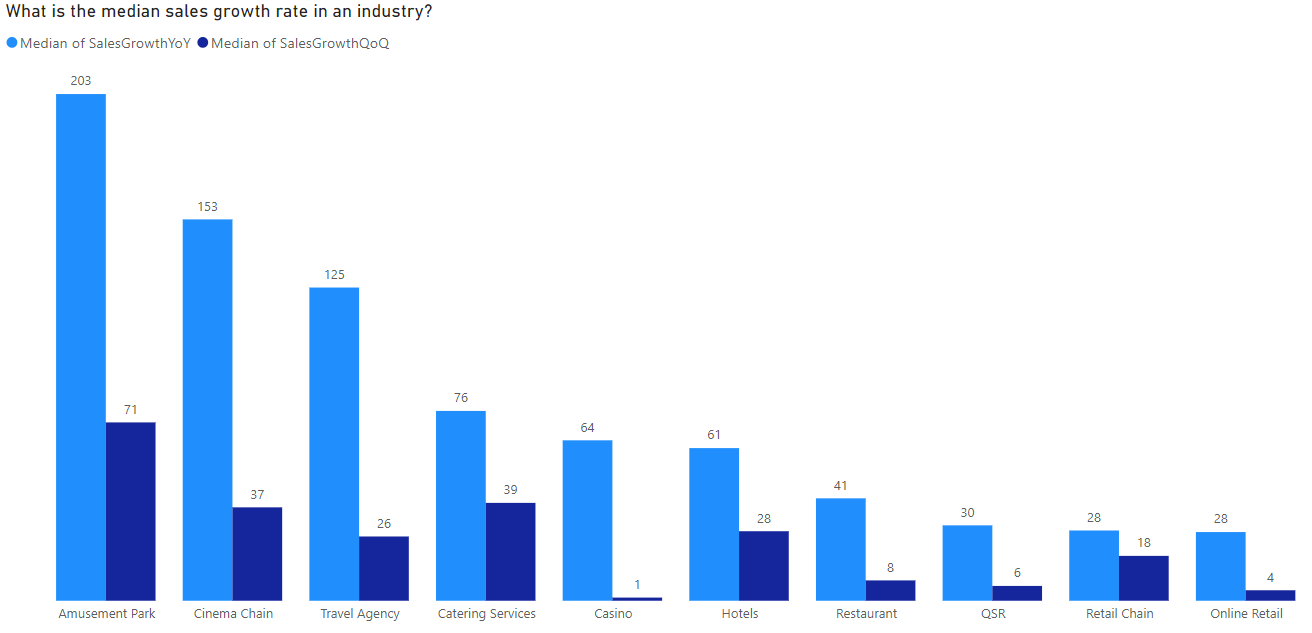

Retail and Hospitality which includes sub sectors like Hotels, Retail Stores, Cinema Chains, Restaurants and QSR, were the biggest beneficiaries of re-opening reporting almost a ~50% median sales growth, but even there topline growth has slowed down sharply this quarter to just about ~19%.

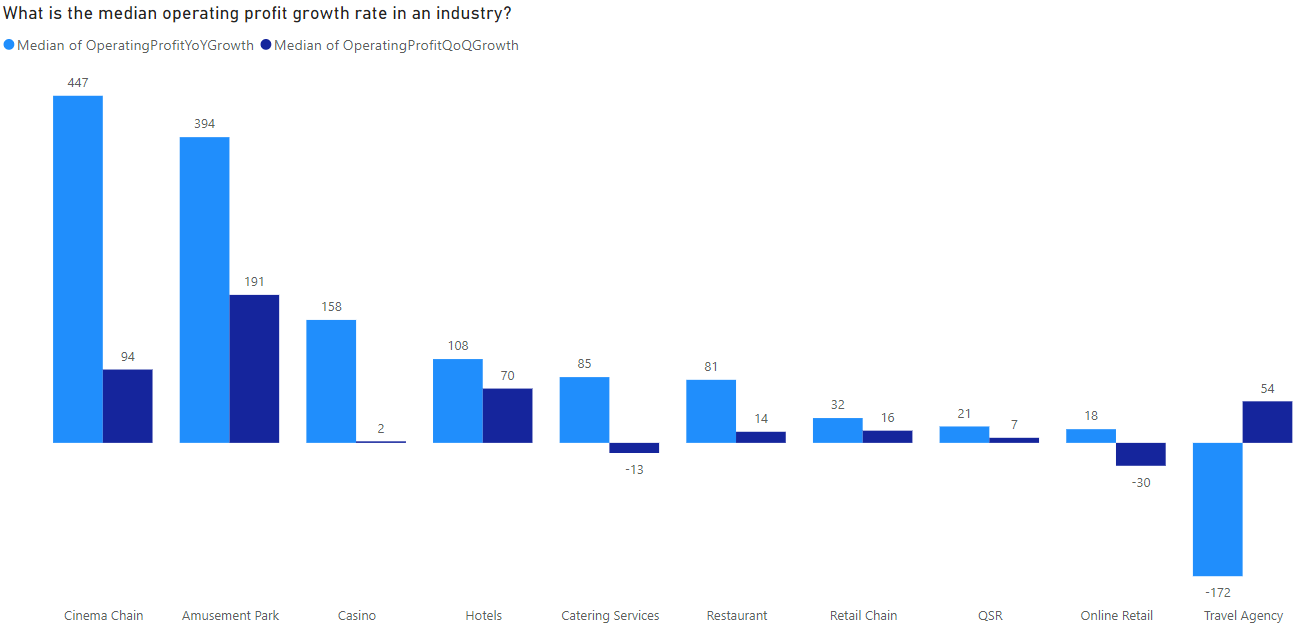

When it comes to earnings growth, the overall picture is much healthier. Corporate India has, in most cases, managed to protect its operating margins to a significant extent, as input costs such as energy and freight cool off in conjunction with recent price hikes.

Industries like cement which took several price hikes in second half of 2022, have clearly benefitted with about 81% of listed companies reporting an increase in operating profit vs pervious quarter.

Here too consuming facing sectors like FMCG continue to suffer with almost zero median growth. It remains to be seen if the consumption economy revives or declines further in the next quarter.

Sector Wise Analysis

BFSI

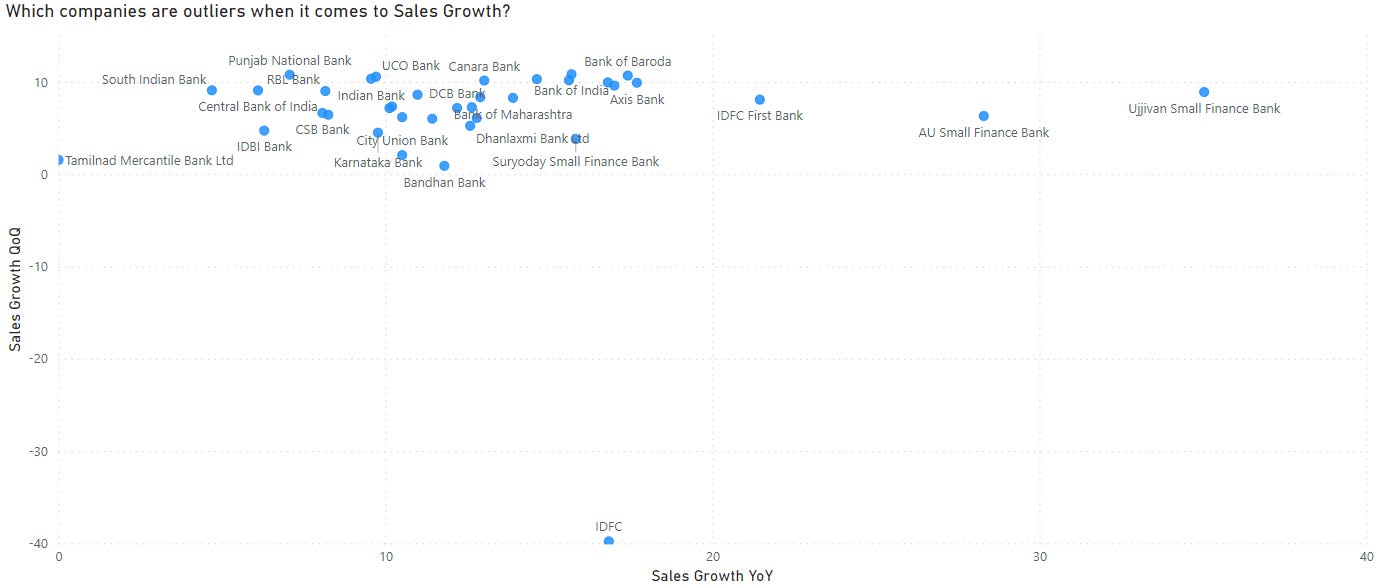

In the BFSI segment, the best performance for this quarter belongs to banks (both private and public combined). The median quarterly sales growth for banks, came in at 8.1%. Apart from banks, in the listed exchanges, MCX did very well with an actual quarterly sales growth of ~13%.

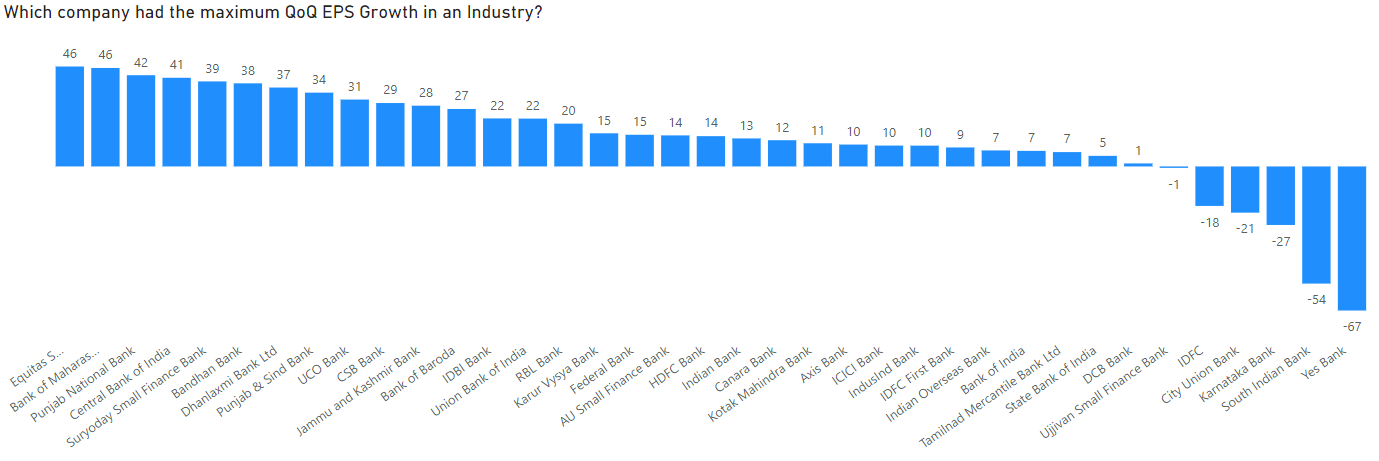

Among banks, Ujjivan Small Finance Bank is the clear winner when it comes to both YoY and QoQ Sales growth, followed by AU Small Finance Bank and IDFC First Bank.

In terms of pure EPS growth, however, Equitas Small Finance Bank takes the lead, followed by Bank of Maharashtra and Punjab National Bank.

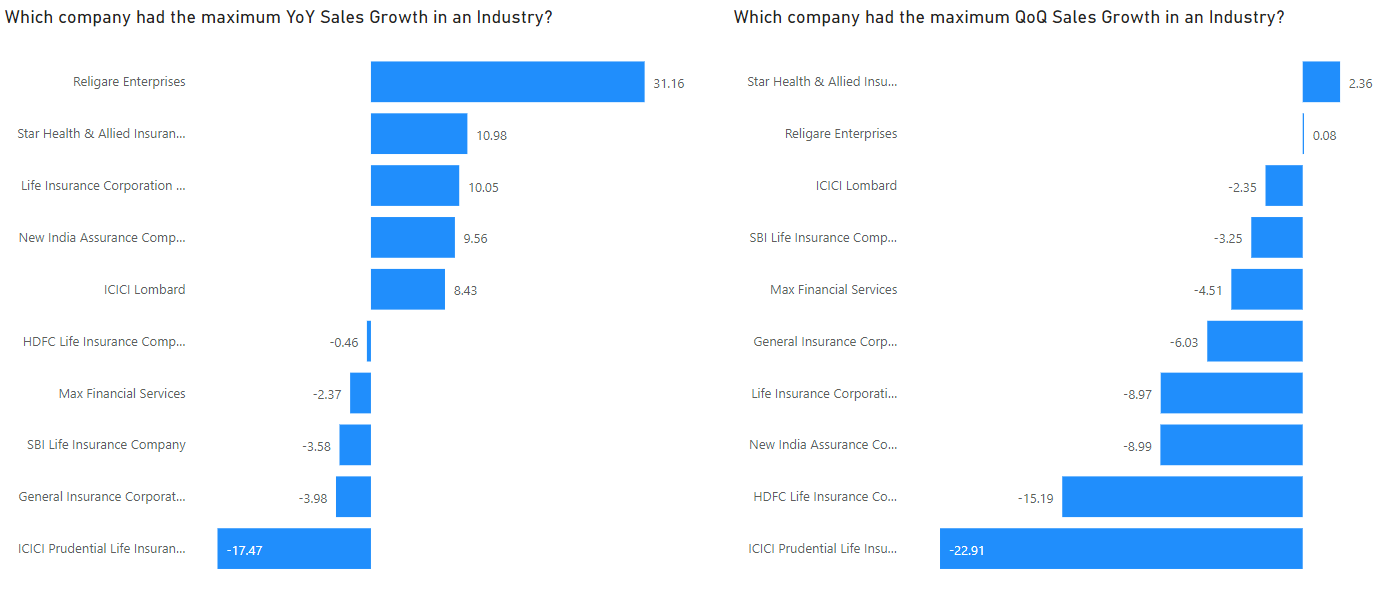

Turning our attention towards another big sector within BFSI - Insurance. Here too, most companies continue to struggle with the only two exceptions being - Star Health and Religare Enterprises.

There are multiple other sectors within BFSI, but its impossible for me to analyze all at a company level. Please also note that we are analyzing companies purely based on sales and operating growth metrics - other important factors like governance, valuations etc. are ignored here.

Railways

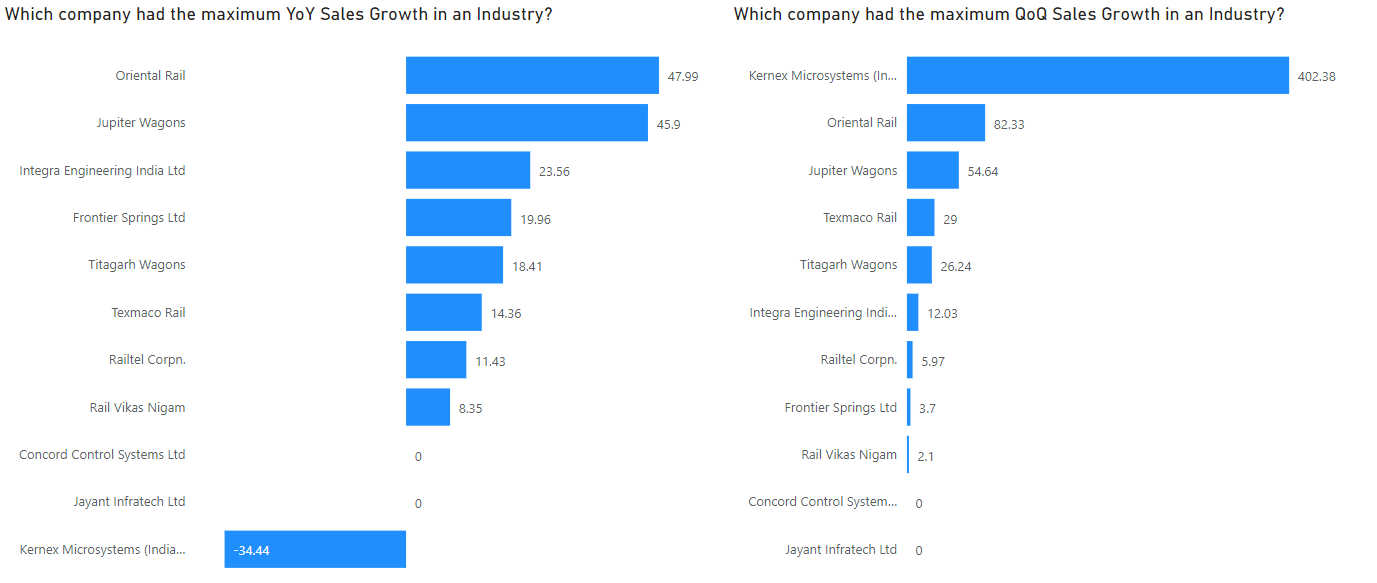

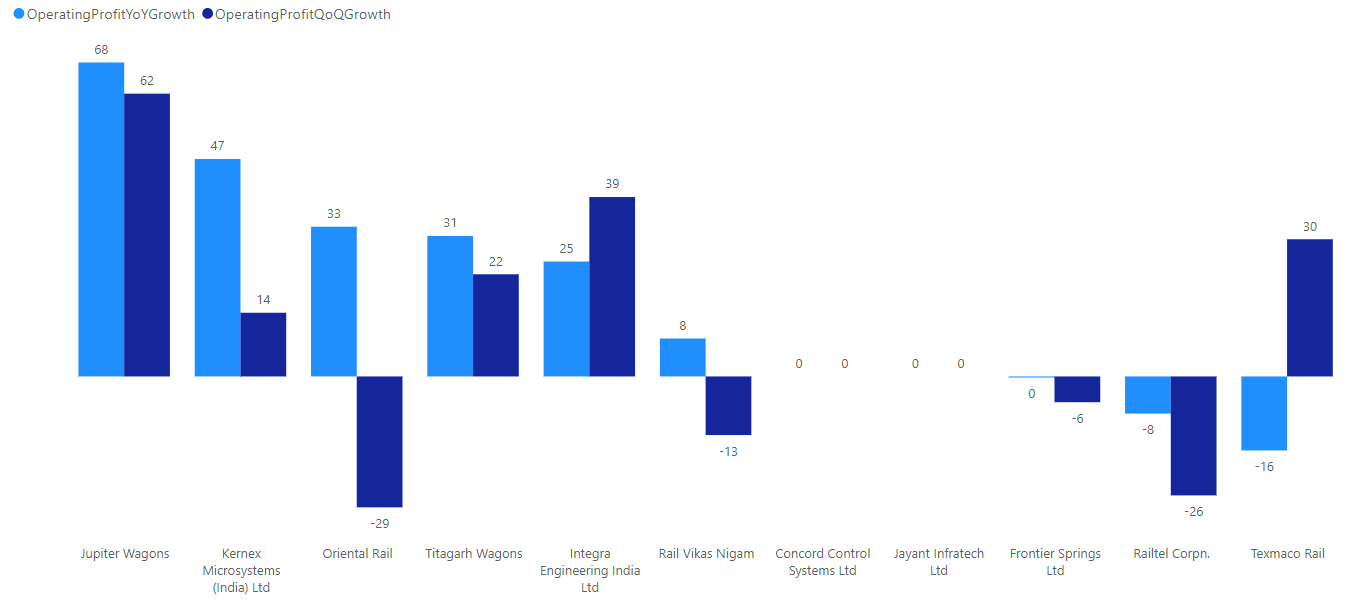

Most companies within Railways sector are doing well, driven by the big government capex push. Among, all the companies Jupiter Wagons stands out.

Although most railway companies are experiencing significant growth in their topline, Jupiter Wagons, Titagarh Wagons, Integra Engineering and Kernex Microsystems are the only ones achieving notable growth in bottom-line, i.e., operating profit.

Retail & Hospitality

The last 12 months for retail and hospitality sector were the gift of God. Almost all of hospitality sector has been growing on steroids driven by ‘revenge spending’ and post pandemic reopening.

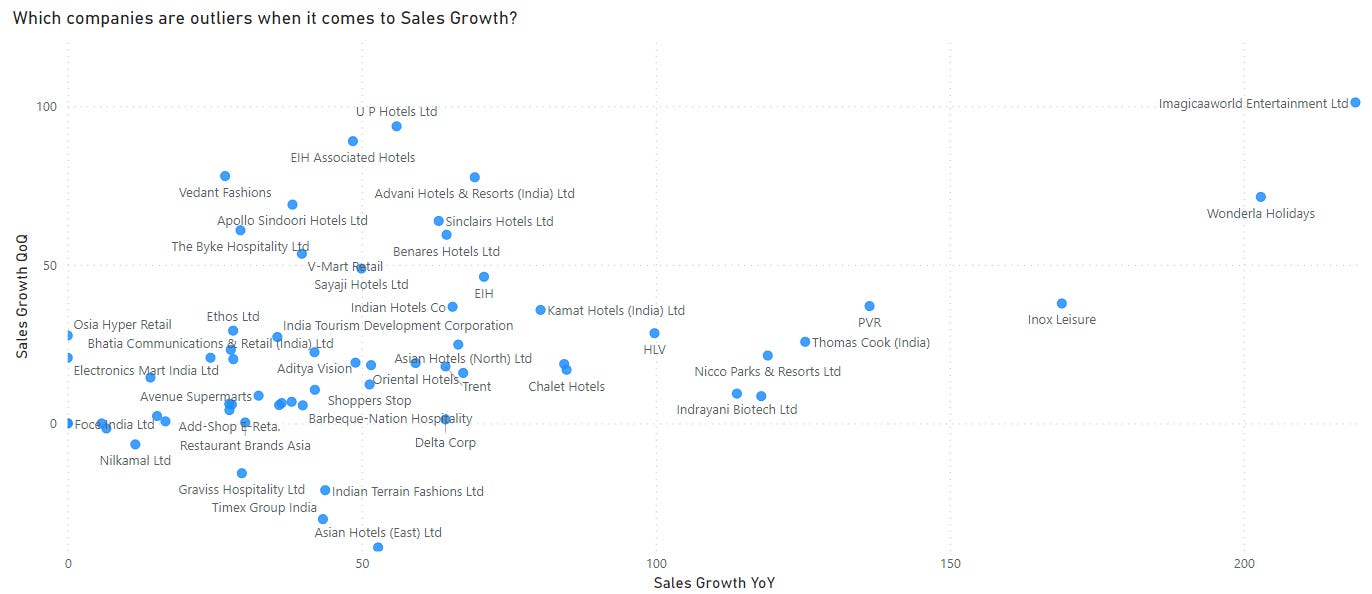

The best performing sub sector within the entire retail and hospitality sector - Amusement Parks!

Imagicaaworld Entertainment and Wonderla Holidays, two listed amusement parks, have reported remarkable topline growth in both quarterly and yearly periods.

Meanwhile, cinema chains have taken the lead in terms of operating profit growth. It's worth noting, however, that this growth rate is abnormal, as both PVR and Inox Leisure were impacted by the pandemic in the previous year.

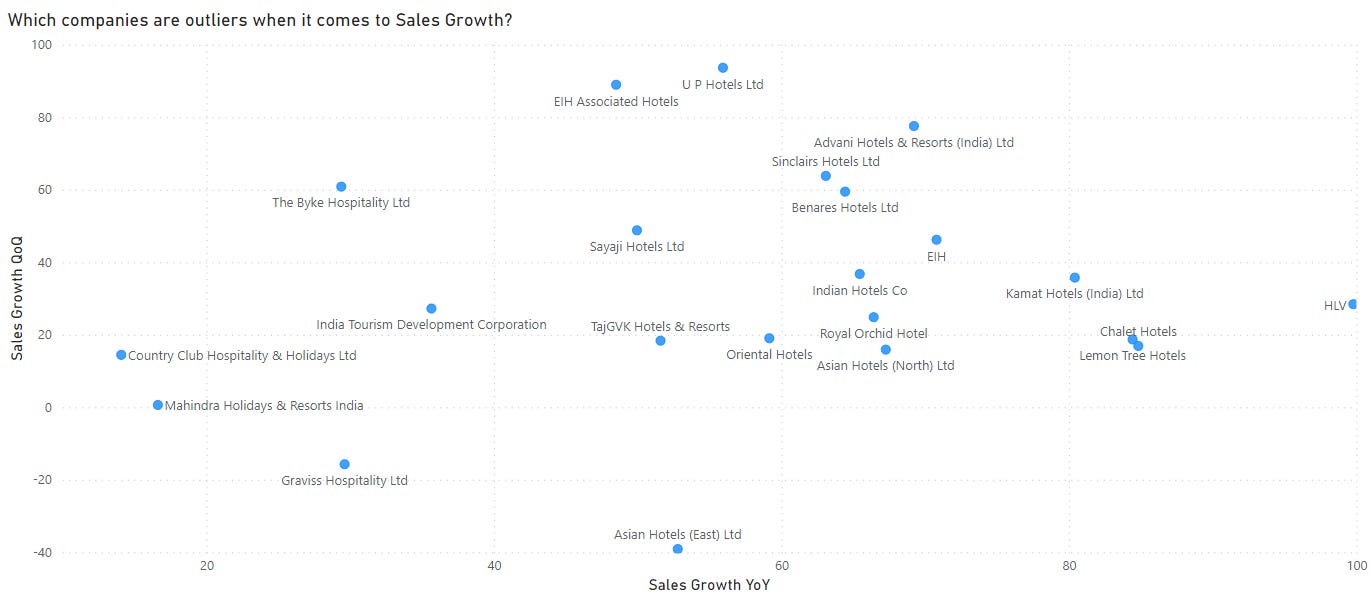

The topline growth of hotels is varied, with companies like Mahindra Holidays & Resorts struggling to grow, despite tailwinds in the sector. On the other hand relatively unknown firms like, UP Hotels, the owner of the Hotel Clarks chain, and EIH Associated Hotels, a JV of the Oberoi group, have exhibited the best overall performance at both quarterly and yearly levels.

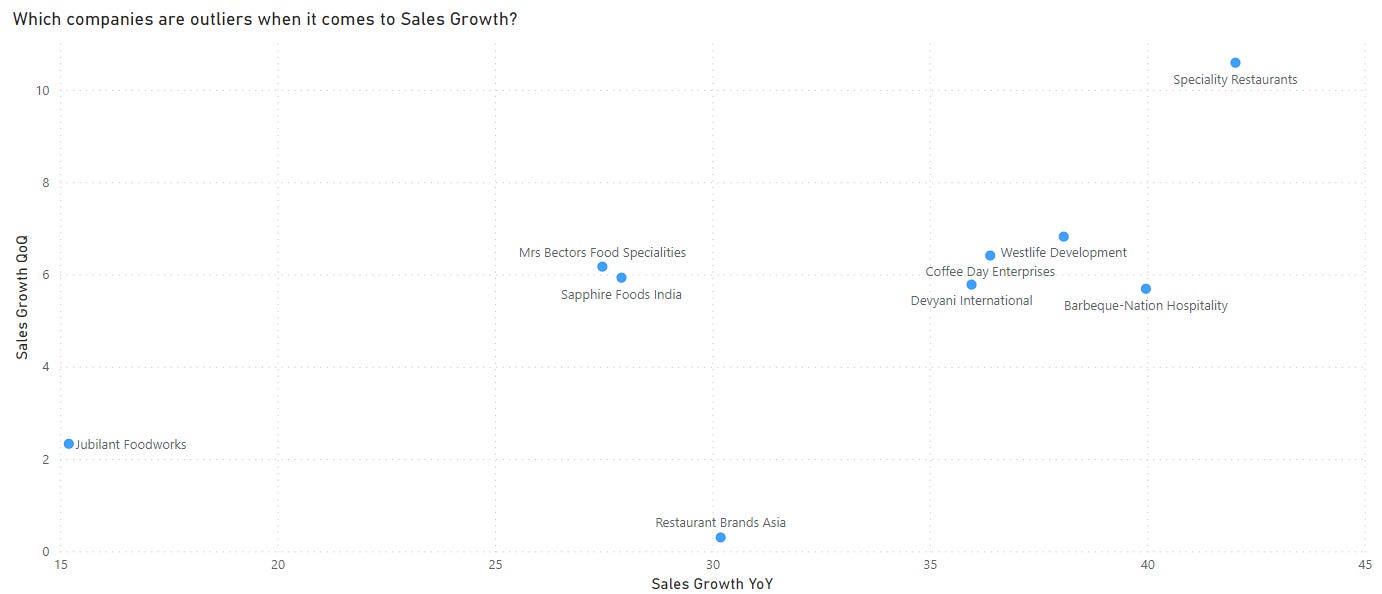

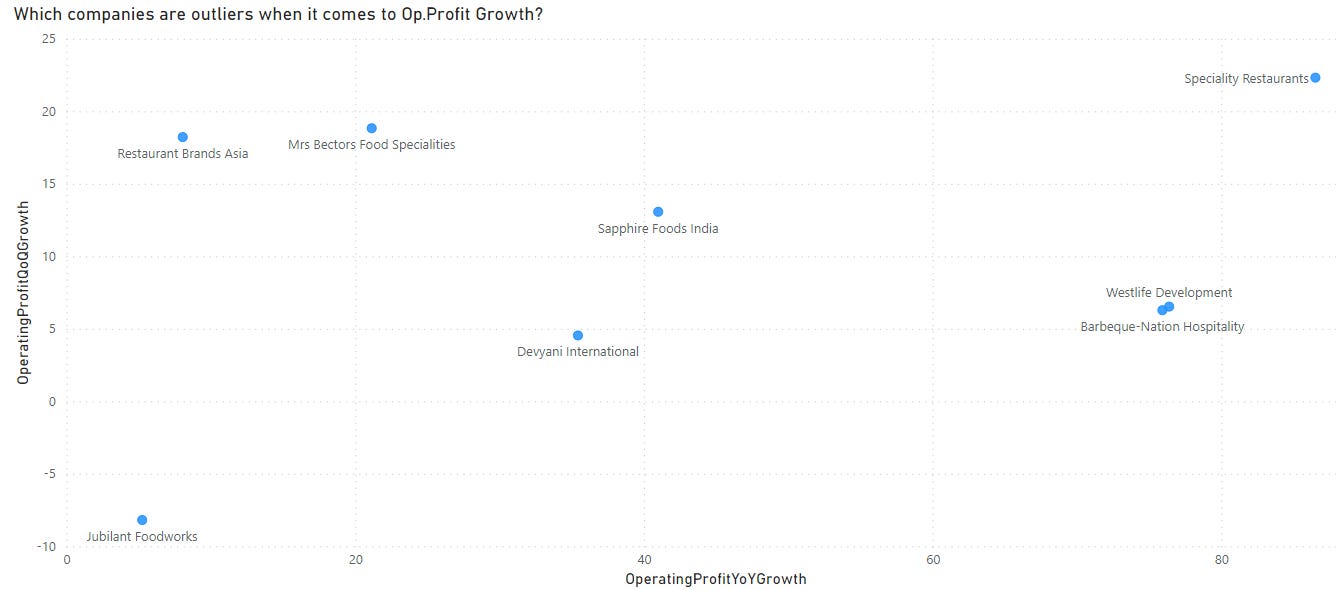

Now, let's shift our focus to one of the most adored sectors in the retail and hospitality industry - the QSR and traditional restaurant chains.

Among them, Speciality Restaurants - the company behind the popular 'Mainland China' and 'Asian Kitchen' restaurants - stands out as a clear outlier.

Among pure QSR names, Westlife Development - operator of McDonald’s stands out.

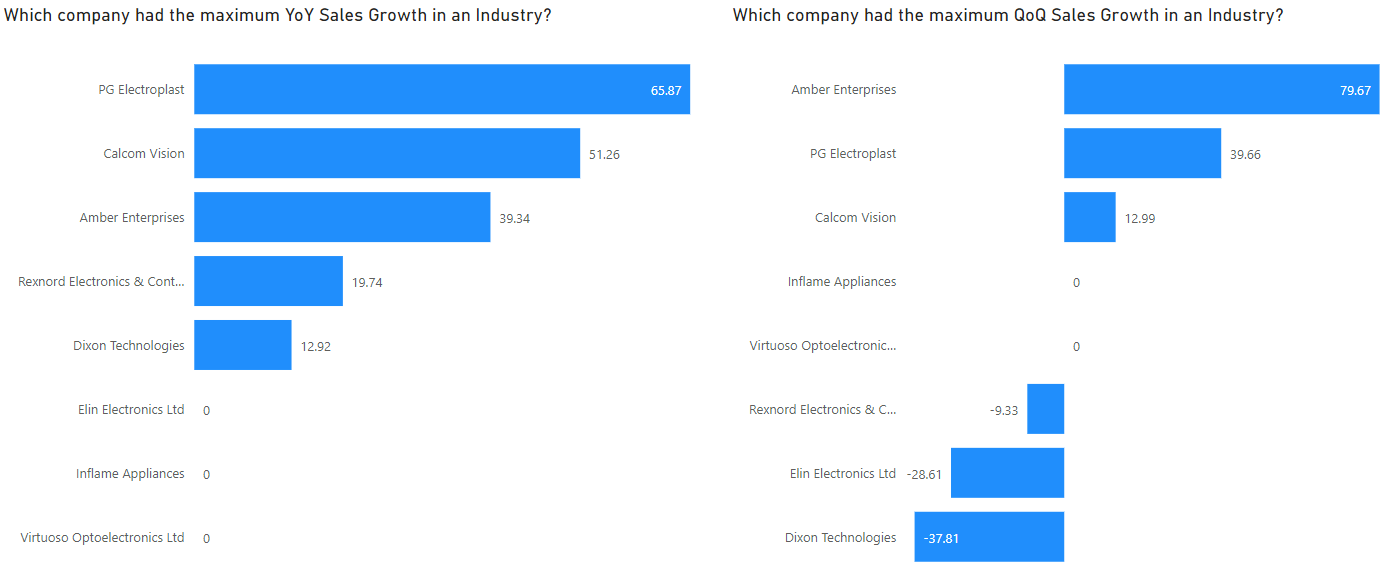

Contract Manufacturing of Electronics

The median yearly topline growth for electronics contract manufacturing space has been ~16% and median yearly bottom-line growth around ~19%.

Here, three companies - Amber Enterprises, PG Electroplast and Calcom Vision stand out among the rest.

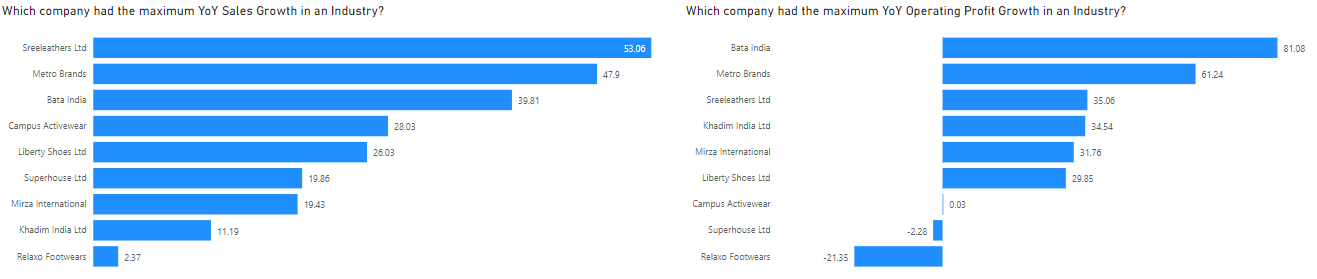

Footwear

Within the footwear industry, some of the most popular and beloved stocks like Relaxo seem to be clearly struggling while other ignored names like Bata India emerging as clear leaders.

This space was also a recipient of the re-opening tailwinds and has been growing topline at a median growth rate of ~26% and bottom line at ~32%.

The quarterly growth rate has slowed down sharply to ~1.7%, so some headwinds maybe ahead.

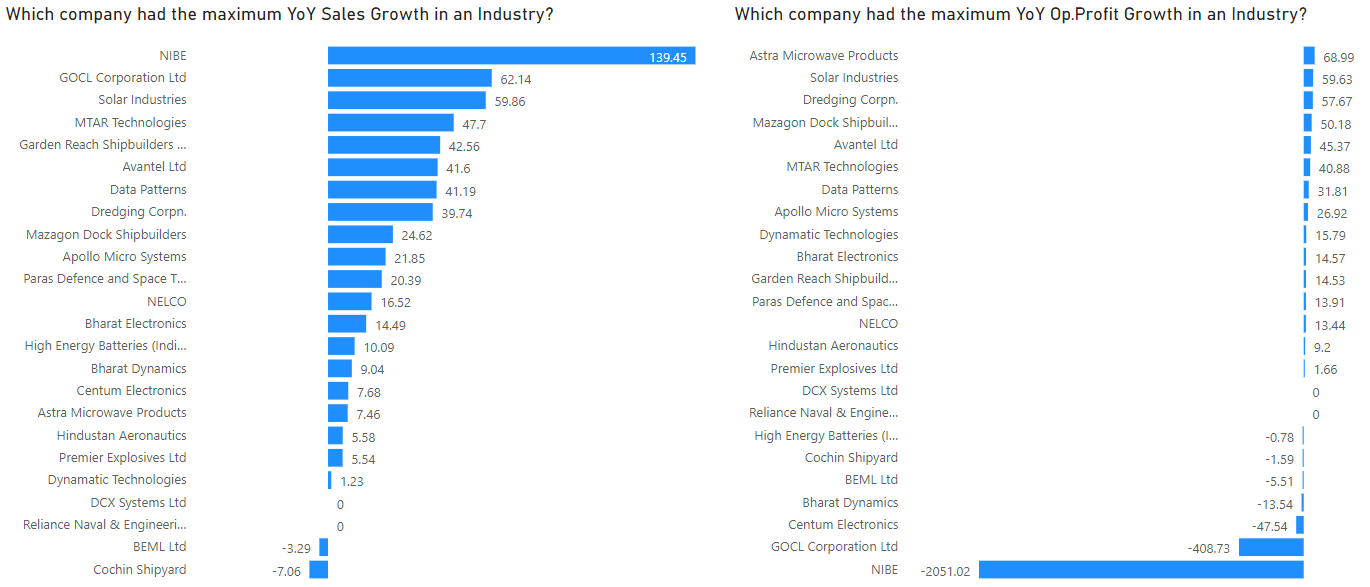

Defence

Companies across the defence sector in India posted a ~8.4% quarterly median topline growth and a similar ~8.5% quarterly bottom-line growth.

Most listed companies in this sector are quite different from each other in terms of product offerings, maturity and technical capabilities, as such it is hard to do a like for like comparison.

Some of the companies that stand out are Solar Industries, Astra Microwave Products and ship developers like Mazagon Dock Shipbuilders.

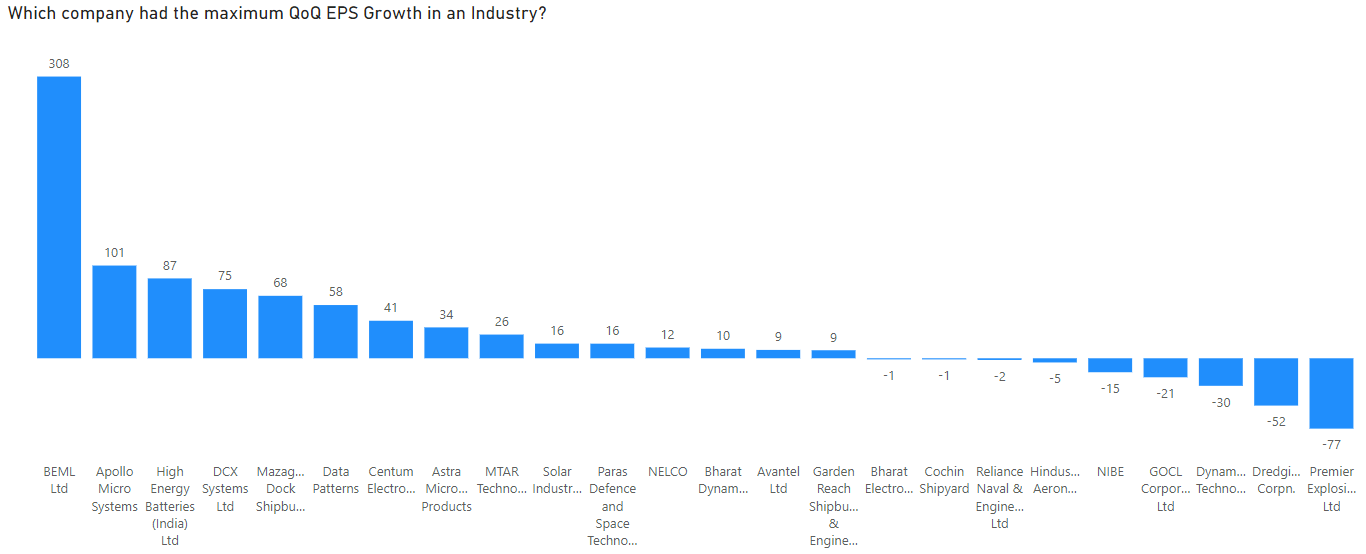

In terms of pure quarterly EPS Growth, BEML takes the pole position.

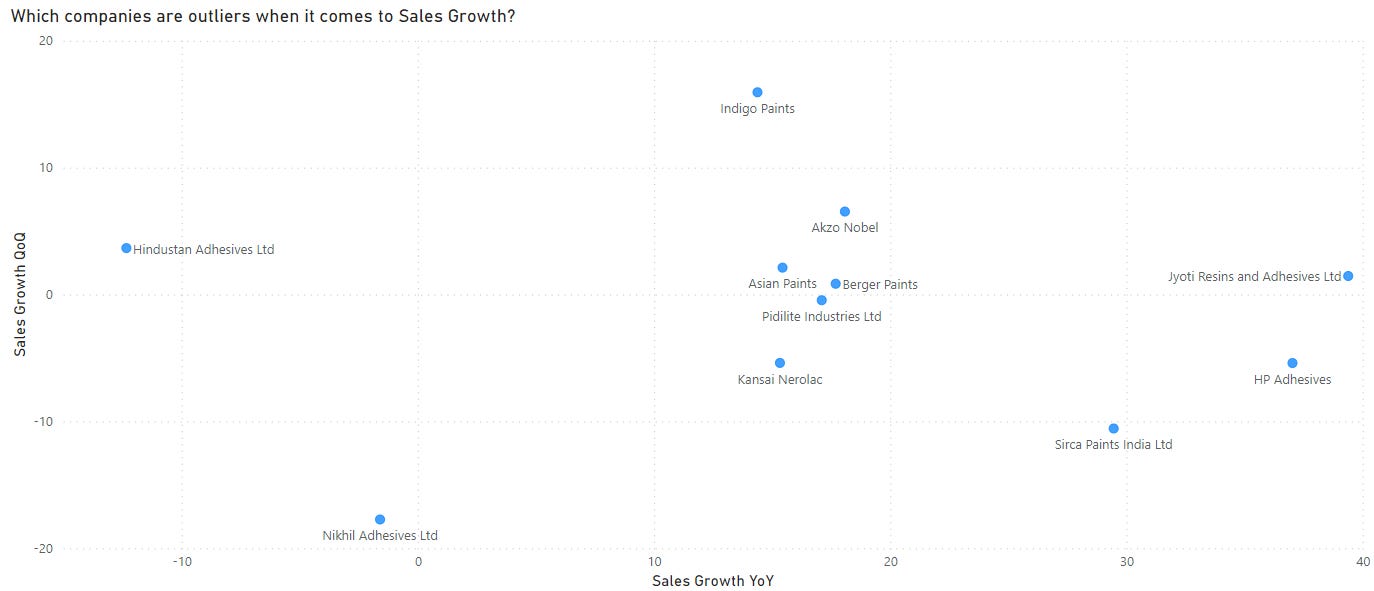

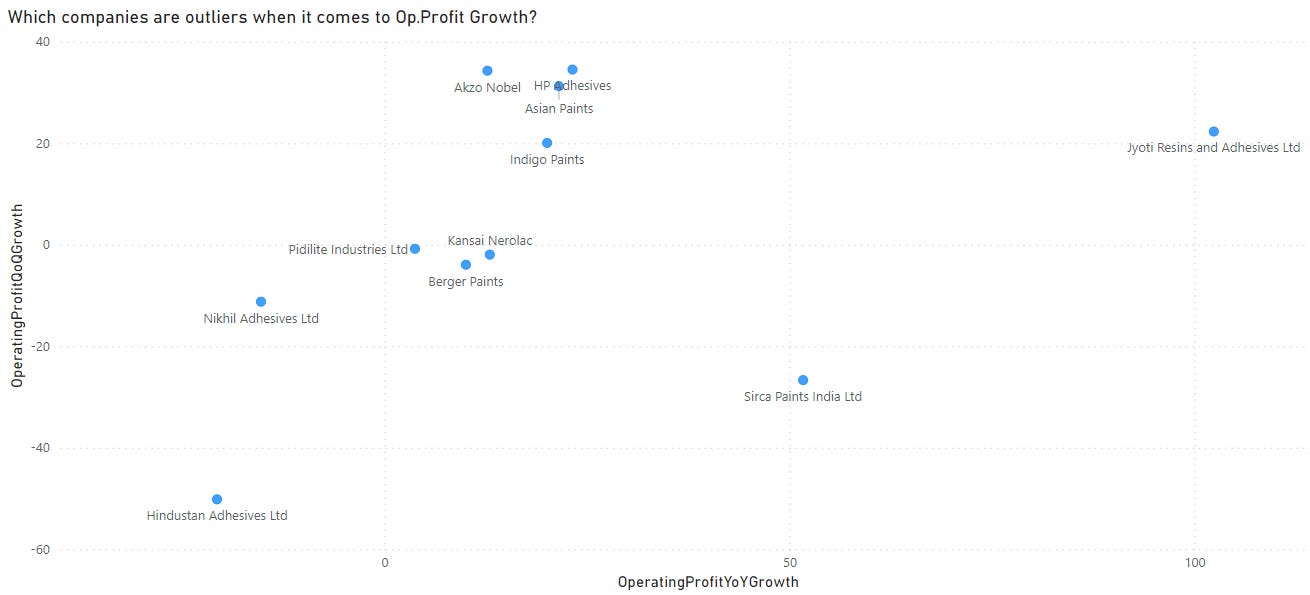

Paints & Adhesives

The median quarterly growth rate for Paints & Adhesives companies was at a negative 0.8%. The only company that stands out here among its peers its Jyoti Resins and Adhesives.

Jyoti Resins and Adhesives has been quite consistent, beating out its peer group in almost all of yearly and quarterly growth metrics.

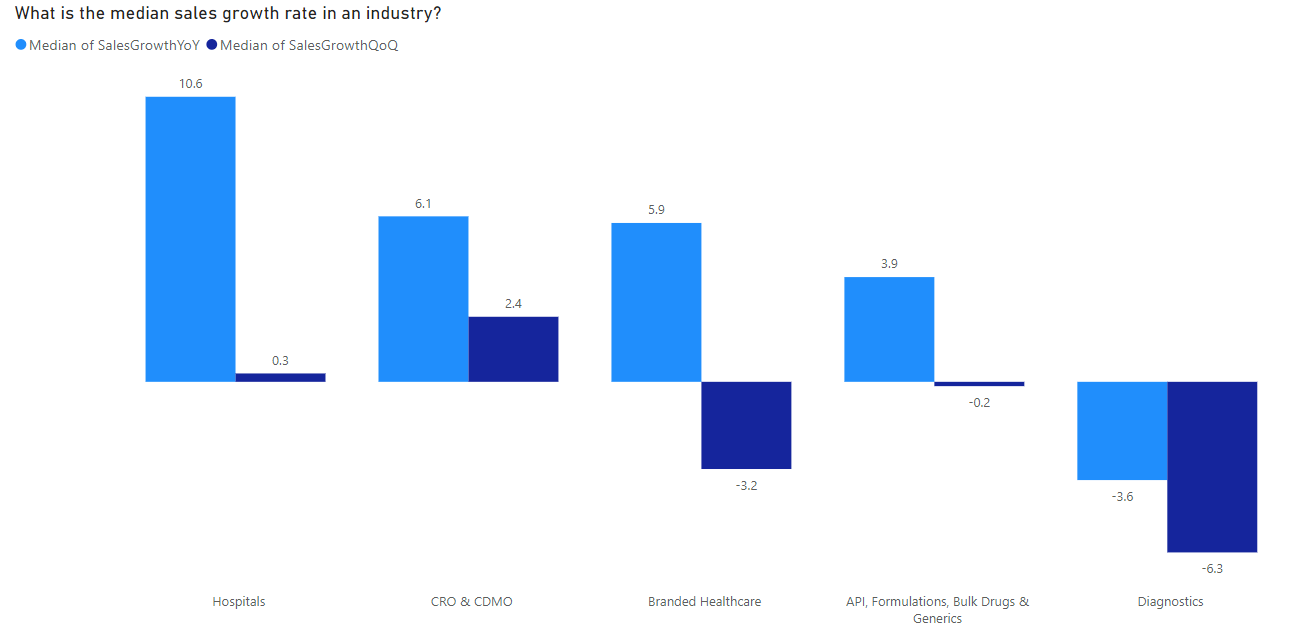

Healthcare

Within the healthcare sector, hospitals have published the best yearly topline performance, increasing sales by ~10.6%. The worst performing part of healthcare seems to be diagnostics with this quarter’s median topline growth coming in at a negative 6.3%.

Narayana Hrudayalaya, KIMS, Dr. Agarwal's Eye Hospital, and Lotus Eye Hospital are among the hospitals with the highest level of performance

Auto

Autos, which were the star performing sector of 2022, showed signs of slowing down this quarter. While the median yearly sales growth for auto companies comes in at a impressive 18%, the quarterly sales growth was at a negative 3.3%. Only about 30% of auto companies reported a positive sales growth vs previous quarter.

Among the names that stand out are - Olectra Greentech, Kabra Extrusion Technik, Automotive Axles and NDR Auto Components.

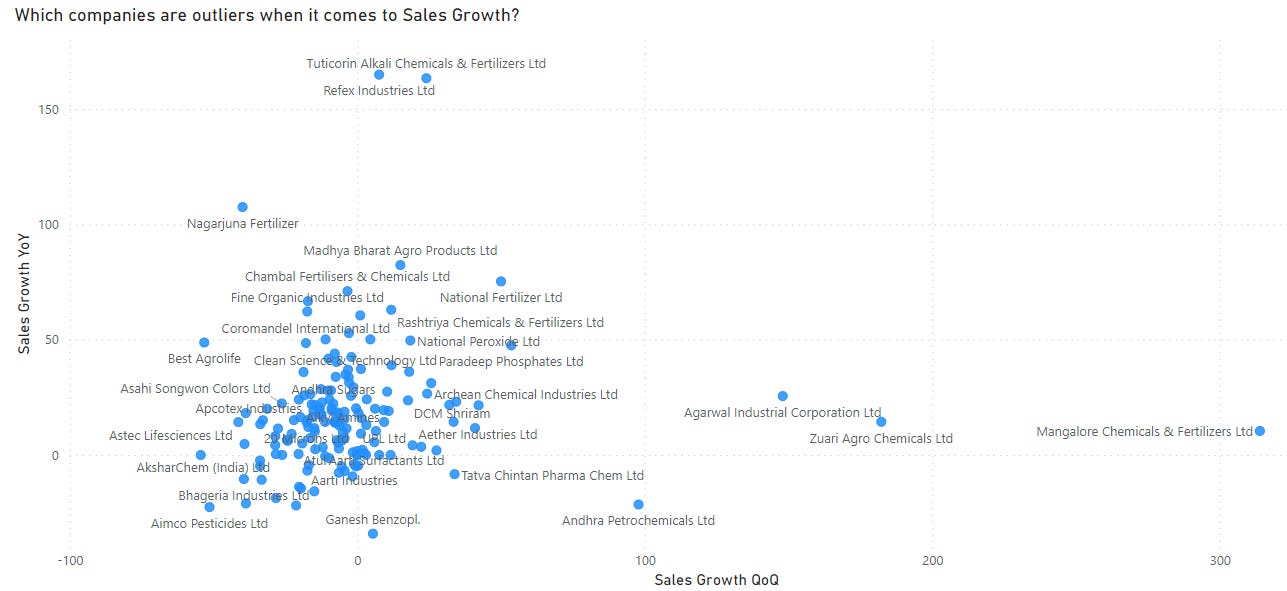

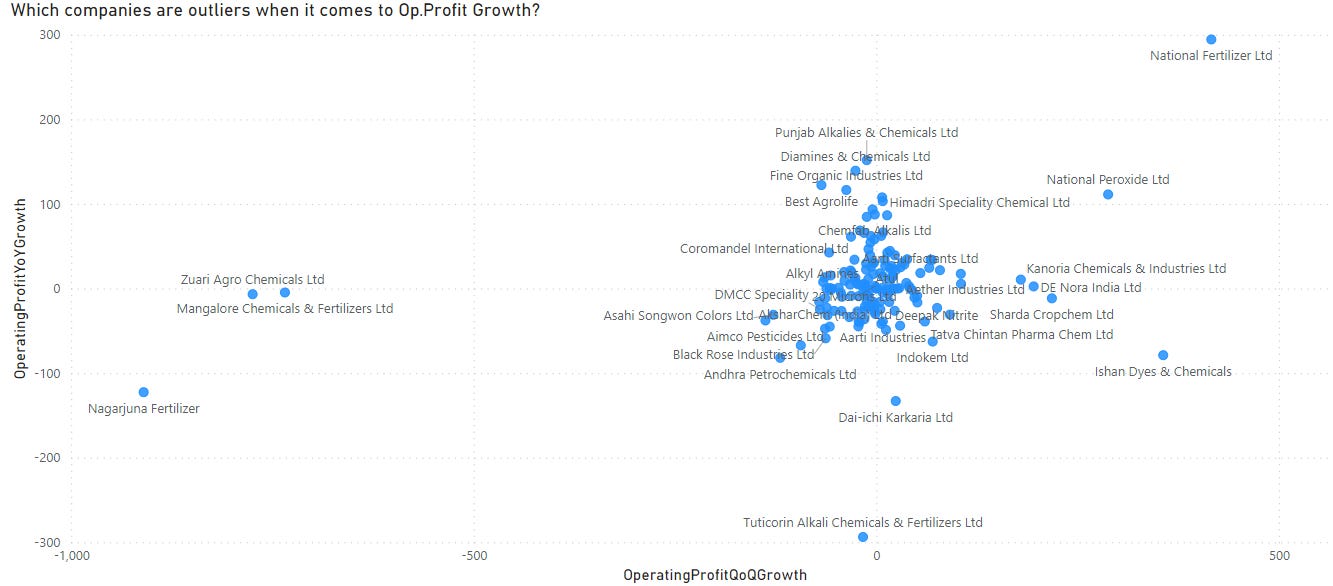

Chemicals

Chemical sector too, broadly speaking, seems to be reeling under pressure. The earnings growth, both yearly and quarterly, in this sector is non-existent, with a median quarterly topline growth of a negative 6.8%.

High valuation of companies in this sector, also makes it prone to severe stock price corrections amidst a sub par performance.

The fertilizer companies appear to be the only area showing strong performance within the wider chemical sector. Nearly all fertilizer companies have reported robust double-digit growth rates, and in some cases, even triple-digit growth rates.

Notably, National Fertilizer stands out as an outlier, boasting approximately 295% yearly growth in operating profit and about 75% yearly growth in sales.

Conclusion

In summary, the Q3FY23 earnings analysis of Corporate India reveals a mixed bag of results, with indications of a slowdown in consumption-led growth. While certain sectors such as Railways, Hospitality, and Defence are performing well due to various reasons, there is a lack of broad-based earnings growth. Even within large sectors such as chemicals, only specific sub-sectors, like fertilizers, are showing strong performance, with very few companies in that sub-sector performing exceptionally well.

Given the absence of widespread earnings growth, it may become increasingly challenging to select winning stocks going forward, particularly when coupled with a challenging global economic outlook. Therefore, it is likely that the overall market will consolidate for at least another quarter.

As a first-time earnings analysis, certain sectors such as technology were not covered due to ongoing data organization efforts at my end.

While this article may contain a lot of metrics and data, I look forward to hearing your thoughts, criticisms, feedbacks and comments on how I can improve this for the next quarter.

Going forward, this will be a regular exercise on my part and you can expect a detailed earnings analysis like this, once every quarter.

Please do leave a comment and share your valuable feedback.

Thankyou for reading. Until next time.

Peace,

Tar

Great work, really appreciate your hardwork. Thanks sir

I can imagine how you might have struggled with master data/sector classification. Classifying conglomerates like ITC!!. Great job with visualization and easy to understand format.