The year is 2008.

News headlines are filled with the collapse of Lehman Brothers and the onset of the Great Financial Crisis. Stock markets around the world have tanked anywhere between 40 to 70% from their last peak, made earlier in 2007. Economic outlook all over the world is grim and money seems to be running on short supply.

It’s against this backdrop, a young Sahil Barua is brainstorming various business ideas from his dorm room in IIM Bangalore. As the economic conditions throughout 2008 deteriorated, so did his hopes to launch a start up.

He closes the lid on his business plans and takes a job as a management consultant with Bain & Co. Little does Sahil know at the time that he will meet his future co-founders at Bain and three years later in 2011, they will together lay the foundation for what will become a $3 Billion logistics company.

This is the story of Delhivery.

Before we proceed, please consider sharing this write up with your friends or on your social media.

My aim, through these write ups, is to reach out to as many people as I can, so that they can make informed financial decisions.

Part One: From Hyper Local to eCommerce 🚚

Delhivery started as a hyperlocal food delivery service in New Delhi.

In 2011, restaurants were increasingly being introduced to the power of internet and while Zomato was helping them coming online, food delivery was still managed by individual restaurants.

There was money to be made in streamlining food deliveries and so Sahil along with his colleague Suraj Saharan quit their consulting jobs with Bain and started Delhivery.

What started as a successful hyperlocal food delivery service quickly pivoted to building a logistics firm for eCommerce.

The main motivation to pivot was the scale of opportunity and absence of anyone else trying to optimize logistics for eCommerce. Traditional players were accustomed to delivering documents, pre paid orders and movement of freight where as in eCommerce, there is usually a two way logistics channel - business to customer and then customer to business.

The latter is usually return orders and cash collected from customer in case of cash on delivery, which were 90%+ eCommerce deliveries at the time. None of the existing logistics players were accustomed to this new way of delivering goods and their network built and optimized for old logistics industry would take a complete rebuild from the ground up to cater to this new segment.

This was an area ripe for opportunity for Delhivery. They could build a new logistics company that was designed from the ground up for eCommerce - and so they did.

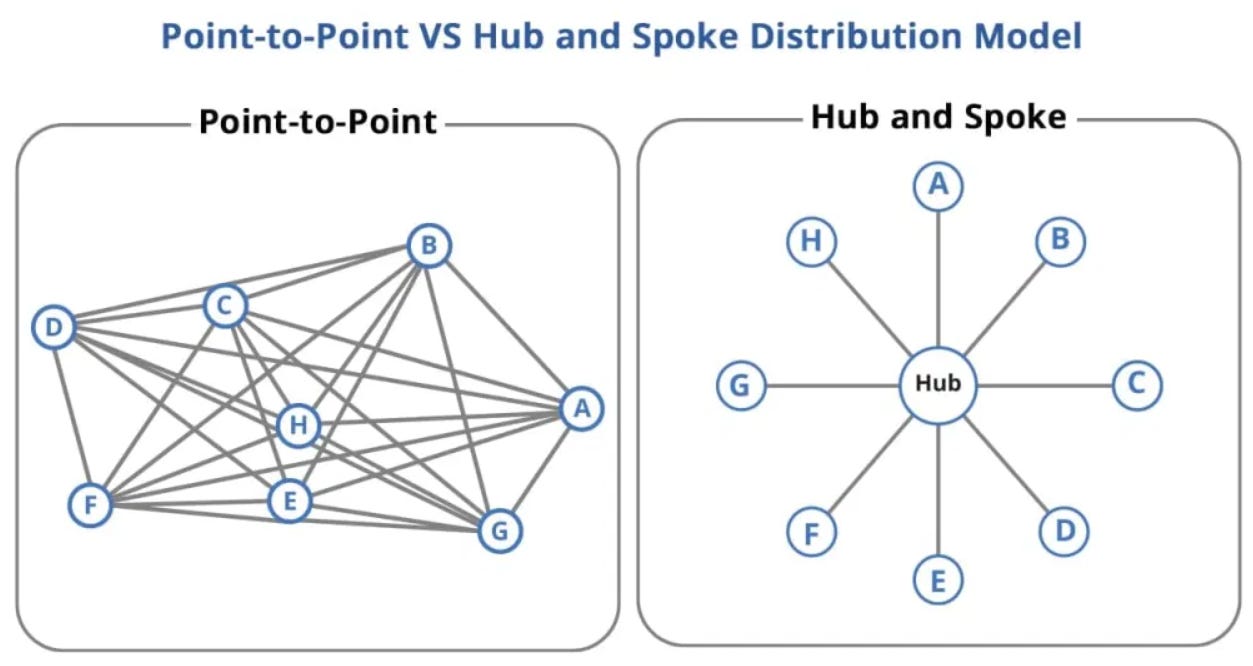

Traditional Logistics vs Delhivery

Traditional logistics players work on a Hub and Spoke Model.

Deliveries collected from various places are sent to a central distribution and sorting hub for further processing. The hub then further sends these packages to smaller sorting facilities until they are sent to delivery centers responsible for each delivery area.

This model is slow and works well when time isn’t of the essence.

Delhivery follows a point to point model. Each facility in this model acts as its own hub and sorting facility. This allows Delhivery to pick up packages from anywhere and directly send it to the nearest sorting facility which further processes it directly to the facility closest to delivery destination.

This model is fast and with a lot of help from technology Delhivery is able to reduce the delivery time from a few weeks to a one or two days.

The model works even faster when number of nodes in the network increase significantly.

Below is an illustration of the Delhivery Logistics Mesh Network.

As illustrated above, Delhivery has a mesh network on a scale unlike anyone else in India. In a city like Mumbai, where eCommerce deliveries are high, they can simply add more nodes and meet the demand. Where as in Tier 3 cities where eCommerce deliveries are considerably less compared to Mumbai, they can make do with a fewer nodes.

For a traditional player following a hub and spoke model, this agility in enhancing the network doesn’t work as they have to incur considerable spend to introduce a new hub in the model.

This is Delhivery’s competitive advantage #1.

A Lot of help from Technology

On the face of it, Delhivery looks like a logistics company, but as you peel through the layers, you will discover almost every single aspect of their logistics network is operated via their proprietary technology stack.

In Delhivery’s case, they like to build the technology first and logistics later.

The company has over 80 proprietary self developed applications that work together to help Delhivery deliver millions of packages every year. Delhivery further goes ahead and collects data points on each of these deliveries. Machine Learning optimized algorithms continuously consume these datapoints and work tirelessly behind the scenes to optimize this logistics network even further.

This is the same playbook Amazon has used over the years to help it become the largest, fastest and most reliable logistics company in the world.

Delhivery’s logistics technology is so successful, that they are now exposing it as a SaaS offering to other enterprises and customers.

Excerpt from their DRHP ⤵️

“We intend to externalize our logistics operating system as a platform and a SaaS offering by enabling other logistics service provider, logistics-tech companies, and enterprise and developer partners, in India and globally.”

This SaaS offering on its own can be a significant pie of their revenue a couple years down the road.

Test for their technology prowess came in during the Covid lockdown in March 2020.

In March 2020, when India announced a completed lockdown, the logistics industry came to a definitive halt. Ten days later when the country selectively reopened, Delhivery by leveraging its ‘Logistics OS’ was able to selectively activate 8300 pin codes for essential delivery and re-establish operations overnight simply by looking at unstructured data (announcements by local, state and national authorities).

An example of the applications developed on their technology stack is Orion, the application they use for Truckload Freight Management. Delhivery being an asset light firm, owns a tiny portion of delivery fleet (less than 8%), rest of it is either leased or sourced via Orion.

Orion helps match demand from shippers with suppliers of truckload capacity in real time. The application was primarily built to help Delhivery source delivery fleet from its network partners, but now has an added optionality of being launched as a standalone SaaS based offering for other large logistics companies.

Deeply integrated technology is Delhivery’s competitive advantage #2.

Why own an asset when you can lease it?

Logistics by its very nature is an asset heavy, upfront capex driven business.

A typical logistics company requires warehouses, distribution centers, fulfilment centers, staff to deliver and manage packages, delivery fleet and capital to run the business. All this before even it can begin to deliver its first order.

It should come as no surprise then, that more than 95% of logistics industry in India is fragmented and made up of small business owners running a logistics service at a very small scale.

For example, 85% of Road Transport companies in India own less than 20 trucks that drive on an average less than 300 kms a day. 90% of warehouses in India are smaller than 10,000 sq feet in size.

These small businesses cannot become mid to large scale companies unless there is technology to help them vastly increase their logistics network via partnerships with larger companies.

Delhivery through its technology solutions found a way to effectively build and run a marketplace for this vast network of small scale untapped capacity of truck fleets and warehouses throughout India.

Most of this demand in this marketplace today is from Delhivery itself.

Excerpt from their DRHP ⤵️

“Our systems function as a managed marketplaces that match partner capacity with Delhivery internal and third-party client demand based on partners’ service quality ratings and pricing.

This approach has enabled us to quickly expand to geographically dispersed locations, optimize loads, improve our cost structure and maintain flexibility in handling seasonal demands while incurring minimal fixed costs and capital expenditures.”

Delhivery’s motto is to invest in critical infrastructure while leveraging everything else via its network partners.

Delhivery owns a little assets of its own but leases a lot of them.

The company effectively has 12.42 Million sq. ft of logistics space available to it throughout India that cover over 17,045 pin codes which are serviced by its self owned and partner contracted fleet of trucks delivering over a billion packages weighing almost a million tonnes for its 21,000+ customers.

Pretty big and noteworthy numbers for a company started less than a decade ago.

This ability to scale up its logistics network without having to burn a lot of cash is Delhivery’s competitive advantage #3.

Partner and Automate

The little assets Delhivery does own on its own are highly automated. Take for example, their Gateways - which are the largest logistics facilities forming the core of their network.

Gateways are the big nodes in their mesh logistics network that handle all types of packages and perform majority of the tasks. The entire delivery network functions as fast as Gateways can. It is for this reason Delhivery has invested heavily into automating every single aspect of their Gateway functions that can be automated.

Packages are sorted automatically as soon as they arrive to a Gateway, with some Gateways being completely automated, capable of handling upto 32,000 shipments per hour.

Partnerships are another area where Delhivery has started to excel. In order to grow operations across border and stabilize Indian revenues, the company has entered into strategic alliances with FedEx and Aramex.

Any packages coming through the FedEx or Aramex networks to India will be delivered via Delhivery through its domestics logistics set up. Similarly any packages originating out of India to International destinations on Delhivery network will be serviced by FedEx and Aramex.

Apart from FedEx and Aramex, Delhivery already has a partnership with UPS which they entered into in 2019.

This ability to struck partnerships with strongest global players, helps Delhivery expand its network without any additional costs and is its competitive advantage #4.

Before we move on to financials, above is the brief timeline of Delhivery since its incorporation in 2011.

Part Two: All About Money 🪙💰

Revenues

70% of FY21 revenue for Delhivery, or 2,550cr out of 3,635cr was from express shipment of deliveries for other eCommerce websites.

The rest 30% of revenue is divided between Part Truck Load (11%), Supply Chain Services (11%), Full Truck Load (6%) and Cross Border Delivery Services (3%).

Needless to mention an overwhelming majority of this revenue pie is linked to growth of eCommerce in India. Delhivery acknowledges and mentions this as one of their key risks in their DRHP.

Excerpt from their DRHP ⤵️

“Although we continue to diversify our customer base, e-commerce customers contribute a majority of our shipment volume. Accordingly, our business and growth are highly correlated with the growth of the eCommerce industry and more generally, commerce, in India.”

Delhivery is slowly diversifying into other industry verticals like shipment of customer electronics, consumer durables, FMCG, healthcare, lifestyle, automobiles and manufacturing.

Overtime the dependency on eCommerce should go down but I doubt it will ever be less than 50% of the overall revenue pie.

Reducing Losses and Increasing Income

Like most start ups, Delhivery is a loss making company. Unlike most start ups though, Delhivery has a clear path to profitability as their revenues are growing at a CAGR of 44% while losses are reducing.

The two main top expenses for the company are

Freight Handling and Servicing (76% of Revenue)

Employee Benefit Expenses (16% of Revenue)

As the company’s operations expand and volumes increase, operating leverage should play out and help reduce the freight handling expenses to a more manageable extent.

The employee benefit expenses however, are here to stay and may even increase in future as the company attracts and tries to retain more technological talent.

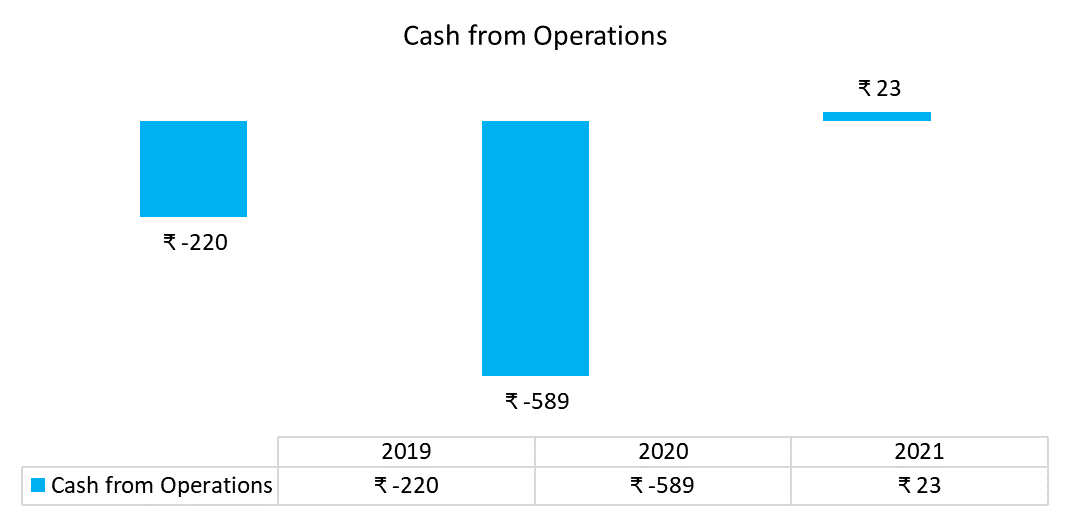

Increasing income and reducing losses, made Delhivery cash positive for the first time in 2021.

The losses might be reducing but make no mistake, this will never be a high Gross Margin business unless optionalities like their SaaS based offering for ‘Logistics OS’ playout and starts contributing to a significant chunk of revenue.

Debt

As of June 20, 2021 Delhivery had about ~342cr of long term and short term debt on its books. Much of this will be repaid from some of the proceeds from IPO.

Customer Concentration

A key area of risk for Delhivery is the customer concentration. An average of ~45% of revenue comes from just five customers.

Delhivery does not disclose the name of these customers but it is safe to assume some of these five customers are largest eCommerce companies in India like Flipkart, Myntra, Amazon etc.

Most of these large eCommerce players are investing in logistics capability of their own and only hire Delhivery when their own internal logistics systems are running at full capacity. As such as and when the logistical prowess of these eCommerce companies increases, their dependency on Delhivery should reduce and as such Delhivery’s revenues from these customers.

To counteract this revenue concentration risk, Delhivery has set its sights on a different kind of customer - the D2C (Direct to Customer) companies. These are your mom and pop small internet businesses that do not have the scale to invest in logistics of their own but want to primarily sell their products on the internet.

Delhivery onboards these customers and provides them with the logistics capability for them to conduct their business online. As of FY 21, some 675 out of 21,000 customers Delhivery caters to, were D2C companies.

D2C is kind of going through its own renaissance in India and is expected to grow faster than traditional large scale eCommerce.

Part Three: Valuations and About The IPO

Objectives of IPO Offer

The company is raising 3750cr in its IPO via issuing fresh equity. Out of this 3750cr, 2500cr will be used for organic growth - expanding the current logistics network and upgrading and improving its ‘Logistics OS’ proprietary technology stack.

The remaining 1250cr will be used to fund acquisitions and other inorganic growth opportunities.

Majority of the company is owned by venture and private equity funds, with original founders collectively owning less than ~8% of the entire company.

The DRHP currently does not indicate how much these VC and PE funds wants to offload their stake in the IPO.

Valuations

Updated on 11th May 2022

Delhivery finally launched its IPO today seeking a market cap of 35,000cr at the upper band of the IPO price range of Rs 462 to Rs 487 per share.

This valuation target, by any stretch of imagination is towards the extreme end.

To give you some perspective, you can buy most of the listed profitable logistics companies in India for 35,000cr or you can buy a single loss making Delhivery.

The pre IPO financing round for Delhivery pegged its valuations at 22,500cr (~$3 Billion) just a few months back, so even with that in mind its quite a formidable ask to list oneself at 35,000cr market cap.

While Delhivery has a great business that one day maybe can recreate what the likes of FedEx did for America in 1980s, today the price is too high to take that gamble.

As with all the other IPOs, I will follow my rule and wait for six to twelve months before taking a call to invest.

Conclusion

Logistics is a high barrier capex heavy sector and Delhivery through the use of its own proprietary technology stack has enabled itself to raise these barriers to entry even further.

In my opinion, Delhivery is a good proxy bet to play the growth of eCommerce industry in India.

After my deep dive on Nykaa, this was the second company, I personally really enjoyed reading in depth and writing about.

I hope your experience was the same.

Thank you for reading, see you in the next one.

Peace,

Tar

Enjoyed this. I am really bullish on e-commerce growth in the coming decades. Looking forward to the IPO valuations.

excellent article, but I don't like the middle management. I had given interview for this company pre ipo for Salesforce sales Consultant role problem was everyone in their management team was always late. Time management & respecting others time I feel should be very highly valued.